And on the eve of the October jobs report. Based on Tuesday’s monthly GDP and last week’s consumption and income, we have pictures of some key series after the NBER Business Cycle Dating Committee (NBER BCDC):

figure 1: Nonfarm Payrolls, NFP (dark blue), Bloomberg Consensus as of 11/3 (blue+), civilian employment (orange), industrial production (red), excluding personal income transferred mid-2012 ( green), manufacturing and trade sales in 2012 dollars (black), consumption in 2012 dollars (light blue) and monthly GDP in 2012 dollars (pink), all log normalized to 2021M11=0 . The lilac shading indicates a hypothetical recession for 2022H1. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published Nov. 1, 2022), and author’s calculations.

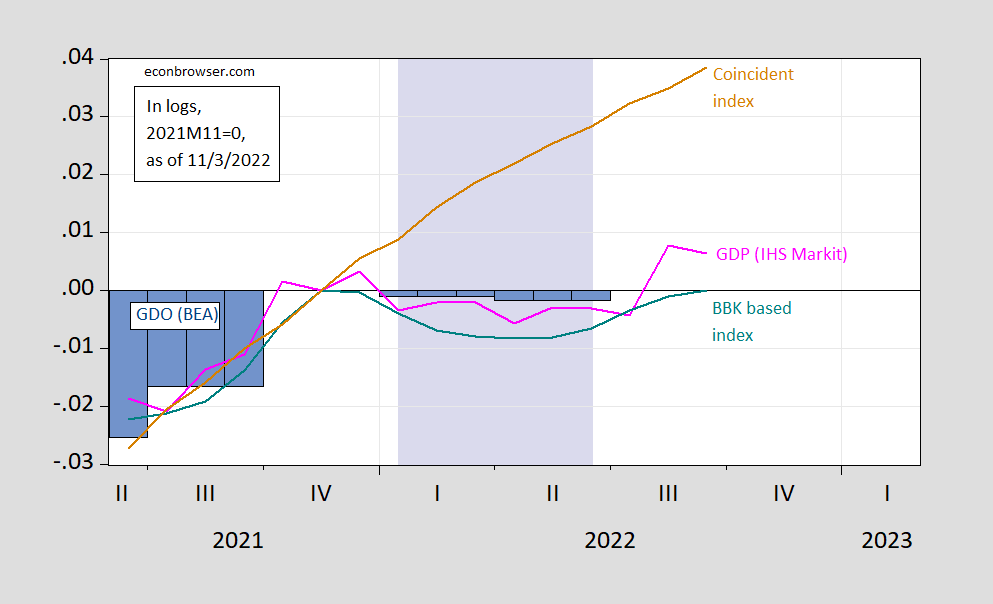

It’s interesting to consider what some alternative measures indicate (including GDOs that the NBER BCDC does consider):

figure 2: 2012 Monthly GDP USD (pink), Brave-Butters-Kelley Growth Based Index (Teal) and Concurrent Index (tan), All logs are normalized to 2021M11=0. The lilac shading indicates a hypothetical recession for 2022H1. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published Nov. 1, 2022), and author’s calculations.

One of the big questions surrounding these pictures is how the employment indicator can be so different from the income/production index (the coincident index is mostly driven by labor market information).

According to this, how about the H1 recession Comment:

1. H1 is a recession by the most commonly used criteria

2. Still, the slump in the first half did not have some of the hallmarks of many recessions, especially the lack of a rise in unemployment

3. This phenomenon was last seen in 1945 when US defense spending collapsed, ie GDP fell without a substantial decline in employment.

4. Therefore, the economic downturn in the first half of the year seems to be explained by aggressive fiscal tightening. Just yesterday, Biden boasted that he had reduced the budget deficit by $1.4 trillion in just over a year. That’s about 7% of GDP, so we might expect a GDP contraction of about 4% (considering potential GDP growth) and that’s what we’re seeing.

5. So, from this perspective, the first half could be considered a “technical recession”, but I’m referring to a formal decline in GDP without an underlying business cycle.

In any event, only a sharp revision in broad production indicators, such as GDP, would be consistent with a recession in the first half of the year.

{kind=link}

{kind=link}