Inflation may not change that quickly, but inflation expectations can change very abruptly — like this week, when a hotter-than-expected CPI number finally pushed the market over the edge and convinced investors to stop expecting a rate cut in March, or five+ rate cuts this year. That relatively small shift in sentiment, with the market already at a high valuation and with high growth expectations driven by the AI mania, created huge selling pressure as traders pulled back quickly after the cute puppy bit them on the hand. About the only stock that could fight through to a “green” day on Wednesday was NVIDIA, which is not exactly a great sign.

Fine for NVIDIA, of course, holy cow has that continued to climb — but probably adds more fuel to the “this is like Cisco in 2000” arguments, and with every huge leap higher for NVIDIA it becomes harder and harder to quiet the voice in the back of my head that says, “this won’t end well.” (And I acted on that voice’s message a little bit… more on that in a moment.)

But then, whaddya know, by the next day almost all was forgiven, and the market was going up again. Woe betide ye who tries to predict the direction of the market in any given week or month.

And we heard from quite a few of our companies this week… starting with one that I sold a chunk of last week, WESCO (WCC), and the market had a pretty wild reaction to that earnings report, so let’s look at that first.

I sold a portion of my WESCO (WCC) holdings last week because I thought the valuation was no longer compelling, and it had pretty well proven my thesis correct over the past three years, resulting in a nice double. As I noted at the time, there were both optimistic and pessimistic scenarios for how it would play out for this stock this year, and I didn’t have a lot of confidence in guessing which was more likely. They are a distributor of electrical and communications equipment, primarily, and those markets are expected to continue to grow over the next five years — so in theory, at least, WESCO has a good growth runway, spending on broadband and electrical infrastructure and large manufacturing projects and data center expansion should continue to go up, incentivized in part by the various government stimulus programs for extending broadband and re-shoring manufacturing, including semiconductor manufacturing.

But as this quarter indicated, it doesn’t go up in a straight line — partly because a lot of that funding has still not hit the end markets, and will be easing out of the government gradually over five years, and partly because the rest of the end markets are not all booming. Perhaps more importantly, the supply chain chaos of the past few years has finally eased, and customers can again get “just in time” shipments of almost anything they need around the world, which means they don’t have to hoard supplies or pay premium prices any longer, all of which benefitted WESCO by front-loading demand and raising end-user prices (and therefore WESCO margins) by at least a little bit during the 2020-2022 period.

And some of the new federal spending, on stuff like broadband expansion, has been really trickling out at this point. CFO David Schulz on this week’s conference call put it this way: “based on customer and supplier input, we don’t expect to see a recovery in broadband until late 2024 before turning to growth in 2025.”

They are still doing rational things — their cash flow is improving, though not as quickly last year as they had predicted, they are getting involved with big projects and customers that are keeping their backlog large and pretty stable (though not really growing, despite the fact that they also said it “ticked up” in January), and they are going to increase the dividend by 10%, a good sign as they enter their second year as a dividend-paying company.

And the stock is probably valued pretty rationally after this post-earnings drop, so the stock is again at ~10X forward earnings estimates… it’s just that those estimates came down from $17 to below $15 this week, thanks to WESCO’s much-lower-than-expected guidance — going from 12X $17 in expected earnings to 10X $15 in expected earnings means a big drop for the share price, even though it was a “value” stock both before and after the announcement.

2023 sales at WESCO ended up growing by 5%, but their gross margin fell and their operating margin fell, and there is no sign of an abrupt recovery being particularly likely. The fourth quarter was particularly slow, with lower sales of their normal inventory items as well as delays in “certain projects” (we’ve all seen that a lot of big manufacturing and warehouse projects have hit delays of late, including the big semiconductor foundry projects in Ohio and Arizona, but WESCO didn’t call out a specific project).

And they expect 2024 to bring growth on the top line, but just barely, the forecast is for slower growth than 2023 — they’re guiding investors to expect 1-4% sales growth, so they are either “guiding low” or they really don’t see a surge in government spending hitting their customers… or at least, they don’t see it being high enough to offset slowing demand in other areas, like OEM and broadband and general construction.

So they’ve been spending more on SG&A (which is mostly “people”), and they’re seeing their gross margins slip as suppliers offer fewer discounts and end users are more price conscious and less likely to over-order or hoard supplies. They did end up with $444 million in free cash flow last year, which was in improvement on past years but lower than the $600 expected… but most of it came in the second half, and they are predicting $600-800 million in free cash flow for 2024, which would mean that a LOT more of their predicted earnings are real cash earnings — $700 million would be $13.72 per share in free cash flow, and WESCO’s adjusted earnings guidance for 2024 is now that they will be in a range of $13.75-15.75 per share. So that would mean “higher quality” earnings in 2024 than they had last year… but also perhaps lower earnings.

The short answer here is that both the 2023 earnings and the 2024 earnings guidance from WESCO came in roughly 15% below what was expected by analysts, and indicate that the adjusted earnings per share will probably at best be flat over the coming year, and could decline for the second year in a row. And that does not assume any kind of real big-picture economic slowdown or recession, of course. There’s likely to be a fair amount of skepticism from analysts about how effectively WESCO can predict their financial results in any given year, since they came in well short of the guidance they had provided last Spring and Summer. It may not be reasonable to judge them for being far off in predicting their sales, margins, earnings and free cash flow during a period when those things are pretty far off — but they still made the predictions, and included a pretty wide range, and missed that range completely.

It was reassuring to see that pretty specific outlook at the time, too, as I recall, so I don’t blame analysts for following that guidance — it seemed reasonable and rational, particularly after they cut it in August, but here’s how things have gone for WESCO over the past year:

A year ago, in February of 2023, their 2023 outlook was: 6-9% sales growth, $600-800 million in free cash flow, $16.80-$18.30 in adjusted earnings per share. They repeated that guidance in May, sales growth was great at that point, though cash flow wasn’t coming yet and they said to expect that to be late in the year, all was sunny and bright.

Six months ago, in August, they downgraded the guidance after a weak quarter — their new 2023 outlook was: 5-7% sales growth, $500-700 million free cash flow, $15-16 adjusted EPS. Bad news with the big drop, but still solid numbers for what was then a $170-180 stock (~12X earnings, still expecting to grow earnings for the year).

November brought reassurance with the third quarter results, with good free cash flow generation (most of the cash they generated in 2023 came in that quarter), and some buybacks and talk about optionality and strong execution, along with cost-cutting and improving margins. The actual quarterly earnings were flat with the year-ago quarter, and they did warn that October sales were starting out slow, but they RAISED the guidance — sales growth would come in at 5% for the year, they said, not the 5-7% previously guided, but they stuck with $500-700 million in free cash flow and they raised the earnings forecast, to $15.60-16.10. Analysts obliged by putting their forecasts near the top end of that guidance range, at about $15.90, as you would expect. Analysts almost always do as they’re told.

And after what must have been an ugly end to the year for them, sales growth for the year ended up being only about 3%, free cash flow ended up at $444 million and the actual earnings per share came in at $14.60.

So that’s the challenge, really — do we have any trust in their earnings guidance, or in their ability to control their margins or their costs in an uncertain sales environment, given their way-too-optimistic forecasts over the past year, including that “guidance raise” just three months ago, in November?

They certainly recognize the challenges, and talked a lot about how that fourth quarter was “unacceptable” on the call, and that they will be more assertive in cutting costs to match their lower sales, but it’s also true that they don’t have a lot of control over what the demand environment looks like among their customers, or when sales will come through.

Here’s how they described the challenge, this is CFO David Schulz on the call:

“Like the third quarter, growth in utility, industrial, data centers and enterprise network infrastructure was more than offset by declines in broadband, security, OEM and construction. We experienced customer destocking in our shorter-cycle businesses in the second and third quarters. In the fourth quarter, we saw a step-down in demand versus our expectations, particularly in December….

“As we moved into the fourth quarter and as we mentioned on the earnings call in early November, we expected to see an acceleration of sales from October to November and again into December, primarily driven by the shipment of projects from the backlog.

“Instead, we experienced a further slowdown in our stock and flow sales, along with some project delays, primarily within our CSS business. We were expecting organic sales to remain flat and instead, they were down approximately 3%.”

And things have not bounced back yet, which is why the guidance was so surprisingly low — they said that they continued to see sales declining in January, though from their comments on the conference call the backlog did “tick up” to start the year.

I’m not in a hurry to get rid of my WCC position, and they’re now down to a valuation of only about 10X their expected free cash flow for 2024 (or if you want real numbers and not company forecasts, 17X their free cash flow in 2023), but I’m more likely to sell down my position further than I am to buy more — as I noted last week, this was never a position that I considered to be a “high quality” or “forever” stock, I bought with the intention that this would be a 3-5 year trade on realizing value from their Anixter merger and benefitting from increased electrical and telecom infrastructure spending. We’ve got the merger value realized now, that three-year integration is complete and was successful, with their “synergy” targets all exceeded and the debt slowly beginning to come down (the used debt to buy Anixter, which was good for shareholders, partly because debt was very cheap back then, and have claimed great ‘deleveraging’ since, though that mostly means their cash flow covers the debt level better, thanks to growing earnings since the merger, not that the actual debt level has come down). Still, though, much of the expected demand growth has not yet really materialized in their end markets, though they still expect “secular growth” in these areas and it should be true that government incentive spending is still on its way… we’ll see how things settle down after this abrupt drop.

Here’s what I said back in August, when they were getting the shock of a downward reset in expectations for 2023 (now downward enough, it turned out):

“I lean toward having some confidence that the business is likely to plateauing, not collapsing, and that there is room for some margin improvement and a resumption of some reasonable low-single-digit revenue and high-single-digit earnings growth if we don’t go through a major down-cycle in the economy, generally speaking. Given a variety of uncertainties, now that they’ve “missed” two quarters in a row and that’s likely to lead to more analyst and investor caution, particularly as they start to talk more about repaying their first tranche of debt (in 2025), I’ll pencil in a lower “preferred buy” now — over the past decade the bottom has been roughly 8X earnings, and if we use the lower company forecast for 2023 earnings ($15.50) instead of the higher trailing earnings ($16.42 in 2022), that gets us a much lower “preferred buy” level of $124. I don’t know if the stock will fall that far, mostly because I don’t know whether they’re disappoint again next quarter, but it’s a good number to look for. That would also be about 10X free cash flow, which is rarely a bad price to pay unless the company is in perpetual decline, and I don’t see any reason to expect that’s the case here.”

Well, that free cash flow hasn’t quite shown up yet — but if they’re right in projecting at least $600 million in free cash flow for 2024 (their range is $600-800 million, so, to be fair, the forecast is really $700 million the way most of Wall Street thinks about those things), then 10X free cash flow would be $6 billion, or just about exactly $117 per share. They’re now forecast to earn $14.67 in 2024, given the lowered earnings guidance, and 8X that would also be about $117. I’ll bump down the “preferred buy” to that level (it was previously $124). I’ve held the “max buy” at 11X earnings recently, and the lowest number we have available on that front, the forecast of $14.67 per share in earnings for 2024 (trailing GAAP earnings for 2023 were down to $13.84, but adjusted EPS came in at $14.60 last year, too, roughly the baseline level they now expect for this year). That would set “max buy” at about $160, so that’s probably about the most you’d want to pay if WCC is going to grow at about the rate of inflation, pay a growing dividend, and buy back some shares. The stock could go higher, of course, but that depends on people believing it to be a growth story again — or on proving out the growth potential over the next couple years.

WESCO believes they’re a brand new company, and have come through a wild period of dramatic shifts in the supply chain but are now back on track with roughly the trend they were on pre-Anixter, in 2019… and that year, they traded in a range of about 8-11X earnings, too. Maybe that’s the rational level if they can’t improve their margins or become more of a value-added distributor, we’ll see.

For me, I’m willing to be somewhat patient and I don’t often go “all in” or “all out” on a company in one fell swoop, but I think the growth potential for WCC is not particularly compelling, and it’s probably near the top end of what a rational valuation might be if they’re not going to grow, in the 10-11X earnings range. It’s a better company than it was pre-Anixter, but it’s got the same management team, we’ve reaped a good chunk of that reward already, and I’m not seeing a lot from management that makes me change my mind about this being a shorter-term trade in a company that has been historically mediocre.

And this is what I said back in that August update about my big picture expectations:

As was the case a quarter ago, I think WESCO in the $120s and $130s is a pretty clear buying opportunity for the 2-4 year infrastructure spending cycle we should be starting right now… and if you think we can do that without a meaningful industrial recession in the US, then you can pay more. I’m just a little less confident about the high end numbers I was using six months ago, particularly after two quarters where the business has been hurt worse than management expected. I was contemplating lightening up this position a little bit after seeing the initial numbers, since this is currently a max allocation holding for me (about 4% of my individual equity commitment is to WCC), but after going through the financials more thoroughly and listening to the conference call, I feel a bit more reassured about the 2-3 year prospects. I’m holding.

That ceased to be the case a week ago, as I sold a quarter of my shares… and following the last two quarterly updates and their new outlook for 2024, which indicates no real expected growth or positive outlook in the next year, and no sign that the gradual progress of Federal stimulus is going to be enough to offset slowness in other parts of the business, I’m back to “less assured”. Expecting single-digit earnings growth during a period of stimulative spending seemed reasonable, particularly given how long it has taken for that stimulus to actually become spending, but now that six more months have passed, and more projects have been further delayed than have moved forward and become orders, I don’t like the trajectory.

If we’re looking at zero growth and a low valuation, as now seems more likely, then I think we have some better companies to consider these days, so it might make sense to choose one with a stronger brand, or a historically more profitable business that provides more upside potential and the likelihood of margin expansion in the future. Deere & Co. (DE) comes to mind from our watchlist, since that’s a global leader whose earnings have stagnated of late and driven the valuation down to about 10X trailing earnings, a similar current valuation to WESCO, with both offering a weak 2024 forecast this week. I think it’s more likely that Deere will eventually recover and create value for investors again, despite the current projection that their earnings will dip about 20% this year and then recover slowly from that point, than I am that WESCO will show meaningful earnings growth and reach a higher valuation in the next couple years.

So I sold another chunk of my WESCO shares today, half of my remaining stake, at just over $150, now that I’ve had some time to think it over, the market has evened out some of the initial overreaction to the bad quarter, and my trading embargo from last week has lifted. I’m more likely to continue to sell down that position over time than I am to buy more, but I’ll try to keep an open mind. That’s enough to guarantee a profit for this position, since I’ve now taken out about 10% more cash than I put in, which is why it shows up with a negative adjusted cost basis in the Real Money Portfolio spreadsheet.

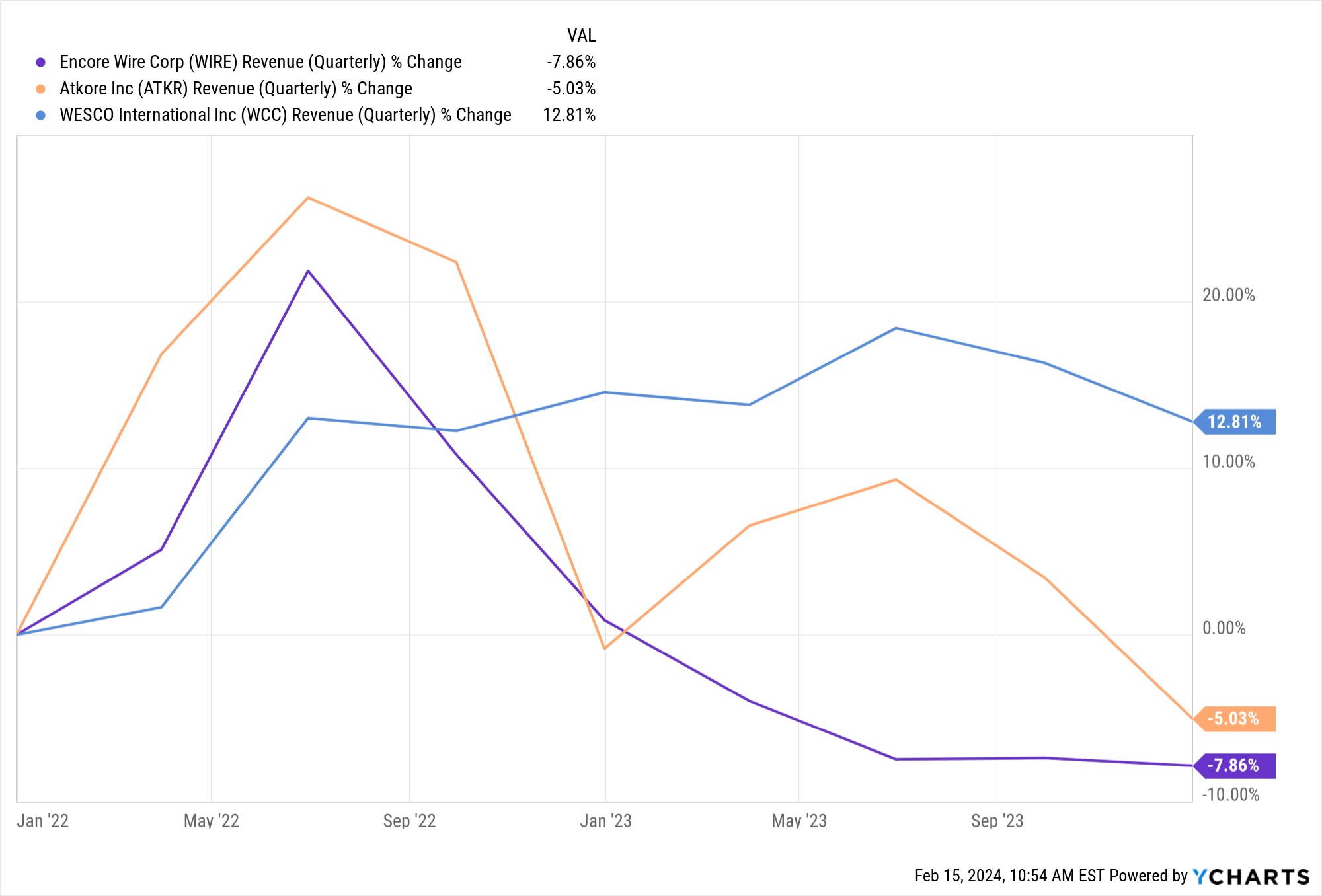

Incidentally, Encore Wire (WIRE), which like Atkore (ATKR) is a manufacturer and supplier of equipment into these same industries (ATKR mostly sells conduit, WIRE mostly sells copper wire, both are profoundly impacted by commodity prices), had a better quarter than WESCO — their CEO said, “Our team shipped a record number of copper pounds in the fourth quarter due to consistent strong demand for our copper wire and cable products, representing the strongest volume quarter over the course of the full year. Our ability to capitalize on this demand and deliver unmatched speed and agility in serving our customers is a testament to our single-site, build-to-ship model, an important competitive advantage. We experienced sustained, increased copper wire and cable demand from mid-2023, which continued through the fourth quarter.”

Still, though, because of shifting commodity prices, that volume growth did not lead to revenue growth — this is what the revenue of all three of those companies has looked like over the past two years, they all surged in 2022, largely due to the pricing and demand picture benefitting from the supply chain disruptions, but have been been drifting down over the past two quarters as that normalized:

*****

Then we got into a bunch of mostly high-growth stocks reporting this week, where results are supposed to be a lot more volatile (unlike WESCO, which you wouldn’t think should be prone to these dramatic 25-30% post-earnings moves, but has sometimes, including this week, bounced around like a jumpy tech stock).

The Trade Desk (TTD) had actually a slight earnings “miss” last night, analysts had overestimated earnings by a few cents… but they guided for (continued) big revenue growth in the first quarter, the revenue guidance was about 6% higher than the analyst estimates, which would mean year-over-year revenue growth of at least 25% next quarter, and that got everyone excited, with the stock instantly popping almost 25% higher after earnings last night (since settled down to a ~18% gain or so).

That’s awfully nutty, of course, it’s tough to argue that the earnings result, solid though it was, meant that suddenly TTD became almost $10 billion more valuable, and it came back down quickly after that overreaction, but suffice to say that TTD investors were pleased. The actual adjusted earnings for the quarter came in at 41 cents, roughly the same as the analyst estimate, so that was 23% earnings growth for the quarter, and revenue came in at $605 million, about 4% higher than the forecasts and, as happens with pretty much every fourth quarter, that was their best quarter ever.

This is so often the game with The Trade Desk — it’s been a great growth company since inception, with excellent revenue and earnings growth almost every quarter, and clear scalability as their ad buying network, data and software solution has continued to attract more ad buyers, leavened by the fact that they’re one of the worst offenders in the “stock-based compensation” category. The stock tends to react violently to forward guidance, so it dropped 20% when they offered weak guidance last quarter… and then surged this quarter when they beat that guidance and offered what was seen as optimistic guidance for 2024. The cash picture has steadily improved, and they’re starting to grow enough to begin to offset their huge stock-based compensation, but the valuation is still very rich, no matter how you look at it.

I still like Jeff Green, and he has been consistently clear and pretty accurate with his outlook on the state of the advertising market — the conference call is always worth listening to, but here’s how he says things are going now:

“While there is much to celebrate about 2023, I’m even more excited about 2024 and beyond. I’ve never felt more confident heading into a new year. I believe we are uniquely positioned to grow and gain market share, not only in 2024 but well into the future, regardless of some of the pressures that our industry is facing, whether it’s cookie deprecation, growing regulatory focus on walled gardens, or the rapidly changing TV landscape….

“Often people looking at our massive global industry continually overlook significantly different strengths, weaknesses and opportunities for different types of companies. Some wrongly think only big companies win, and smaller companies like us don’t. That paradigm is completely wrong. In general, the current shifts will help companies with authenticated users and traffic, which also sit next to large amount of advertiser demand.

“These macro changes hurt those, especially content owners and publishers who don’t have authentication. So this year, CTV and audio have big opportunities ahead, and the rest has pockets of winners and losers. But nearly everyone will be either better off or worse off. And I believe 2024 is a year of volatility for the global advertising market. And for those who are prepared, like The Trade Desk, it is an opportunity to win share. Our platform is set up to make the most of any signal that can help advertisers drive relevance and value. Our platform now sees about 15 million advertising impression opportunities per second. And we effectively stack rank all of those impressions better than anyone else in the world based on probability of performance to any given advertiser without the bias or conflict of interest that plague most walled gardens.

“With UID2, Kokai, and advances in AI in our platform, we now do this more effectively than ever before. And our work in areas such as CTV, retail data, and identity are helping build a new identity and authentication fabric for the open internet. So, regardless of how the environment evolves around us, we will always be able to help advertisers find the right impressions for them.”

So TTD continues to grow a little faster than the overall digital ad market, as it has mostly done for years, and management is very optimistic about the coming year — they’re usually optimistic, but I’d say that they were qualitatively more so this time around. They also increased their buyback authorization to $700 million, though that’s not hugely meaningful — at best, we can hope that they’ll use buybacks to offset most of the stock-based compensation.

This is a stock where the scalability is so clear that I’m willing to pay a stiff premium valuation, and have grudgingly accepted the use of “adjusted” numbers that ignore stock-based compensation, since the market has pretty clearly signaled that it doesn’t care about that at all. The scalability comes from the fact that they get a slice of each dollar spent on their platform, but primarily sell software and data, which are inherently scalable once the R&D and sales costs are absorbed, so earnings growth should outpace revenue growth pretty significantly over time.

But I also generally hold out for bad days to buy TTD, it’s not a stock I’ve often been able to justify when things look rosy and investors are excited. The level I look for as a “max buy” with TTD has been 40-45X forward adjusted earnings, tied to what I see as very likely and sustainable average earnings growth of 20% going forward — analysts haven’t yet updated their forecasts for 2024 earnings, but I’d guess that those estimates will be bumped up to somewhere in the $1.50-1.55 range, perhaps a little higher (they were $1.45 before the conference call). The most optimistic number I can justify is 45X forward adjusted earnings, so that’s now $69… and it’s a lot easier to justify something like 30X earnings, which is typically my “preferred buy” level for this stock, so that’s about $47. TTD is very volatile, as befits a stock that currently trades at 25X revenues, a level very few companies have ever been able to justify for long, and it’s very likely that investors will find something to worry about and we’ll see sub-$70 prices again at some point… but, of course, there are never any guarantees about the future.

And if you’re looking for a reason to be cautious, stock-based compensation remains nutty, prior to this quarter TTD was using new share issuance to cover roughly a third of their total costs (including the cost of goods, SG&A expenses, all the operating costs). A big slice of that goes to Jeff Green personally, but it’s a huge number overall — stock-based compensation was recently running at about $500 million a year, and total revenue for 2023 of $1.95 billion. That’s why GAAP earnings for last year were $0.36, while their adjusted EPS came in at $1.26. Their buyback authorization might heal some of the dilution that comes from this, and it puts their surplus cash to work, but it’s really more like capitalizing payroll — it makes sense as a business owner if investors are willing to ignore it, and if it incentives your employees to do well, but it’s not exactly a clear way to account for your operating expenses. It used to be that almost every tech company focused on their adjusted earnings, but now, at least, most of the big guys (Alphabet, Apple, Amazon, etc.) have stopped reporting adjusted earnings and have gone “all in” with GAAP and accepted that stock-based compensation is an expense, not a way to create “free” labor. TTD will probably be embarrassed into joining them at some point, but maybe not soon — if we’re lucky, they’ll have growth that overwhelms this issue and makes it moot, as happened with NVIDIA, another serial abuser in the stock-based compensation space, over the past year, with NVDA finally seeing its GAAP earnings come close to catching up to “adjusted” earnings.

*****

Roku (ROKU) results were about as expected, with revenue slightly higher than forecasted. Active account growth was strong in the fourth quarter, as expected (lots of new Roku users with new TVs), and streaming hours continued to grow, but the bad news was that they had another decline in average revenue per user (ARPU), with that number dropping below $40 for the first time in a couple years (it had been in the low $40s since mid-2021, after a period of dramatic growth through the early days of the pandemic), and their guidance was not particularly optimistic — kind of the flip side of TTD, and both do have some common drivers since they both essentially ride on the back of the advertising industry, with particular exposure to the migration of ad dollars from linear TV to streaming TV (though ROKU is far less easily scalable, and arguably has stronger and more worrisome competitors rising). They were also the flip side of TTD last quarter, when TTD disappointed and ROKU excited investors with their ongoing cash flow recovery and some bumps up in their key performance indicators (like that ARPU number) which have turned worrisome again now.

That weaker outlook presumably did a lot to cause the big drop after hours last night, when I glanced at the ticker it was down more than 15%, in the high $70s, and it got worse as the morning trundled along, so it’s now around $72. ROKU has not been able to make that leap into real profitability, though it is improving on that front with more cost cutting, so without any kind of profit number to lean on, there’s not much of a foundation for the stock when sentiment shifts. The stock has bounced around quite a bit with those sentiment changes, it has seen both $50 and $100 over the past year.

The cost-cutting they’ve talked about has been working, though it required reducing their R&D spend, which might be worrisome when it comes to holding their market share in the future, and their devices gross margin was still negative, but much less negative than the previous holiday season (they’re willing to sell devices — TVs and streaming boxes — at a loss to build the user base), and the core platform business did pretty well, with 13% gross profit growth over the year ago period as ad revenue picked up a little (“platform” means advertising and sales commissions for streaming services, mostly), but it didn’t grow as fast as the active accounts or the streaming hours, or the digital streaming market as a whole, according to The Trade Desk, so they’re not getting much leverage to the scale of usage of Roku TVs at this point. They did end the year with two quarters in a row of positive cash flow and free cash flow, and positive Adjusted EBITDA, though that was to be expected with the advertising recovery and their cost cutting.

I find the market outlook for Roku more worrisome than I did in past years, because competitors have finally begun to get some traction in building out competing operating systems for smart TVs — ROKU is still the leader, but Amazon is closing in, and Walmart is rumored to want a larger role in this space as they think about maybe buying Vizio, a TV maker who has persisted in building its own operating system (though it’s still trivially small, so probably needs a bigger partner to get any advertising traction). Roku’s system is still better than the competition, and is much stronger among lower-income consumers because of their superior “free TV” offerings, which should give them a little more exposure to advertising spend… but the competitors who Roku lapped last time in taking control of this market a decade ago have not given up, and they’re coming back for another battle.

The big difference between last quarter and this was just the level of optimism in the outlook — last quarter they were on the way up, and they overshot analyst estimates and told analysts to increase their numbers… this quarter they still beat those numbers, but effectively told analysts to bring their future numbers down a little — this was how they stated their guidance this time:

“We plan to increase revenue and free cash flow and achieve profitability over time. At the same time, we remain mindful of near-term challenges in the macro environment and an uneven ad market recovery. While we will face difficult YoY growth rate comparisons in streaming services distribution and a challenging M&E environment for the rest of the year, we expect to maintain our Q4 2023 YoY Platform growth rates in Q1. This will result in Total net revenue of $850 million, total gross profit of roughly $370 million, and break-even Adjusted EBITDA in Q1. Continuing our performance from 2023, we expect to deliver positive Adjusted EBITDA for full year 2024.”

2023 was better than 2022, and 2024 should be better still… but it still won’t be nearly as good as 2021, when the streaming wars and COVID lockdowns turned Roku into a profit-generating machine. I think they’re going in the right direction, and I’m willing to be patient as we see if they can hold on to their market share with their new TVs, partly because I’m really impressed with the way that Roku came out of nowhere to beat Apple, Alphabet, Amazon and so many others in this space the first time around, and I like the aggressive goals of founder/CEO Anthony Wood… but I don’t need to make this a larger position, not while we’re still waiting to see how streaming television evolves and where the profits end up settling. I’m keeping my valuation numbers the same for ROKU, given the failure to grow ARPU this quarter, so “max buy” stays at $68, “preferred buy” at $46, and this remains roughly a 1% position for me… small enough to comfortably absorb the volatility and continue to be patient. I still like the business, but I don’t see any objective reason for the numbers to improve dramatically this year.

*****

Kinsale (KNSL) reported another walloping beat of the earnings estimates, they had $4.43 in earnings per share in the fourth quarter, so that’s 53% earnings growth… and for the full year, that meant $13.22 in earnings, which was just shy of 100% growth (analyst had forecast $12.04). They had very low catastrophe-related claims in the quarter, which was common to most of the insurance companies I follow, and the quarter had a combined ratio of 72.1%, which was enough to bring the full-year ratio down to 75.4%. Remarkable profitability and growth for an underwriter, which is, of course, why it trades at a much higher valuation than pretty much any other underwriter. Thanks to higher interest rates, the investment income that was essentially a rounding error in 2022 doubled in 2023, so it’s beginning to become a real contributor (underwriting income was $270 million for the year, investment income $102 million).

You might say that $10 billion (Kinsale’s market cap) is a lot to pay for an insurance company with a little over $300 million in net income, and you’d be right — KNSL is trading at a little over 30X earnings these days and more than 10X book value, a rich valuation, roughly twice that of the second-richest-valuation among relatively large insurance companies (that would be Progressive, which is at about 5X book value and 28X earnings)… but it’s also clearly separated itself from the pack, performance-wise, over the past couple years. Excess & Surplus lines insurance, which is all Kinsale does, is getting more important as more regular insurers drop coverage of certain business lines or geographic areas and as risks get more unusual, and Kinsale clearly has a huge advantage in the way they price and sell their coverage. Nobody else seems to be even close, and Kinsale still has less than 2% of the E&S market, so there should be opportunity for them to continue to grow.

It’s not going to get less risky, though — there’s a reason why insurance companies (almost) never trade at these kinds of valuations, and it’s mostly just that they are in the business of judging and taking risk, and sometimes they get surprised. Kinsale is doing incredibly well, but we shouldn’t assume they are perfect — something could dramatically upset their underwriting and make it clear that they wildly mispriced a risk, and there could be a point where they lose quite a bit of money. Hasn’t happened yet, and they shouldn’t have a lot of long-tail risk compared to some insurers (who have reserves to cover policies they wrote decades ago, in some cases, as risk perceptions change or new liabilities appear), but while I have accepted that Kinsale clearly has built an edge, and can be valued like a growth stock, I also keep my allocation somewhat limited because there is the looming risk that something surprising could upset their black box risk calculations… and, of course, the risk that investors will change their mind after a bad quarter, and decide Kinsale doesn’t deserve to trade at a huge premium to the other E&S underwriters. This strong quarter brings Kinsale almost back to those all-time highs they hit back in October, just over $450.

I pencil in 25X forward earnings as my “preferred buy” level for Kinsale, and 40X trailing earnings as the “max buy”. With $13.20 now in the books for 2023, that would be a “max buy” of $528 — that seems ambitious, but it’s likely to be OK as long as Kinsale can keep growing revenue and earnings by at least 20% a year, which is my baseline expectation… and that’s also about where the stock is trading at the moment, after the 20% post-earnings pop in the share price (revenue growth has been well above that 20% growth level for all but two or three quarters since they went public in mid-2016,… earnings growth has been more volatile but has averaged much more than 20%, both revenue and earnings per share have grown at a compound average rate of 37% since that IPO, almost eight years ago).

My “preferred buy” level settles in at $360 now, which is also roughly where the shares were trading six weeks ago, and pretty close to my last buy in the $340s. I imagine things will continue to be volatile, and the inherent risk of their business, which shouldn’t be able to grow this fast forever and could, at this kind of valuation, bring a 50% overnight drop in the share price if they’ve made a critical underwriting error somewhere and report a terrible quarter someday, means I’ll continue to cap my exposure here to about a half-position (roughly 2% of my equity capital), but Kinsale has steadily been earning this kind of valuation so I’m at least happy to let it ride, and will likely continue to nibble if prices stay in my range as I add more capital to the portfolio. The risk of a terrible outcome fades as they continue to execute so well, and as the Excess & Surplus Lines market continues to be perfectly set up for them to take share, but I don’t want to become too complacent in assuming that will forever be the case in the future. I’ve drunk the Kinsale Kool-Ade, and I’m loving it… but I can at least tell the bartender to hold off after half a cup.

*****

Toast (TOST) is one of the simpler tech stocks I own — with its huge market share in restaurant POS systems, it essentially acts like a royalty (between 0.5-1%) on restaurant sales. They’ve invested heavily in a sales force to push their payment systems out to more and more restaurants, concentrating on building max concentration in geographic areas, which then should build up to a network effect of sorts, letting them continue to grow with less “sales” investment, and they’ve been trying to build on the success of the payments platform by selling more add-on software modules to Toast restaurants. There is competition in this space, so the challenge is that they have spent a lot on building that sales force, and have to keep spending on R&D to keep the platform appealing to their customers, even as there’s always some churn because a lot of restaurants fail… but the relentless growth of that “royalty” over time makes the potential for exceptional returns enticing, once they begin to really scale up to consistent profitability and, most likely, huge profit growth in the coming 5-10 years if the overall consumer economy avoids a big recession.

Information leaked out yesterday, before the earnings release, that Toast had laid off about 10% of its workforce, joining the parade of tech companies who have a newfound interest in efficiency and profitability, but that didn’t tell us much about who was being laid off, or what that might mean for the company… for that, we had to wait until they actually reported earnings last night. Was it because they had reached self-sustaining scale in sales, and they didn’t need as large a sales force? Was it because sales were weaker than expected, and they had to cut costs? Just a realization that they had over-hired, like many tech companies in recent years? Toast is the company that’s physically closest to Gumshoe HQ, they’re in Boston and I’m only about 100 miles away, and I imagine most of us probably know a restaurateur that uses the platform, but I’m afraid that didn’t led me to any great insight on what these layoffs might mean. Which is OK, we don’t have to trade on every bit of news… I resolved to wait a full 12 hours before I had more information. I know it’s stupid, but these days, sadly, that sometimes feels like some Warren Buffett/Charlie Munger stoicism and patience. Waiting for real information? How old fashioned!

Well, turned out that this was a “restructuring” the board agreed to, which mostly sounds sensible. And the results were quite solid, Toast added another 6,500 locations in the fourth quarter, so they’re up to 106,000 now, and their annualized recurring revenue run rate grew 35% over the past year to now $1.2 billion (that’s from both their payment processing “royalty” on a stream of gross payment volume that is now over $33 billion a year, and the more profitable, but smaller revenue, software subscriptions). They had mildly positive EBITDA and positive cash flow, as has been the case for a couple quarters, but are still losing money on a GAAP basis… and they still have plenty of cash, that enduring legacy of the fact that they lucked out by going public when valuations were stupid, in late 2021.

They expect adjusted EBITDA to remain positive and grow, reaching $200 million this year (the comparable number was $61 million last year, which was their first year without a negative number in that column). And they made some large deals, expanding into larger enterprises — they’re going into Caribou Coffee with their Enterprise Solutions, and into Choice Hotels (for restaurants at Cambria and Radisson hotels, at least, and maybe more), so they are encroaching on the big customers that are slower to change, which is good news (though it’s arguably mildly negative news for PAR Technology, our other small restaurant POS provider, since big chains are their core business… I think there’s plenty of room for both, particularly given PAR’s huge advantage with the larger fast food chains, but at some point the competition will probably tighten with those two and the other new and legacy providers).

That’s roughly the kind of adjusted EBITDA that ROKU analysts are expecting, interestingly enough, though ROKU is projected to be 2-3 quarters behind in reaching that levle, and the two are expected to have pretty similar growth as well, and are similar in size (market cap $10-12 billion), but I am a lot more confident in projecting the future profitability ramp for Toast, given the stickiness of their customers and the steadiness of their payments and subscription revenue — partly because it’s growing the user base faster and the revenue line and gross profit much faster. Roku’s only real advantage in that comparison is that their end market is much larger… but Toast is still far from saturating their market, and they’ve barely begun to move overseas. Not that the two are directly comparable, but sometimes it’s worth comparing two unprofitable growth companies to see if one obviously stands out as more hopeful or more predictable, and in this case Toast looks a lot more compelling because of that more predictable future.

Toast is not quite as easy a buy now as it was last Fall, when investors were worried about their last quarter and I added to my holdings, but it’s still in a pretty reasonable valuation range given the reasonably predictable revenue growth, as long as you’re willing to wait for that growth to become real earnings as they reduce costs and continue to scale up their user base over the next few years. I haven’t changed my valuation thinking, for me TOST is still worth considering up to a max buy of $26 and is more appealing below my “preferred buy” level of $18, and we’re right in the middle of those two numbers after a good post-earnings “pop” today. It’s a bumpy ride, and they aren’t obviously or abundantly profitable yet, which means they tend to get sold down whenever investors are feeling fearful, so being patient can work… but this is one of the few rapid growth companies where I own and the stock reported great results and an optimistic outlook, including the cost-cutting from those layoffs and a new buyback authorization, and the stock popped much higher (a 15% jump this time), and yet the stock remains below my “max buy” number. So that’s something.

*****

Some more minor updates…

BioArctic (BIOA-B.ST, BRCTF) reported its final 2023 results, with no real surprise — for those who don’t recall, BioArctic was the original developer of what Eisai and Biogen turned into Leqembi, the only approved disease-modifying treatment for Alzheimer’s Disease, and the reason we own it is because although BioArctic continues to develop other early-stage treatments for brain diseases, with their most advanced new molecule being in Parkinson’s Disease, the company itself is essentially a small R&D shop which, if Leqembi becomes a big and long-term hit as an Alzheimer’s treatment, enjoy massive royalties on those sales. It’s slow-developing, mostly because this first formulation of Leqembi is hard to prescribe and hard to provide, so Biogen and Eisai have had to do a lot of patient and provider education and build out an infrastructure to serve them, but dosing is ongoing in the US and Japan, and will begin in China later this year, so there remains potential for this to be a blockbuster drug… particularly if the subcutaneous version gets approved in the relatively near future, making dosing much easier (currently, it has to be infused). My intent was to wait at least a year or so to see how the ramp-up of Leqembi sales proceeds, and I may have to wait longer than that, given the slow start, but from what I can tell everything is still proceeding just fine. Here’s their press release with the latest results, if you want the specifics, but it doesn’t mean much — we’re still just waiting for the huge potential patient base to get access to Leqembi, and, given the valuation of BioArctic, I don’t think we’re risking a ton as we wait… but any fantastic returns might well be several years down the road, and are far from certain.

Royal Gold (RGLD) released its full earnings update, and was right in line with the preliminary results they shared in January, so my estimate of cash flow was pretty close (I figured they’d have operating cash flow of $414 million, the reported $416 million), and they offered top-line guidance for GEOs (gold equivalent ounces) to be about the same in the first quarter as it was last quarter (47-52,000 GEOs — last quarter it was 49,000). In the end, net income for 2023 was about the same as 2022, but they did raise the dividend a bit and improve the balance sheet. They didn’t give any guidance going further out, but they probably will do so next quarter — and given their revenue sources (76% gold, 12% silver, 9% copper last year), the stock will presumably rise or fall with gold prices. They don’t have quite the same single-property risk that we’ve seen from Sandstorm Gold (Hod Maden) and Franco-Nevada (Cobre Panama) over the past year, at least in the eyes of investors, so the shares are holding up reasonably well over the past year (not doing as well as Wheaton Precious Metals, better than FNV or SAND)… so RGLD still has a better valuation than any other large gold royalty company other than Sandstorm (which remains much cheaper, since people hate it right now following their at-least-temporarily-dilutive acquisitions), and it has a better likely revenue/earnings/cash flow growth profile than FNV or SAND, with growth likely to be about as good as WPM (which is far more expensive).

No change to my assessment at this point, RGLD would be the easiest buy among the big royalty companies, with historical stability and a reasonably discounted valuation and some likely production growth… but Franco-Nevada is close to being “buyable”, given the disastrous crunch they took from the Cobre Panama closure last year (they don’t report until early March, so I’m hoping they’ll disappoint and take a beating again, FNV has always been worth buying when it trades like the ‘average’ royalty companies, and those moments have been fairly rare). Sandstorm is so hated that it’s hard to know when things might turn, we’re really waiting for Nolan Watson to prove he meant it when he said that Sandstorm’s growth is “in construction” now, and they’re essentially done with their big acquisitions… if so, and if their collection of mines comes online roughly as expected, they should outperform all the others, but that remains a big “if.”

And Sandstorm Gold (SAND), which likewise had preannounced some of its 2023 numbers, reported last night — here’s what I said last month, when we got their top-line numbers:

Growth is not going to be great in the next year or so unless the gold price goes meaningfully higher, since their larger growth properties (new mines) won’t be coming online instantly, but there are some new mines and some expansion projects in the works, and production should grow slightly. Assuming that Sandstorm CEO Nolan Watson has learned some lessons from his aggressive acquisitions, and is genuinely willing to sit on his hands and stop issuing shares, Sandstorm will be able to spend the next couple years paying down debt and letting the actual cash flow finally begin to compound, so there’s still a good path to a very strong return over the long term, if gold prices don’t collapse — but it’s understandable that investors are sick of waiting, given Sandstorm’s serious underperformance relative to its larger gold royalty peers, and the fact that they took some dilutive steps backward on the “capital efficiency” stairway in 2022 in order to boost their asset base and improve their future growth profile.

The final numbers were a hair lower than their preliminary ones, since actual accounting revenue of $180 million fell short of the $191 million “total sales” number they had preannounced, but the key metrics don’t change that much (operating cash flow was $151 million, and I had expected $155-160 given their top-line guidance). They continued to talk about delevering this year, selling non-core assets to pay down debt, and being disciplined about waiting for the growth to emerge from the portfolio they already own, which is positive in my book. My “max buy” is 20X operating cash flow for SAND, too, though I also net out their debt (since it’s considerable), and that would still be $9 — very, very far away, in part, I think, because investors don’t really trust Watson to really stop making those big acquisitions that won’t bear fruit for many years. “Preferred buy” remains about half of that, so would mean buying the company at close to a 10% cash flow yield (operating cash flow is not the same as free cash flow or earnings, but I did net out the debt balance, and you get the general idea).

I’ve been too stubborn with SAND, and either RGLD or FNV is probably a safer investment because of the length of time it has taken for Sandstorm’s growth assets to be built, but those assets are still very likely to be developed (or completed, for the ones in development), and I think SAND management has absorbed the hard lesson of their too-ambitious acquisitions and will let the portfolio develop organically. Which should mean that Sandstorm has much more growth potential than the other gold royalty companies if we see another gold bull market, because they should enjoy both revenue growth from new mines coming online and multiple expansion as they catch back up with the more beloved players in this space…. but that’s been true for a few years, and I wouldn’t blame you for being skeptical.

*****

Teqnion (TEQ.ST) reports tomorrow morning, following the Berkshire Hathaway model (issue financial reports on the weekend, so people can think them over when the stock isn’t moving around), so we’ll see how that goes — enthusiasm has risen for this stock again, as more investors have discovered it, which means the stock has hit new all-time highs this week in the absence of any other news about their subsidiaries (or any new acquisitions recently), so it’s at a tough-to-justify valuation of about 35X earnings at the moment… but that’s OK. I’ve pretty well bought into the plan from Daniel and Johan, and I intend to be patient with this one.

Berkshire should report a week from tomorrow, incidentally, and has bumped up above my “max buy” price for the first time in a very long time, so it’s going into this next earnings report as an awfully popular stock… we’ll see what happens, but the underwriting and investment earnings will probably be pretty exceptional. And maybe they’ll finally tell us what stock they’ve been secretly buying, with waivers from SEC disclosure, over the past two quarters (Berkshire has been building at least one position, probably in the financial sector, that they’ve asked the SEC to let them not divulge in their last two 13F filings — which isn’t that unusual, Berkshire has done the same a couple times in the past, though two quarters in a row is a little surprising and means they must still be buying whatever it is, so it could be a large position of something big, though they would have to disclose if it reaches 5% ownership in any one company).

*****

I got a reader question about NVIDIA (NVDA) and SoundHound AI (SOUN) this week, and thought others might be interested in the answer… since for probably stupid regulatory reasons, and due to a lack of financial education among financial writers, it became NEWS this week that NVIDIA owns a little bit of SoundHound. That send the stock of SOUN up almost 70%.

What actually happened? Here’s an expanded version of what I wrote in a comment to that reader:

NVIDIA has owned a little slice of SoundHound since it was a venture investment a long time ago — maybe 2017? I would have to check to be sure, but the date doesn’t really matter. There was a flurry of interest this week because of NVIDIA’s disclosures about a handful of small venture investments it owns… but I believe none of those are new, it’s just that NVIDIA didn’t previously have enough value in outside investments that it was required to file a 13F.

What changed? ARM Holdings (ARM) went public, and that’s NVIDIA’s biggest investment by far (presumably a remnant of when they tried and failed to acquire Arm Holdings from Softbank a couple years ago, though it’s possible they bought more). I’m guessing that since the IPO was in the last days of the third quarter, NVIDIA probably was supposed to file a 13-F in mid-November to acknowledge that holding as of the third quarter, because their total investment portfolio was probably worth more than $100 million at that time, for the first time (I think “managing $100 million” is the cutoff for being required to file a quarterly 13-F of your US equity holdings, but the number could have changed since I last checked), but there may be technical reasons why they didn’t have to do so at that point, maybe they get a little grace period after an IPO or something. Now they do have to file the 13F, though, because of their positions in ARM and RXRX, which now add up to a bit over $300 million. Unless the values of those positions drop below $100 million, or they sell those (relatively) larger stakes in ARM or RXRX, NVIDIA will now be filing 13Fs each quarter.

I would not buy anything just because NVIDIA was forced to file the details of their ownership stakes in five companies that they’ve invested in on a venture level or have ownership stakes with due to a partnership (like Recursion (RXRX), which is their second-largest investment after ARM, and the only other one of meaningful size). NVIDIA’s holdings in ARM are currently worth a little over $200 million, and in RXRX just under $100 million, so those are barely rounding errors for a massive firm like NVIDIA… but NVIDIA’s stakes in Soundhound, TuSimple (which is delisting and on its way to becoming even more irrelevant, most likely), and Nano X Imaging (NNOX), the only other three publicly traded companies they hold some shares in, are all lint on the shoulder of the rounding error. All those stakes are well under $5 million.

More importantly, I’d say that none of those represent a new commitment of capital by NVIDIA this quarter, or a strategic endorsement of those firms by the leading AI chipmaker. If I were trading Soundhound, I’d consider this a gift horse worth selling after that surge, though if you have reasons you want to own it for the long term (I don’t), this surge might be irrelevant in a decade.

So NO, NVIDIA did NOT just buy SOUN or TuSimple (TSPH), no matter what you read. They just disclosed those tiny holdings for the first time. Even the larger holdings in ARMH and RXRX are irrelevant to NVIDIA and to ARMH, though I guess since the RXRX investment by NVIDIA was just last year, and it’s a far smaller company, I guess you could argue that RXRX is impacted by NVIDIA’s strategic investment in the company (though that’s also not new, the investment was made back in July and sent RXRX shares soaring to close to $40… they’re around $13 now, despite a pop on this 13F release, so NVIDIA is so far losing money on that — though, again, it’s a trivial amount of money for NVIDIA, essentially just a way to seed another customer with a little cash to help move AI drug discover research along, and create more of a market for NVIDIA’s chips in the future).

I’m not going to get involved with any of these stocks, to be clear, but I’d be tempted to bet against TuSimple, SoundHound or Nano X after this silly NVIDIA-caused pop in their shares this week, not to buy them. Usually when unprofitable and story-driven stocks jump for no reason, they come back down pretty quickly when sanity prevails… though we all saw GameStop (GME) a few years ago, and other nutty stories like the Truth Social SPAC, Digital World Acquisition (DWAC) this week, so one can never be all certain about when or if sanity will prevail.

That level of inanity in TSPH, SOUN and NNOX this week is yet another sign of the coming apocalypse for the “AI Mania” stocks, I’m afraid, and the kind of thing that conjures up visions of this being another “dot com bubble.” It might or might not be, of course, we can’t predict the future, and in many ways the valuations of the biggest AI-related stocks (NVIDIA, MSFT, GOOG, etc.) are FAR more reasonable than the valuations of the biggest dot-com stocks before the crash in 2000, but the rhymes are sounding more and more familiar.

The most reasonable counter-argument to that is not that this isn’t a silly and extreme valuation bubble for the AI-related story stocks… no, the best counter-argument, I think, is that it’s not extreme enough yet, and this is more like 1998 than 2000, so we might just be getting started on our way to a truly crazy bubble. There may be more mania to come.

A reminder of the apocryphal bumper stickers in Silicon Valley circa 2004 or so, “Please God, Just One More Bubble.”

NVIDIA earnings forecasts keep going up, and analyst price targets keep rising, so there’s still no expectation in the market that their revenue growth will slow down markedly, or, more importantly, that this slowdown will be associated with a meaningful drop in profit margins as slowing demand (eventually) cuts into their pricing power. I said back in December, following the last earnings update, that I could rationally justify a range of valuations from $300 to about $680, but was more likely to take profits near $500 (where it was then) than to buy more anywhere near that level. For at least a little while this week, NVIDIA, with ~$20 billion in operating income over the last four quarters, became larger than either Alphabet (~$85 billion in operating income) or Amazon ($37b). Investors love growth, and over the past five years NVIDIA’s revenue growth (total 318%) has certainly been much higher than almost any other very large company (AMZN was 138%, GOOG 117%, only Tesla (TSLA) really competes on that front with 328% revenue growth — though as a manufacturer, their margins are dramatically less impressive) .

Since my last comment, the analyst forecasts for the next two years have gone up a bit, without any real news from NVIDIA but with general rising optimism about A.I. spending from the tech titans over the past few weeks… so we’re heading into earnings now with analysts expecting $18.32 in GAAP earnings over this fiscal year that is just starting now (FY25), up from $17.79, and $21.50 next fiscal year (FY26), up from $20.76. (The adjusted earnings numbers are higher, though as I noted the growth has closed the gap, they’re at $20.71 and $25.17, but I can’t seriously consider using even more optimistic numbers for a company that is already flying on optimism, not when they’ve got a $1.8 trillion valuation. and trade at 40X trailing revenues.)

I’m still holding on to a meaningful stake in NVIDIA, having owned the stock but traded it poorly for many years, so let that be a lesson to you if you’re following my portfolio in any detail — sometimes I trade quite badly, and that has been more true with NVDA than with most of the stocks I’ve owned over the past decade. With that caveat, I’m willing to hold on to see how this plays out… but after the mania represented by those SoundHound trades as we head into NVDA earnings next week (they report after the close on Wednesday), and as the stock crests 40X sales, I can’t resist shaving off a little more of my profit.

So I sold 10% of my NVIDIA shares as it toyed with $740 today, going into next week’s earnings update. It’s entirely possible, and even rational, to project that the demand for their GPUs will keep soaring for a couple years, the party will keep going, and that NVDA will see $1,200 a year from now… but it’s also entirely possible that demand softens just a little, and margins get back to something more like normal, leading to much lower earnings than expected, and NVDA falls to $300 over the next year (or further, if there’s a genuine crash in the tech stocks — though I don’t think that’s particularly likely). The one thing analysts have been consistent about is that they’re always very wrong in estimating NVIDIA’s earnings, even more so than with most companies — and that’s true when things suddenly get surprisingly worse, just as it is when things get surprisingly better.

So that’s what I did this week… taking some partial profits on both a pretty cheap stock (WCC) and a wildly expensive one (NVDA), for different reasons. I didn’t put any of that cash to work just yet, but I’ll let you know when I do so.

And that’s more than any one person should have to read, and I want to get this out to you before the market close, since some folks have asked what I’m doing with those WESCO shares, in particular, so there you have it… questions? Comments? Just use our happy little comment box below… and thanks, as always, for reading and supporting Stock Gumshoe.

P.S. I’ll be on a reduced schedule next week as I take some time to loll in the sun with the family during the kids’ vacation break, so there might not be many new articles for a few days, but I’m sure I’ll come up with something to share by the time your next Friday File is due.

Disclosure: Of the companies mentioned above, I own shares of NVIDIA, Berkshire Hathaway, PAR Technology, WESCO, Kinsale Capital, The Trade Desk, Atkore, Roku, Toast, Alphabet, Teqnion, Royal Gold, Sandstorm Gold, BioArctic, and Amazon. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.

{kind=link}

{kind=link}