in tomorrow's speech Regarding the Phillips Curve and the recent inflation spike in Econ 442, I asked if it could be modified Blanchard Cerutti-Summers (2015) The Philip Curve specification predicts deflation. Answer: Yes.

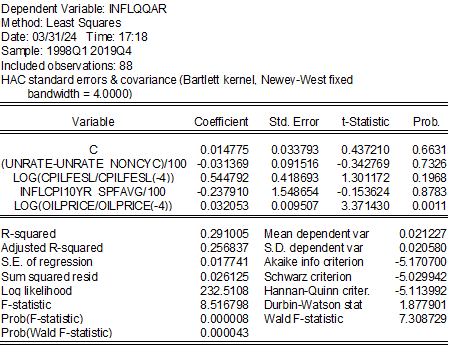

BCS uses:

I modified this by (1) not limiting expected and lagged year-over-year inflation coefficients, (2) using lagged year-over-year core instead of overall CPI, (3) using relative inflation rates for oil instead of imported materials, and/or (4) join the New York Fed Global Supply Chain Stress Index (GSCPI). Then I estimate for 1998-2019 (sample determined by GSCPI availability and avoiding pandemics):

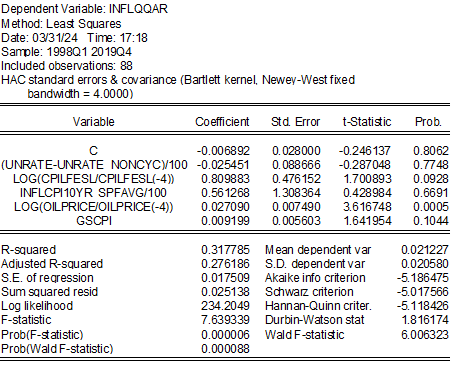

Enhanced using GSCPI.

The unemployment rate gap shows the right signs, although it is not statistically significant. Oil price inflation is quite significant, as is the GSCPI. Note that the effects of GSCPI are from pre-pandemic samples.

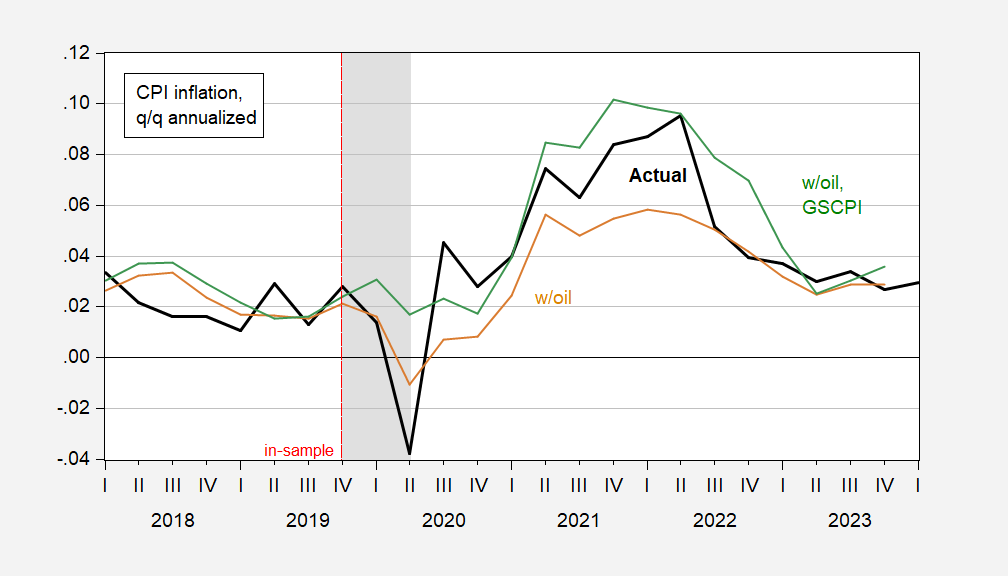

Using these two regressions for out-of-sample prediction, I get the following results:

figure 1: Quarterly quarter-on-quarter CPI inflation in annual terms (bold black) from out-of-sample fits of modified BCS regression (tan) and modified BCS regression augmented with GSCPI (green). NBER-defined recession peak-to-trough dates appear gray. Source: BLS, NBER, and author's calculations.

The mean error (RMSE) of the specification with oil is 1.3% (1.4%), the GSCPI with oil is -1.0% (1.2%), and there are 12 observations from Q1 2021 to Q4 2023.

The fact that the GSCPI augmented equation predicts both inflation and deflation better than the oil indicator alone suggests to me that the unexpected (and to some) continued inflation is due to the supply chain caused by unexpected interruptions.

{kind=link}

{kind=link}