From conclusion to NBER WP No 29687 (Paper),and Caroline Judd and Christina Jude (both French banks):

FDI flows were particularly weak in the years before the pandemic, while traditional drivers such as growth or historically low interest rates should have supported stronger momentum. This suggests that in addition to those structural factors that normally drive FDI inflows, such as increased economic uncertainty following the global financial crisis, FDI inflows may be hindered. While there is a large body of literature that analyzes the empirical determinants of FDI, empirical analysis of the effects of uncertainty is relatively small, in part due to the lack of consistent measures of policy uncertainty across countries.

In this paper, we examine the role of uncertainty in driving FDI inflows in a heterogeneous sample of advanced, emerging markets, and developing countries in a 25-year pre-COVID-19 sample from 1995 to 2019. By relying on a push-pull framework, we control host country and global uncertainty. Stratifying the sample according to level of development allowed us to discern effects of varying strength and direction across country groups.

Thus, what we find most important for FDI inflows is not host country uncertainty, but global uncertainty. Domestic economic and political uncertainty is generally not statistically significant for FDI inflows. These results hold despite differences in global and host country uncertainty measures.

For emerging countries, host country uncertainty also appears to have a negative impact on FDI flows in some cases, but to a lesser extent than global uncertainty. Domestic uncertainty does not appear to be a significant driver of FDI inflows to advanced or developing economies.

We also highlight the phenomenon of flying for safety when global uncertainty is high or persistent, leading foreign investors to redirect FDI to developed countries that are seen as safe havens.

Finally, our findings suggest that greater financial openness reinforces the negative impact of global uncertainty, confirming the fact that the most affected flows are actually cross-border M&As rather than greenfield FDI.

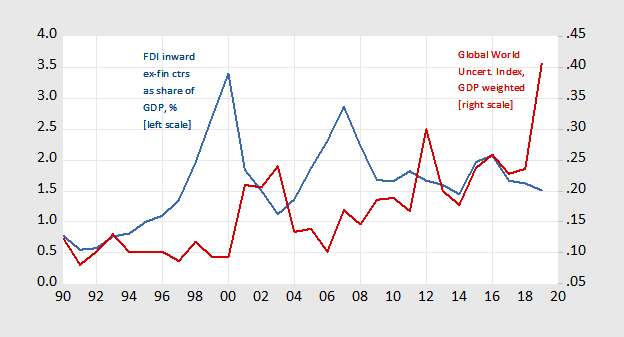

The results are based on a panel dataset, but this time series plot illustrates a key finding.

figure 1: FDI inflows as a share of GDP, former financial centres, percentage (blue, left scale) and global World Uncertainty Index (red, right scale). source: JJC (image 3), Ahir, Bloom and Furceri.

What are the real-world implications? In our baseline specification:

Using group-specific point estimates, we can consider what foreign direct investment inflows would have been if global uncertainty levels from 2015 to 2019 were at 2014 levels (ie, 0.18 instead of 0.41).

…

Our estimates imply a large impact on FDI inflows, which is perhaps unsurprising given the wide variation in assumptions about the level of global uncertainty. FDI inflows to emerging market economies as a percentage of GDP increased by about 1 percentage point, and FDI inflows to advanced economies increased by about 1.5 percentage points.

The non-closed version of the paper is here.

{kind=link}

{kind=link}