Plus the third release of GDP in the third quarter of 2023.

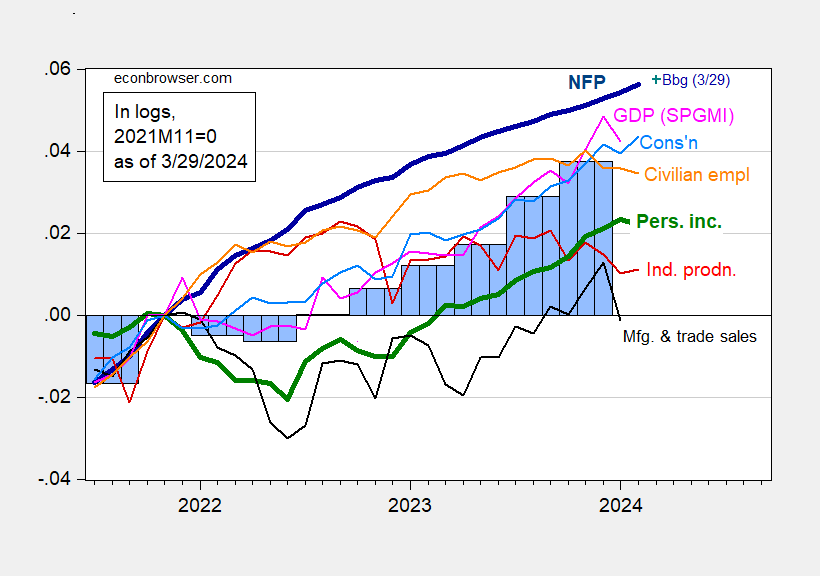

figure 1: CES nonfarm payrolls (bold blue), Philadelphia Fed early benchmark (cyan), civilian employment (orange), industrial production (red), 2017 personal income excluding current transfers (bold green), Manufacturing and trade sales in 2017 Ch.2017$ (black), 2017 Ch.2017$ consumption (light blue), 2017 Ch.2017$ monthly GDP (pink), the third release of GDP (blue bar), all logarithms normalized to 2021M11=0. Source: U.S. Bureau of Labor Statistics (BLS) via FRED, Federal Reserve, BEA 2023 Q4 2nd Edition, S&P Global Market Insights (Nigerian macroeconomic consultant, IHS Markit) (3/1/Published in 2024) and the author's calculations.

Consumption showed strength above consensus, while personal income before transfers declined. Manufacturing and trade sales fell sharply in January. Coupled with sluggish industrial production in February, economic growth is likely to slow.

That said, upward revisions to fourth-quarter GDP and aggregate demand indicators (final sales and final sales to domestic private buyers) point to strong momentum in economic activity.

{kind=link}

{kind=link}