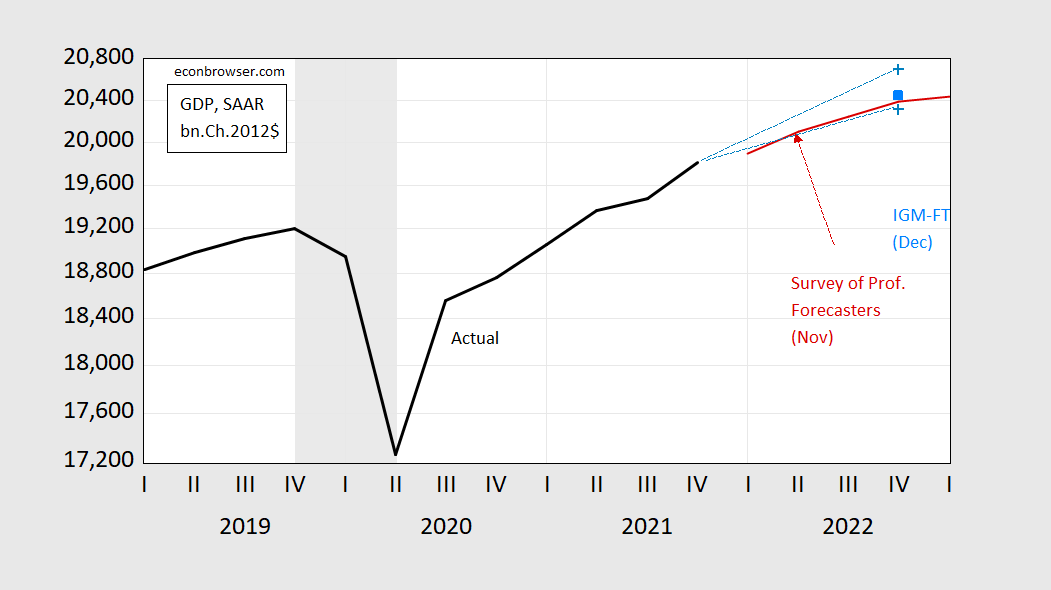

Survey conducted last week, published today here. This FT-IGM Macroeconomist Survey The median forecast implies this path for GDP:

figure 1: GDP (black), FT-IGM survey median (light blue large square), 10th/90th percentile (light blue+) and February Professional Forecaster Survey mean (red), all in ten The unit is Ch.2012$ SAAR. Recession dates as defined by NBER are shaded from peak to trough in gray. Source: BEA, Q4 2nd Edition, FT-IGM survey, Philadelphia Fed, NBER and author’s calculations.

The FT-IGM investigation was conducted on the eve of Russia’s invasion of Ukraine (21-23 February). It will be interesting to see how this information is factored into the assessment (a number of other data emerged between the surveys in early December and late February, including an early release of GDP for the fourth quarter).

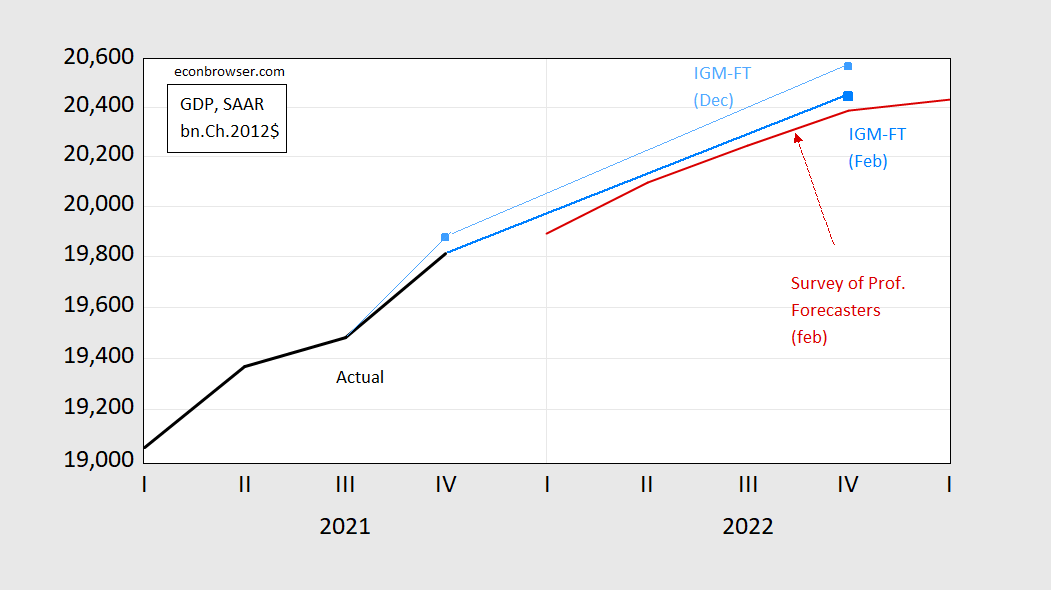

figure 2: GDP (black), FT-IGM survey median responses for February (large light blue squares) and December 2021 (small light blue squares), and February professional forecaster survey mean (red), all in ten Billions in Ch.2012$ SAAR. Source: BEA, 4th Quarter 2nd Edition, FT-IGM Survey, Philadelphia Fed, NBER and author’s calculations.

Given that by Tuesday I was almost 100% certain that an invasion was imminent, my reasons for lowering the estimated growth were obvious. Higher oil prices then trigger a direct contractionary effect through supply shocks and tighter monetary policy. (WTI is now around $100/barrel).

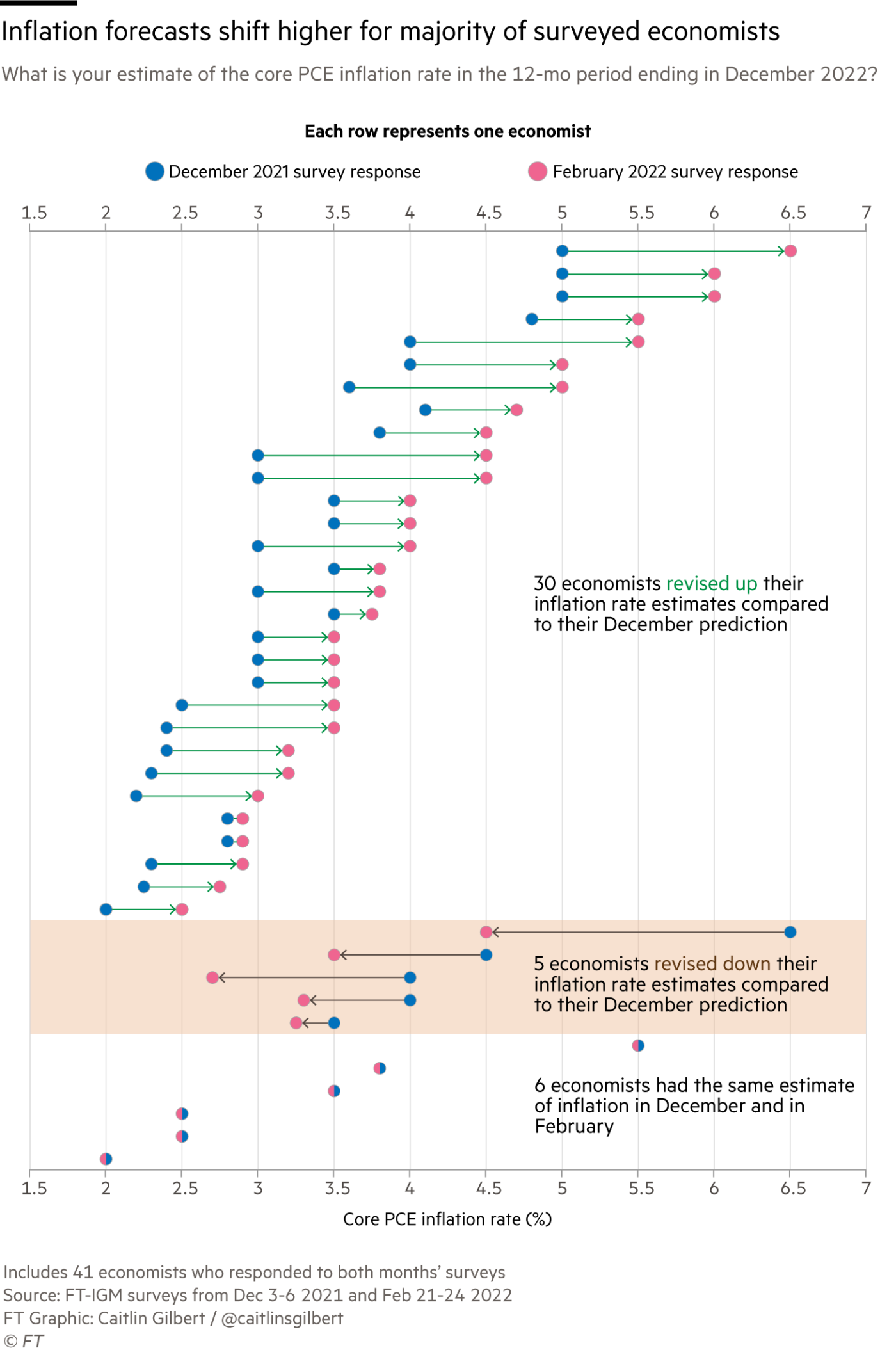

Economists in the survey raised their inflation estimates, as Financial Times article Describe the findings; my estimate rose as inflation continued to beat my expectations; but it also rose as oil prices rose.

resource: Financial Times, 28 February 2022.

{kind=link}

{kind=link}