As of yesterday:

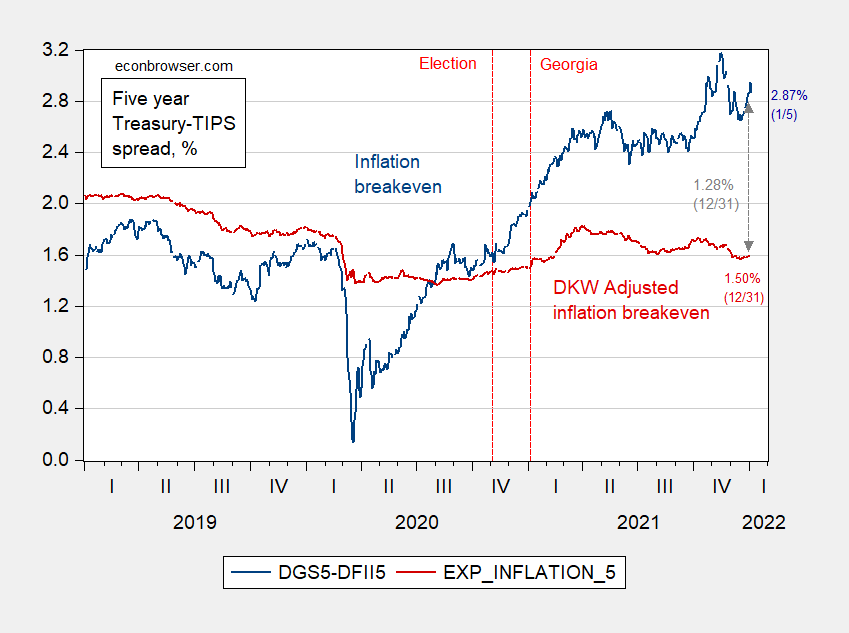

figure 1: The five-year inflation break-even point is calculated as the five-year treasury bond yield minus the five-year TIPS yield (dark blue line). The five-year break-even point is adjusted by the inflation risk premium and liquidity premium per DKW (light blue thin line) ), the five-year five-year forward expected inflation is calculated from the yield of Treasury bonds and TIPS (red), both in %. Source: FRB through FRED, Ministry of Finance, King, Walsh, and Wei (2019) After D’amico, Kim and Wei (DKW) visited on January 6, 2022, and the author’s calculations.

There is a huge gap between the 5-year inflation balance (2.87% as of yesterday) and the adjusted premium estimate-1.28 percentage points as of 12/31.

Figure 5: The five-year expected inflation calculated based on the Treasury bond and TIPS yield (dark blue line), the five-year breakeven point adjusted based on the inflation risk premium and the liquidity premium per DKW (dark red line), are all in %. Source: FRB through FRED, Ministry of Finance, King, Walsh, and Wei (2019) After D’amico, Kim and Wei (DKW) visited on January 6, 2022, and the author’s calculations.

Long-term expectations-the 5-year average in 5 years from now-are declining, and both unadjusted and adjusted are not far from 2% Consumer Price Index (Not PCE).

image 3: The 10-year-3 month term spread (dark blue), the five-year TIPS yield (dark red), and the five-year average expected real interest rate of DKW (pink) are all expressed in %. The decline date defined by NBER is 2/28-4/30/2020. Source: FRB through FRED, Treasury, Kim, Walsh and Wei (2019) following D’amico, Kim and Wei (DKW) interviews on 1/6/2022, NBER and the author’s calculations.

Measures of future economic activity, such as the 10-year to 3-month period spread, indicate a slight improvement in optimism, but it is still not close to the level of earlier this year (such as March 2021). The actual 5-year interest rate has been rising slightly-using the adjusted series last year since the mid-term.

{kind=link}

{kind=link}