I wonder if China’s inflation behavior is abnormal. Answering this question depends critically on (1) what model you believe in, (2) what you think the model parameters are, (3) what you think the input values are, and (4) whether you think the model is stable over time. Here is an answer.

Consider the evolution of CPI inflation in China.

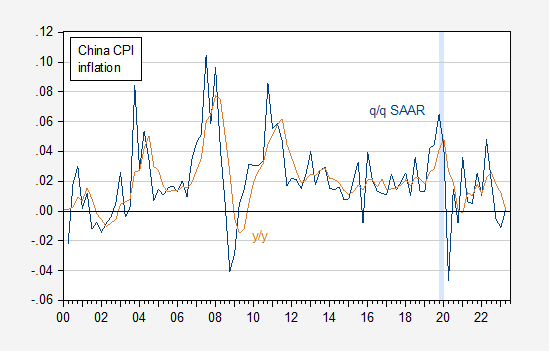

figure 1: China CPI quarter-on-quarter inflation (blue), year-on-year (tan), in log difference. ECRI defines recession dates in light blue. Use X-13 to adjust the CPI. Source: World Bank.

This is the CPI series published by World Bank Kose and Ohnsorge. Seasonally adjust the quarterly series using the X-13 level, then calculate the log difference. A year-over-year series is a non-seasonally adjusted series calculated using the log difference.

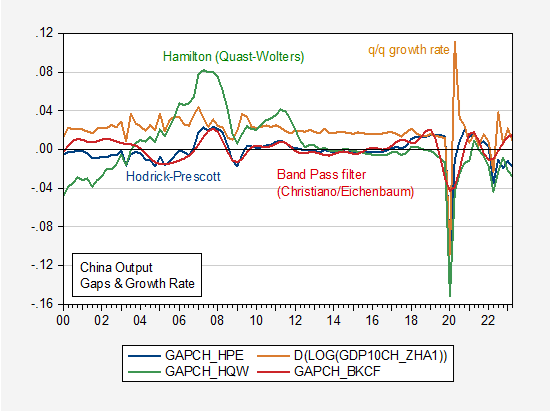

Can the evolution of Chinese inflation be explained by the Phillips curve, both pre-pandemic and post-pandemic? To answer this question requires a measure of the output gap, or some other measure of economic activity. Figure 2 shows the three output gaps measured using statistical methods and real growth in real GDP.

figure 2: HP filtered GDP (blue) on extended sample, bandpass filter (Eichenbaum-Christiano) on extended sample (red), Hamilton filtered (Quast-Wolters) (green), and quarterly GDP growth (tan). Source: GDP from Higgins & Zha/Atlanta Fed, author’s calculations.

- Hodrick Prescott is applying a filter using ARIMA(1,1,0) to GDP data extended by 2 years to solve the end-of-sample estimation problem associated with filters on both sides.

- A bandpass filter is applied to the same extended GDP time series.

- The modified Hamilton filter is the Jim Hamilton filter with h=4 set to 12 instead of 8 following Quast and Wolters (2023)

- Growth rate is the annualized quarterly growth rate of GDP.

GDP data are Higgins and Zha (Atlanta Fed) updates from Q1 2018 based on actual reported growth rates reported by the NBS.

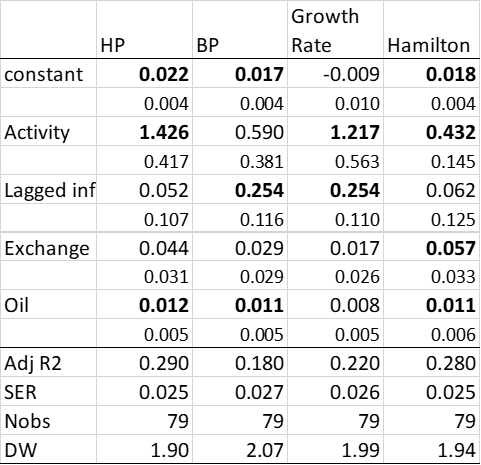

I run quarterly annualized inflation regressions on lagged output gap/growth indicators, lagged trade-weighted nominal exchange rate depreciation, and the contemporaneous change in RMB oil prices between 1Q2000 and 3Q19.

PIt = b + bgapt-1 +c PIt-1 + ΦDqt + FDptOil

The estimated values are shown in Table 1.

Table 1: Determinants of China’s inflation rate

notes: Bold type indicates 10% significance when using HAC robust standard errors.

Note that the gap (or growth rate) is usually significant (except for bandpass filters), whereas lagged inflation is only significant when using a modified Hamiltonian filter. Oil prices always matter.

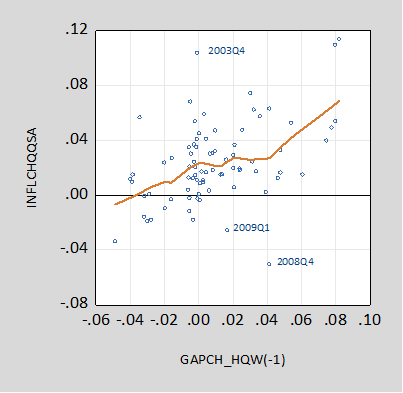

Here’s a scatterplot of inflation (q/q AR) versus Hamilton’s (modified) gap from 1Q2000 to 3Q19:

image 3: Quarter-to-quarter annualized inflation with lagged gap (Hamiltonian filter).

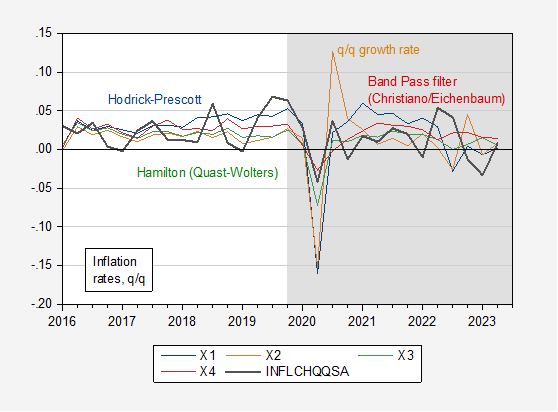

Using these estimates, I projected inflation rates (note that the inflation rates shown below do not match those reported in the media, as they are seasonally adjusted q/q rates). This is a test of the stability of the estimated regression in the post-COVID-19 period.

Figure 4: Real q/q inflation (black), forecast using HP filter (blue), using BP filter (red), using Hamilton filter (green), and growth rate (tan).

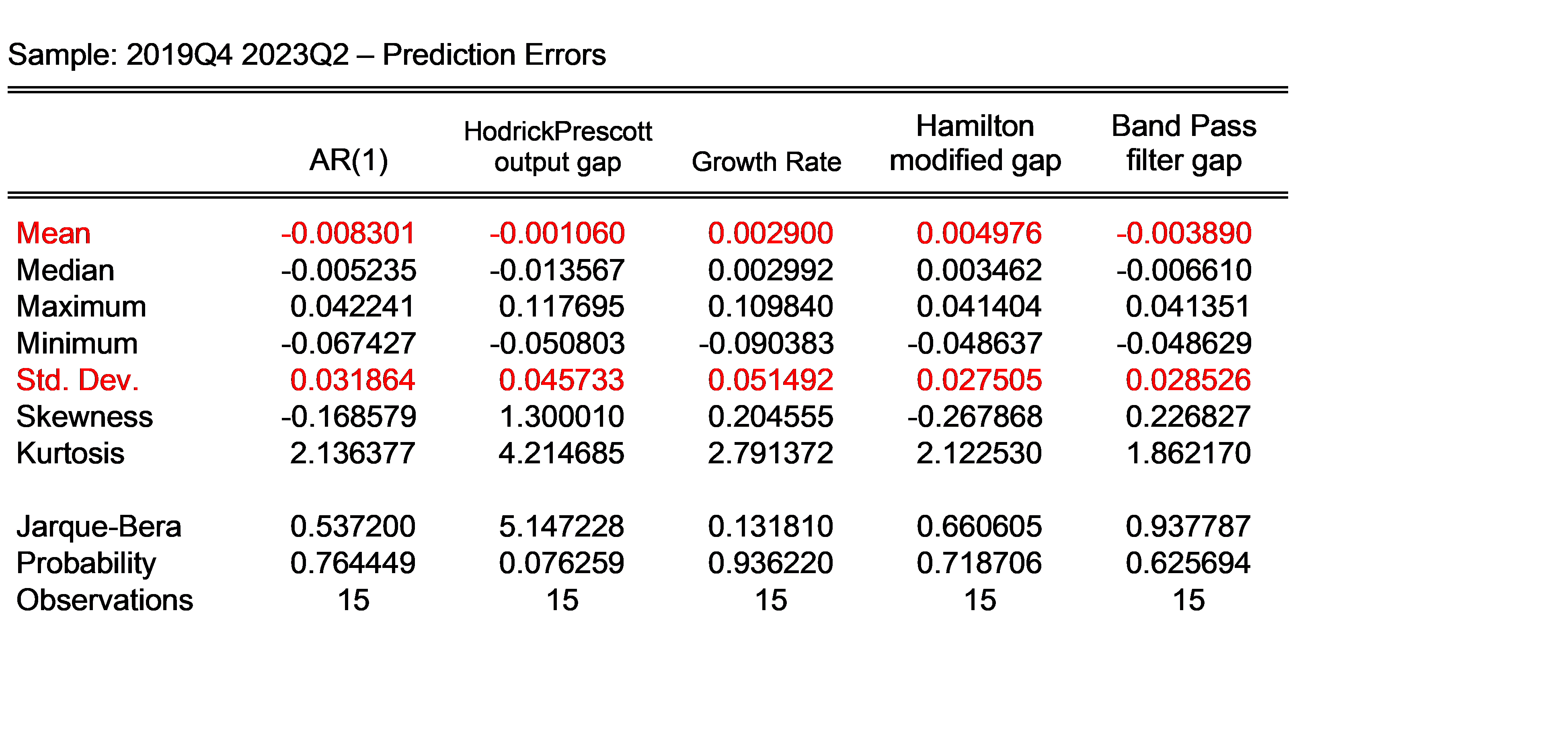

The output gap based on the Hamilton filter yields the lowest RMS error (but the most underestimation).

Table 2: Actual minus forecast

short summary

Indicators of economic activity are positively correlated with inflation after accounting for cost-push shocks, especially oil shocks. Lagged inflation usually does not occur.

{kind=link}

{kind=link}