(As always) Apologies to Shakespeare.from sun woo in Financial Times:

“The entire market knows that there is no deflation in China,” a prominent economist said in response to a question about the risk of deflation at a closed-door meeting in Beijing. “However, we can talk about low inflation [risks]they added, asking viewers to choose carefully which parts of his remarks they report.

“It’s bad if you don’t see me tomorrow,” said the economist.

Now, one might say that, in all governments, economists are not free to say publicly What they think, especially when their views do not align with those of the government. (In my experience in the US government, only policy-level appointees can speak on behalf of the government on issues policy.Regarding data, civil servants are free to discuss data; obviously this will vary across governments, see 2017). But in the current situation, the Chinese government is putting pressure on private sector players (brokers, economists at universities).

There doesn’t seem to be much public discussion about the reliability of price data in China (and I’m not involved in any private discussions), but the numbers look bad enough (from this July 10 post).

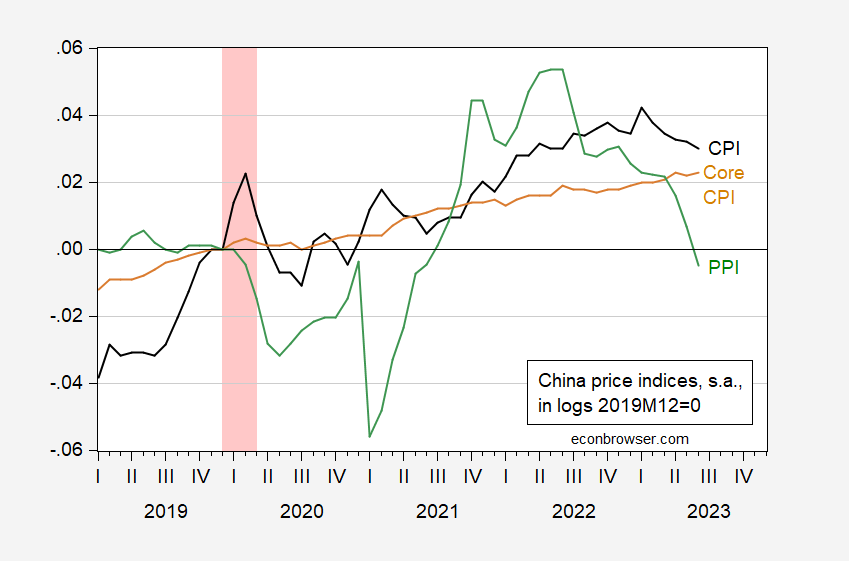

figure 1: China CPI (black), core CPI (tan) and PPI (green), all logarithmic, 2019M12=0. ECRI defines the peak-to-trough dates of recessions as pink. source: Kose/Unworried – World Bank IMF, IFS, both updated using TradingEconomics; and author’s calculations.

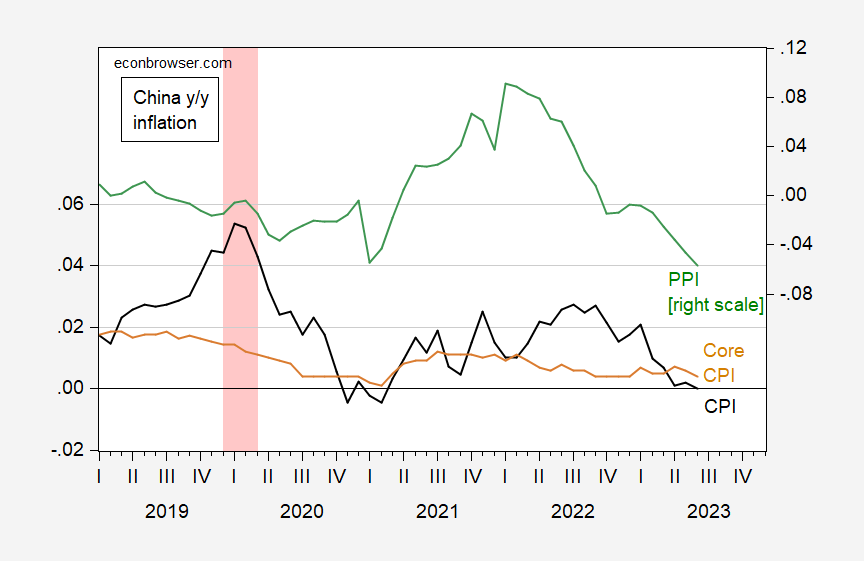

figure 2: Year-on-year inflation rates for China CPI (black), core CPI (tan) and PPI (green). ECRI defines the peak-to-trough dates of recessions as pink. source: Kose/Unworried – World Bank IMF, IFS, both updated using TradingEconomics; and author’s calculations.

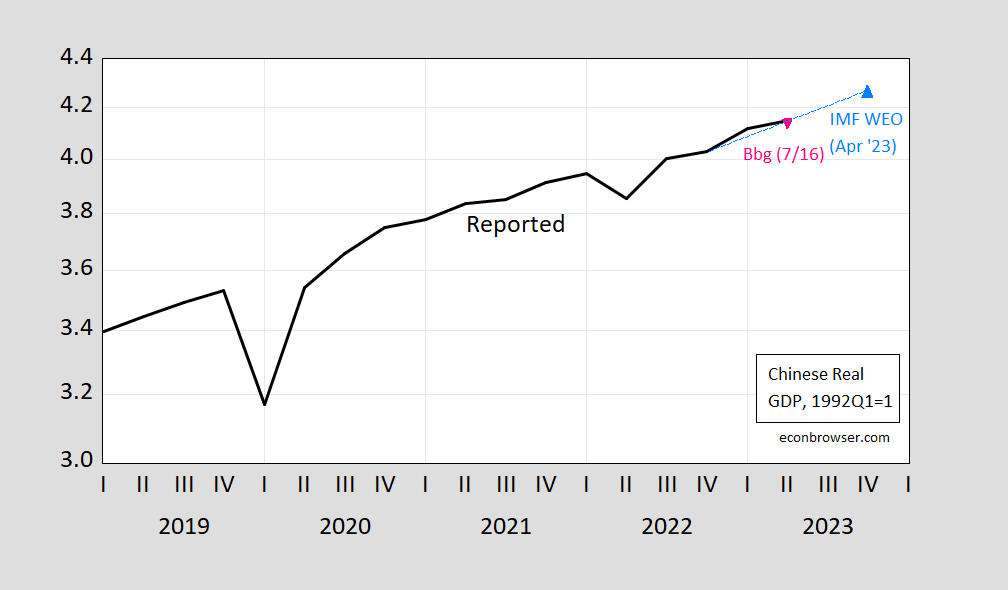

I think I’m also justified in being curious about the GDP numbers given the difficulties I’ve encountered earlier (China in 2021), and others (Fernard, Mueller & Spiegel, 2021 ), checked against various GDP series reported by the National Bureau of Statistics.from Posted on July 16 Regarding the release of GDP and IP.

image 3: Real GDP, Q1 1992=1 (black), Bloomberg Consensus 7/16 (red triangle), IMF April 2023 World Economic Outlook (light blue triangle). Sources: OECD, IMF World Economic Outlook, Bloomberg.

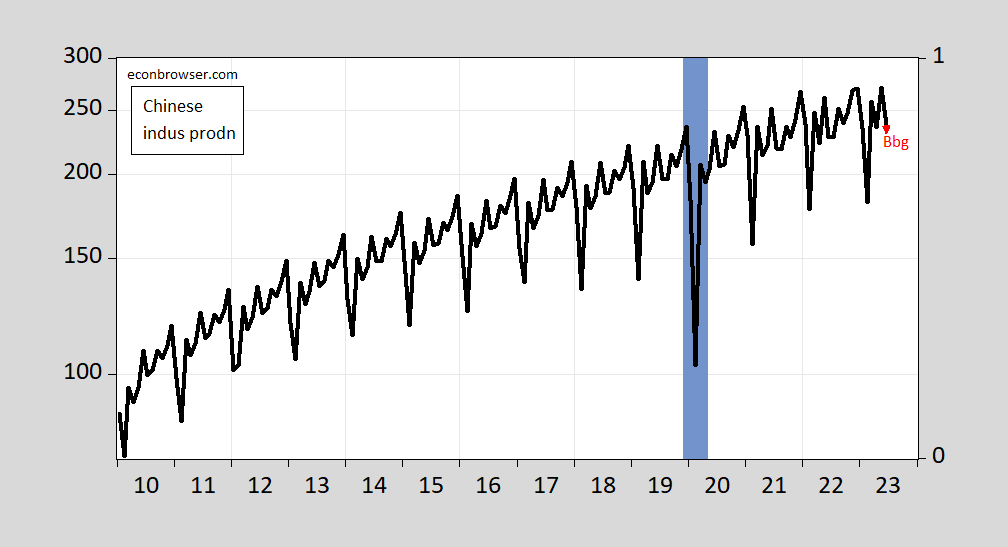

figure 2: China construction ex-industrial production (black), Bloomberg 7/16 consensus (red triangle). ECRI defines the peak-to-trough dates of recessions in blue. Sources: OECD, Bloomberg, ECRI.

Just treat it all as Continuous escalation and suppression of economic information(look Thomas Hale’s recent article in the Financial Times Disappointing economic activity data accelerated this trend (revised and seasonally adjusted black box).

Stay tuned for plausibility of Q2 2023 GDP figures.

{kind=link}

{kind=link}