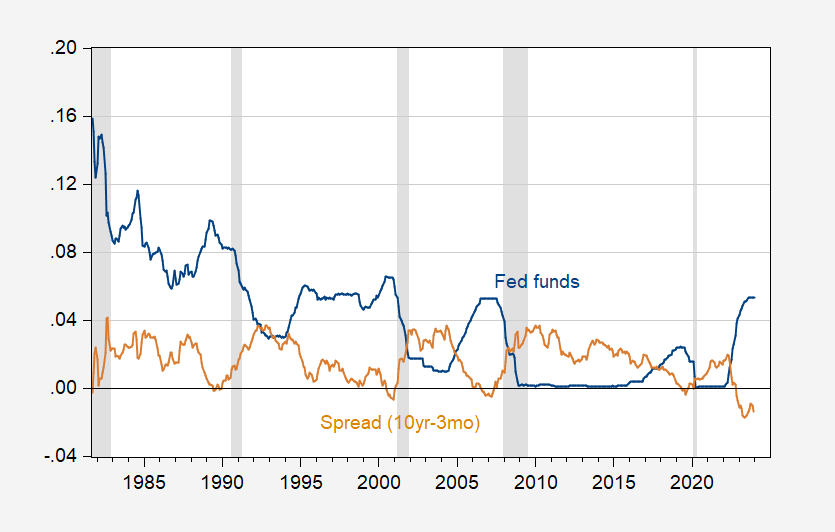

reader Bruce Hall Noting the correlation between peaks in the federal funds rate and recessions, as a contrast I use spread reversals.

Let's compare peaks and reversals:

figure 1: Fed Funds (blue) and 10-Year-3T Treasury spread (tan). NBER-defined recession peak-to-trough dates appear gray. Source: Treasury, Federal Reserve, via FRED, NBER.

Inversions and peaks precede recessions. Which one performs better as a single predictor? I use standard probabilistic regression for evaluation.

figure 2: Recession probits return to the 12-month lead on fed funds (blue) and the 10-year-3-month Treasury spread (tan). NBER-defined recession peak-to-trough dates appear gray. Source: NBER and author's calculations.

The pseudo-R2 for the probit regression of federal funds is 0.07, while the pseudo-R2 for the probit regression of interest rate spreads is 0.27.

Personally, I'll stick with the spread.

{kind=link}

{kind=link}