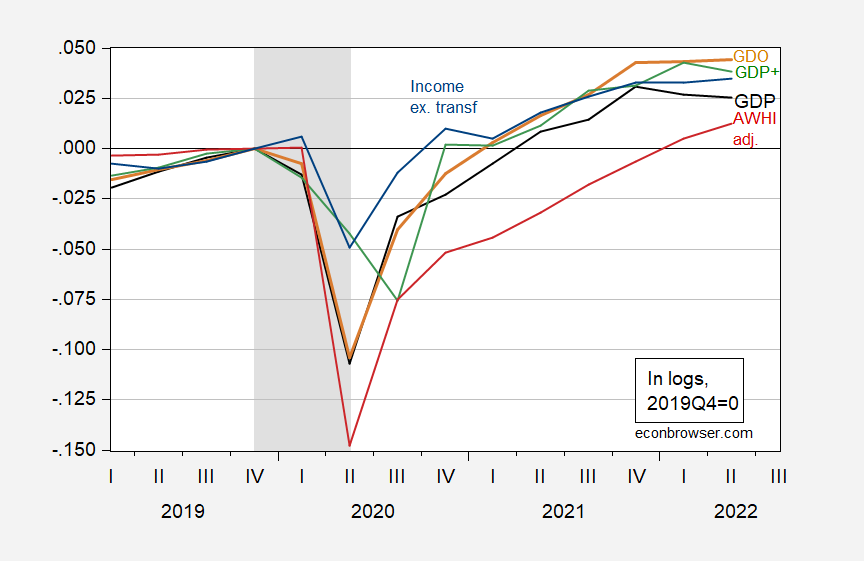

Follow up on Friday’s post (“When is a recession not a recession?”) go through Jan Pam Jacobs, Samad Saferaz, Jan-Egbert Sturm and Simon of Norden here are some pictures of alternative GDP indicator levels, and the quarterly frequency of two key variables followed by the NBER Business Cycle Dating Committee (total hours worked, personal income excluding transfers).

figure 1: GDP (black), GDO (tan), GDP+ (green), total weekly hours worked index (red), and personal income excluding transfers (blue), all in the logarithm of Q4 2019 = 0 . The NBER recession peak-to-trough recession dates are shaded in gray.Note that the weekly total hours index has been adjusted for inclusion in the preliminary benchmark series, as described in this article postal. GDP+ converted to levels using the first quarter of 2016 as a base and subsequent growth rates. Source: Bank of East Asia Second Quarter 2nd Edition, Philadelphia FedBLS, NBER, and the authors’ calculations.

Note that I didn’t include GDP++.However, as pointed out Jacobs et al.GDP++ and GDO are very close to Q1-Q2 growth, so you can infer that the contours of GDP++ are roughly the same as GDO shown above – ie weak but not negative growth.

The GDPNow Q3 now forecast is 1.6%, the St. Louis Fed is 0.9%, and Goldman Sachs is 1.0% (both 8/26). Deutsche Bank forecast 2.8% (as of Aug. 26).

{kind=link}

{kind=link}