Our short answer is: yes.

from NBER Working Paper No. 30737 (An update of the results of this survey postal) by myself and Rashad Ahmedout today (summary):

This paper shows that foreign term spreads constructed from bond yields of non-U.S. G-7 members predict future U.S. recessions, and that foreign term spreads are more predictive of U.S. recessions in the next year than U.S. term spreads. Both U.S. and foreign term spreads can provide information about the U.S. economy, but apply to different scopes and to different components of economic activity. Smaller U.S. term spreads lead to smaller foreign term spreads and dollar appreciation. Small foreign exchange rate differentials will not lead to a sharp depreciation of the dollar, but will lead to a continued decline in US exports and inflows of foreign direct investment into the US. These findings are consistent with the proposition that foreign term spreads contain growth spillovers from the United States and that the resulting dollar strength and slowdown abroad flow back to the United States.

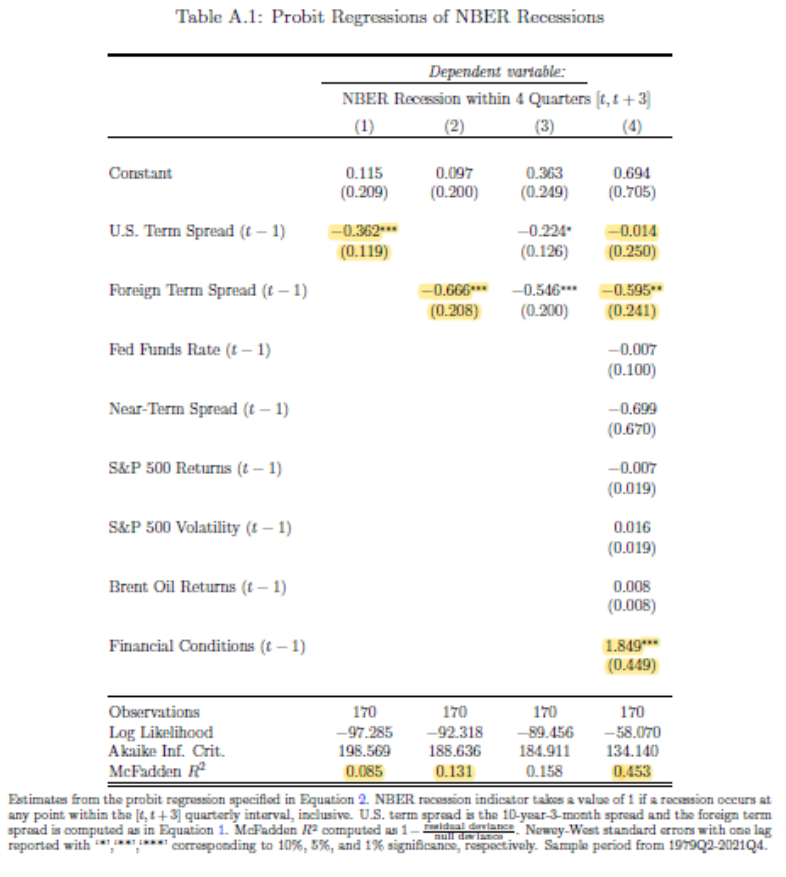

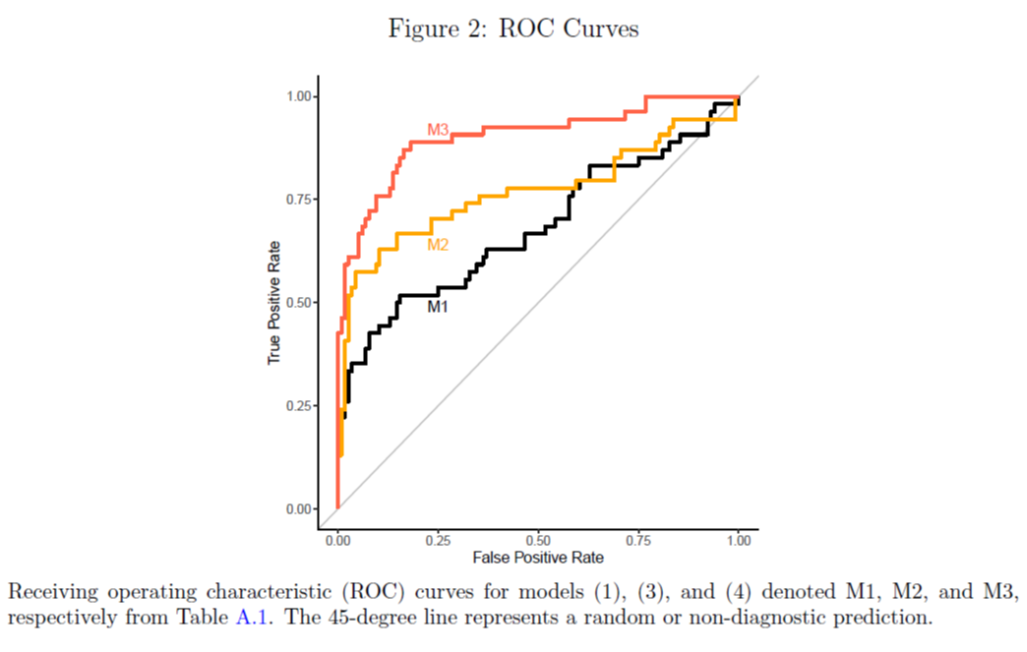

This is the AUROC for US term spreads only (Model 1), foreign term spreads only (Model 2), and US and foreign term spreads plus other variables plus the financial conditions index (Model).

These AUROCs belong to columns (1), (2) and (4) of Table A.1. Note that we are not saying that U.S. term spreads are unpredictable; simply that including foreign term spreads and a range of other U.S. variables results in a statistically insignificant coefficient on U.S. term spreads (U.S. term spreads do appear in (3) is shown as significant).

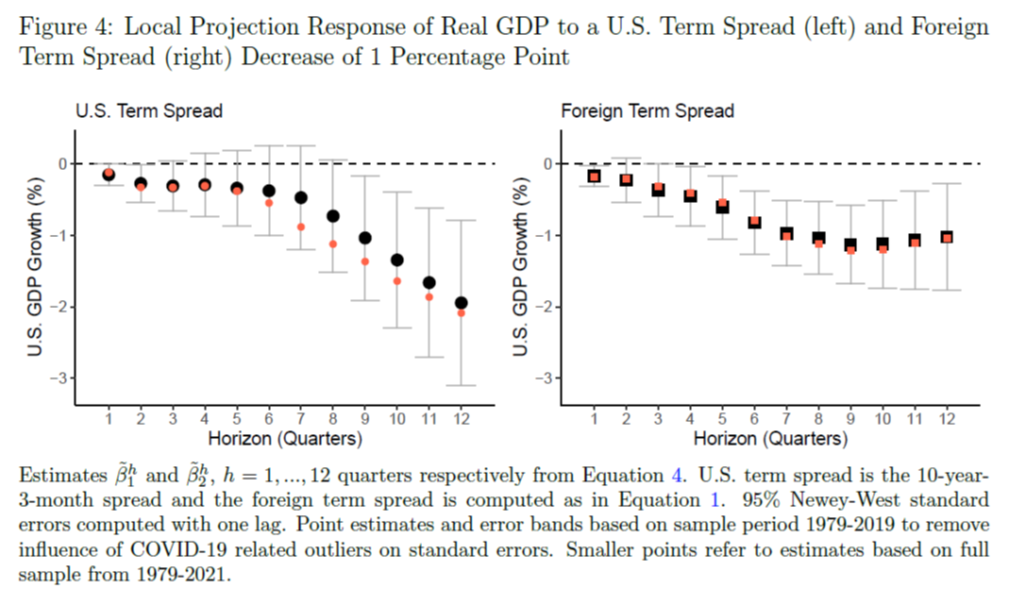

Turning to GDP growth, Figure 4 shows the impulse response function in response to a 1 percentage point increase in the US (foreign) 10-year to 3-month interest rate differential.

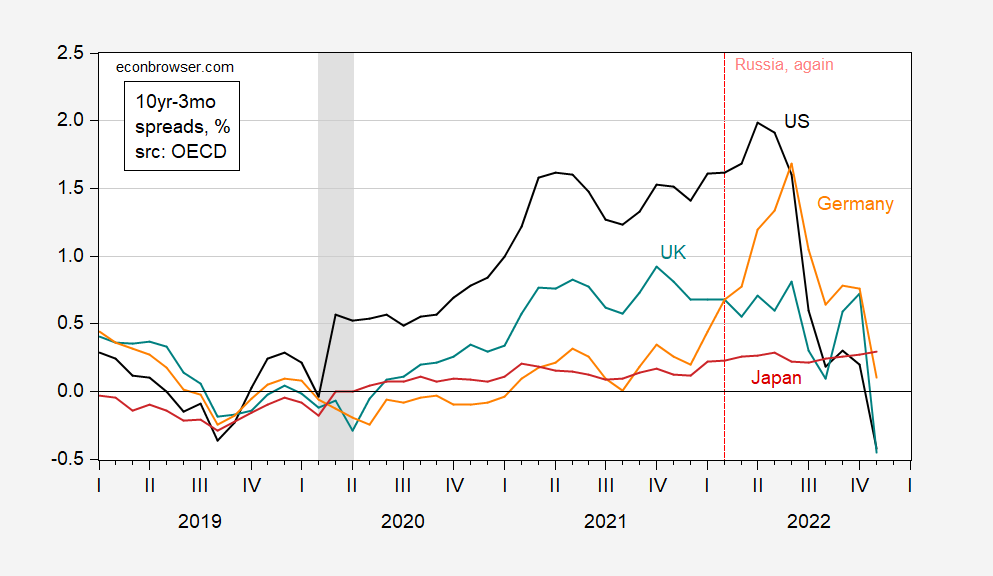

Here’s the current situation on the 10yr-3mo spread (Treasuries minus 3m Treasuries or interbank, depending on the OECD report):

figure 1: Ten-year government bond yields minus three-month rates, in %, for the United States (black), United Kingdom (teal), Germany (orange), and Japan (red). The three-month rate is the government bond yield in the United States, and the interbank rate in other countries. The NBER defines the peaks and troughs of U.S. recessions as shades of gray. Sources: Treasury via FRED, OECD key economic indicators, updated from Tradingeconomics.com, NBER, and author’s calculations.

The foreign yield curves in Germany (representing the Eurozone) and the UK are inverting. However, Japanese term spreads remain positive.

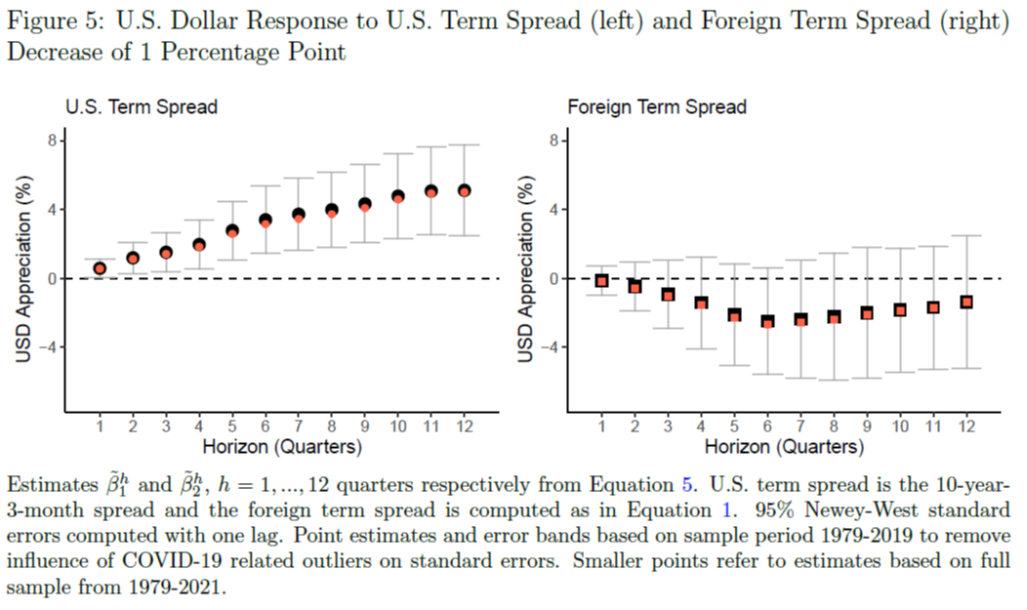

We also determine the dollar’s response to term spread shocks.

A positive shock to U.S. interest rate differentials strengthens the dollar, while a positive shock to foreign interest rate differentials depreciates the dollar. However, only the US IRF showed statistical significance.This discovery and Chen and Zeng (2013).

{kind=link}

{kind=link}