What proportion of the increase in domestic steel prices did tariff increases account for following Section 232 action? Some of the oft-cited estimates relate to the early days of the trade war. With more data, we have more evidence that – unlike tariffs on most other goods – steel has a lower pass rate.

This point was made in a recent working paper Ahmed and Ahmed (2022); from the summary:

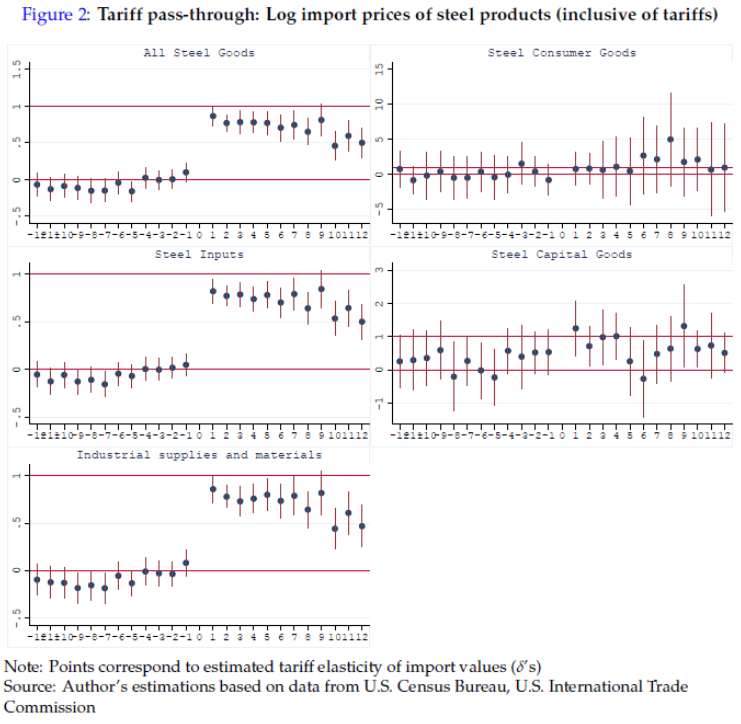

Recent research reports that in terms of higher import prices, the overall burden of tariffs has been entirely passed on to U.S. companies and consumers. However, using U.S. Customs 2018-2019 10-digit import data, we find that import prices for steel products behave differently: First, foreign exporters have gradually lowered their prices, bearing almost 50% of the increased tariffs on all steel products. Industrial supplies and material decisions. Second, the price and import elasticity of consumer steel are significantly higher than 5 and -8, respectively. Third, the immediate increase in the price of industrial supplies was close to 100%, and in the long run, the increase fell back to just under 50%. In the long run, the import elasticity increases to close to 1 over time.

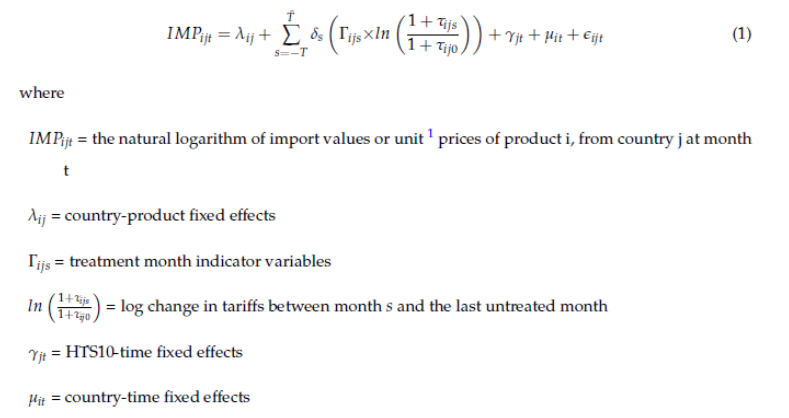

The analysis is an event study using U.S. Customs Department HTS10 figures and country-level monthly import value and volume information, further broken down by end-use categories, namely capital, consumers, industrial supplies, and materials (increase in Equation 1). quantity parameter)

Figure 2 in the paper shows the elasticity estimates for each steel.

resource: Ahmed and Ahmed (2022).

so, Unlike post-Trump import price behavior (Articles 232 and 301) tariffsteel prices exhibit less than full pass-through (echoing Amiti et al. (2020), noted in my previous article postal).

{kind=link}

{kind=link}