Tomorrow we will talk about rethinking the output gap and the concept of trend cycle decomposition in macro policies.Here is the output gap plot from the CBO, from two statistical filters (Hodrick-Prescott and Fleischman-Roberts/Fed Board), and DeLong and Summers (BPEA 1988) Model.

figure 1: Using CBO potential GDP (black), HP filter for 1960-2024 (tan), Fleischman and Roberts/Fed Board 2-sided filter (light green), and pseudo-DeLong-Summers (1988) method (blue) Calculate the output gap. NBER-defined recession peak-to-trough dates are in gray. Sources: BEA 2024 Q1 Advances, CBO (February), Atlanta Fed Taylor Rule utility data as of April 26, 2024, NBER, and author's calculations.

Note that after the Great Recession, the HP filter produced an incredibly small output gap (in absolute terms). On the other hand, bandpass filters such as Baxter King or Hamilton filters that rely on regression methods to extract trends both show large drops and jumps in trends related to the Covid-19 recession (not shown).

CBO’s “production function” approach to estimating trends is unaffected by Covid-19 shocks and is more consistent with economic interpretation. However, it has changed significantly as productivity estimates have changed; recently, Because immigration affects the expected labor stock.

Jim Hamilton There are different interpretations of potential GDP, which rely on differentiated (through specialization) matching of labor and capital supply and demand. Changes in the composition of demand relative to supply can signal weakness. However, I don't have a time series for this potential explanation.

Another way to look at potential GDP is that we cannot take the usual cyclical breakdown of trends for granted. Blanchard, Cerruti, and Summers (2015) Think trends and cycles may be related. They observe that trend growth in GDP typically declines after a recession. From a standard view of the business cycle, this is not a natural outcome. For example, in the Congressional Budget Office's production function approach, a recession affects trend growth only to the extent that lower capital investment and worker discouragement may reduce potential (perhaps by a small amount). In a cross-country analysis, they found that this was not the case.

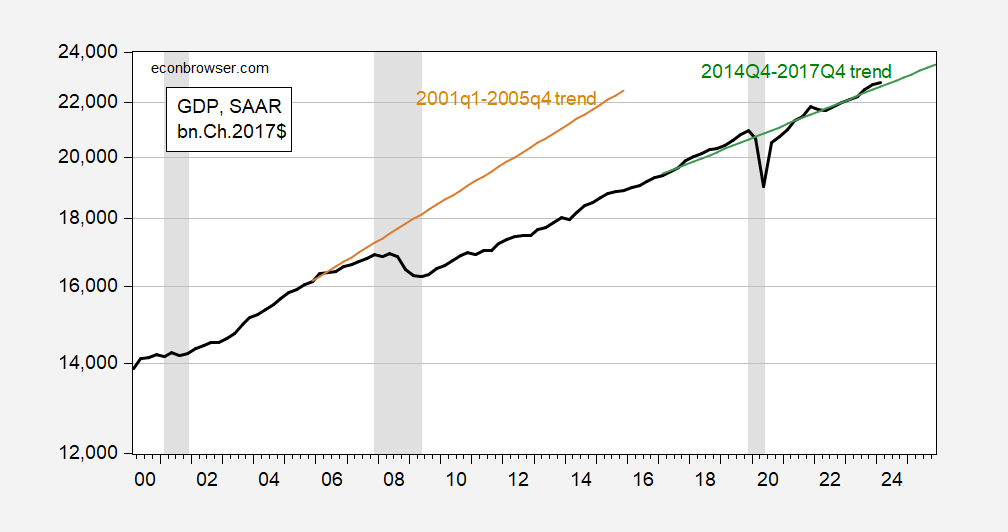

I updated the Blancard-Cerutti-Summers chart for the United States to include more of the late Great Recession and post-2020 recovery.

figure 2: GDP (bold black), linear trend 2001-2005 (tan) and linear trend 2014-17 (green), all in logarithmic scale, in bn.Ch2017$. NBER-defined recession peak-to-trough dates are in gray. Source: BEA 2024 Q1 pre-release, NBER, and author's calculations.

The BCS method shows a significant decrease in both the mean and the trend. Recessions may occur because agents follow conventional wisdom about expected declines in the components of potential GDP (TFP, capital and labor stocks), or because of the trauma of damage to the financial system and, as appropriate, prolonged stagnation in demand .

Interestingly, the 2020 crisis apparently did not have a significant impact on GDP averages or trends. This suggests that either the 2020 recession was not caused by a discrete downward revision of expectations for underlying GDP components, or that swift and forceful fiscal and monetary policy averted the scars.

{kind=link}

{kind=link}