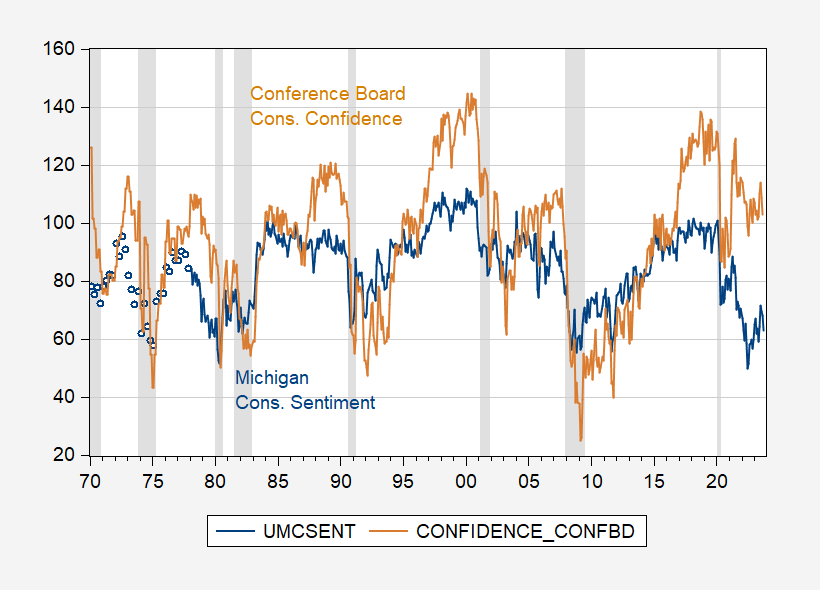

The Conference Board’s last article on the index was titled: “Expectations index fell for the second consecutive month, falling below the recession threshold”. Here’s how the index compares to the University of Michigan Consumer Sentiment Index.

figure 1: University of Michigan Consumer Confidence Index (blue) and Conference Board Consumer Confidence Index (tan). NBER-defined recession peak-to-trough dates appear gray. Sources: U.Michigan (from FRED), Confidence Council (from TradingEconomics), and NBER.

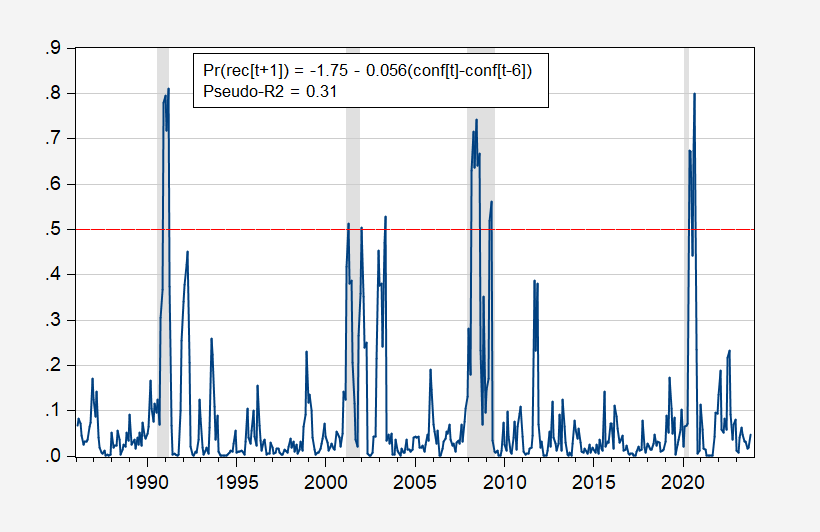

Regression using the Michigan index does not predict recession dates as defined by the NBER very well, so I rely on the Conference Board’s measure. Between 1986 and 2023, six-month changes lag one month, with a pseudo-R2 of 0.31 (assuming no recession as of October 2023). The forecast suggests that there will be no recession through October 2023.

figure 2: The one-month probability regression of the NBER recession date yields a recession probability that lags behind the six-month change in the consumer confidence index. NBER-defined recession peak-to-trough dates appear gray. Source: NBER and author’s calculations.

I’m exploiting the correlation between the sentiment index and the recession date, that’s it. A low confidence index is not the same as a recession (a recession is a broad-based, sustained decrease in economic activity that may cause or signal a decline in sentiment, but is not itself the same thing).

{kind=link}

{kind=link}