this Bureau of Economic Analysis It was announced today that the seasonally adjusted real GDP growth rate for the third quarter of the United States was 2%, slightly lower than the 2.25% average growth rate we saw during the last economic expansion.

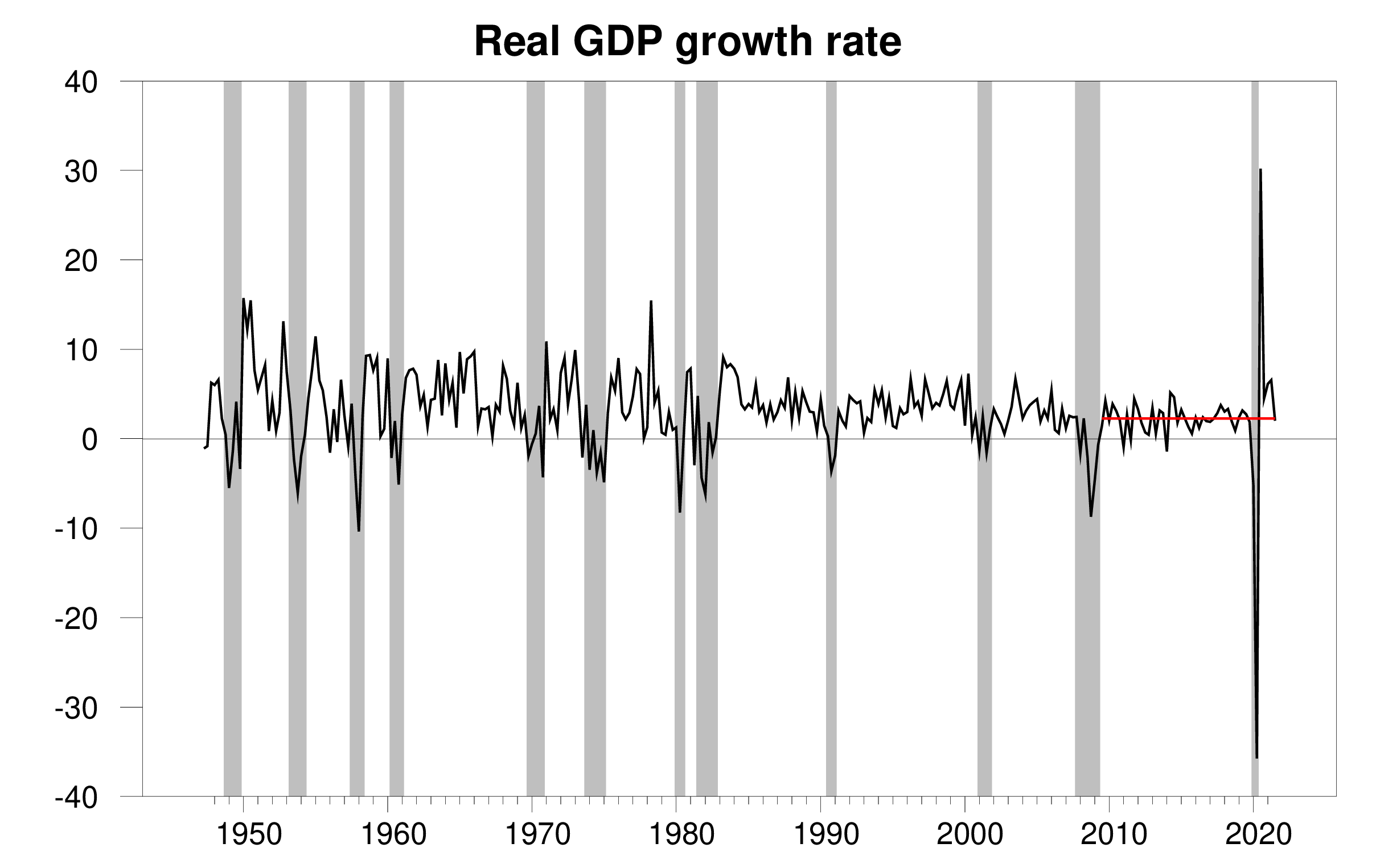

The annual real GDP growth rate, 1947:Q2-2021:Q3, 2009:3-2019:4 average (2.25%) is red. Calculated as 400 times the difference between the natural logarithm of GDP and the previous quarter.

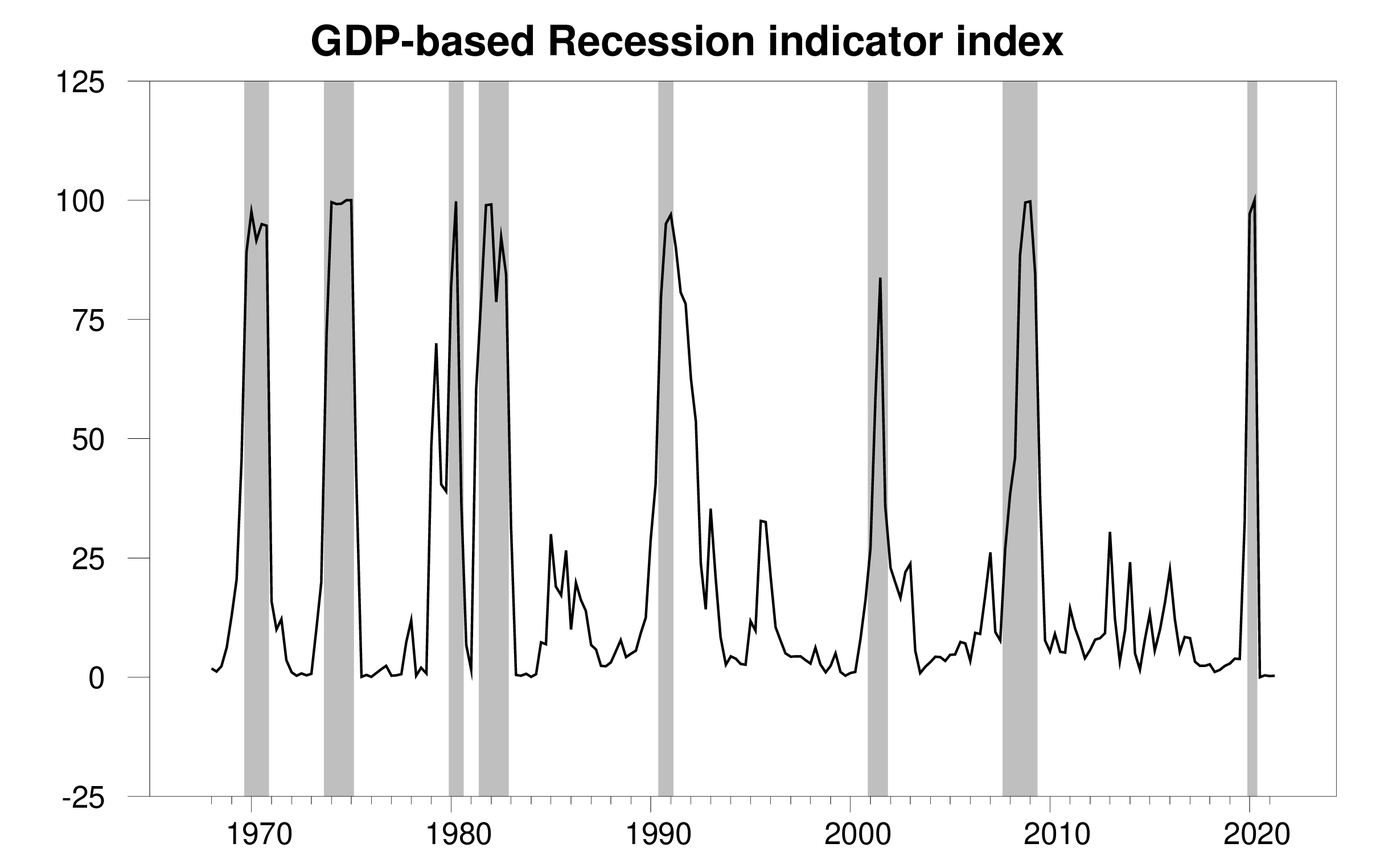

The new data shows Economic Browser Recession Index 0.3% is a very low value historically, marking the clear continuation of economic expansion. The figure released today (0.3%) is an assessment of the economic situation in the previous quarter (ie, the second quarter of 2021). We use a quarter lag to allow data revision and obtain better accuracy. This index provides the basis for our 15-year automated procedure to allocate the dates of the first and last quarters of the recession.As we announced January 28, The COVID recession ends in the second quarter of 2020. The NBER Business Cycle Dating Committee subsequently July 19.

Index of recession indicators based on GDP. The plotted value for each date is based only on the published GDP figures up to one quarter after the specified date. The last date shown in the figure is the second quarter of 2021. The shaded areas represent the NBER decline dates, which were not used in any way to construct the index.

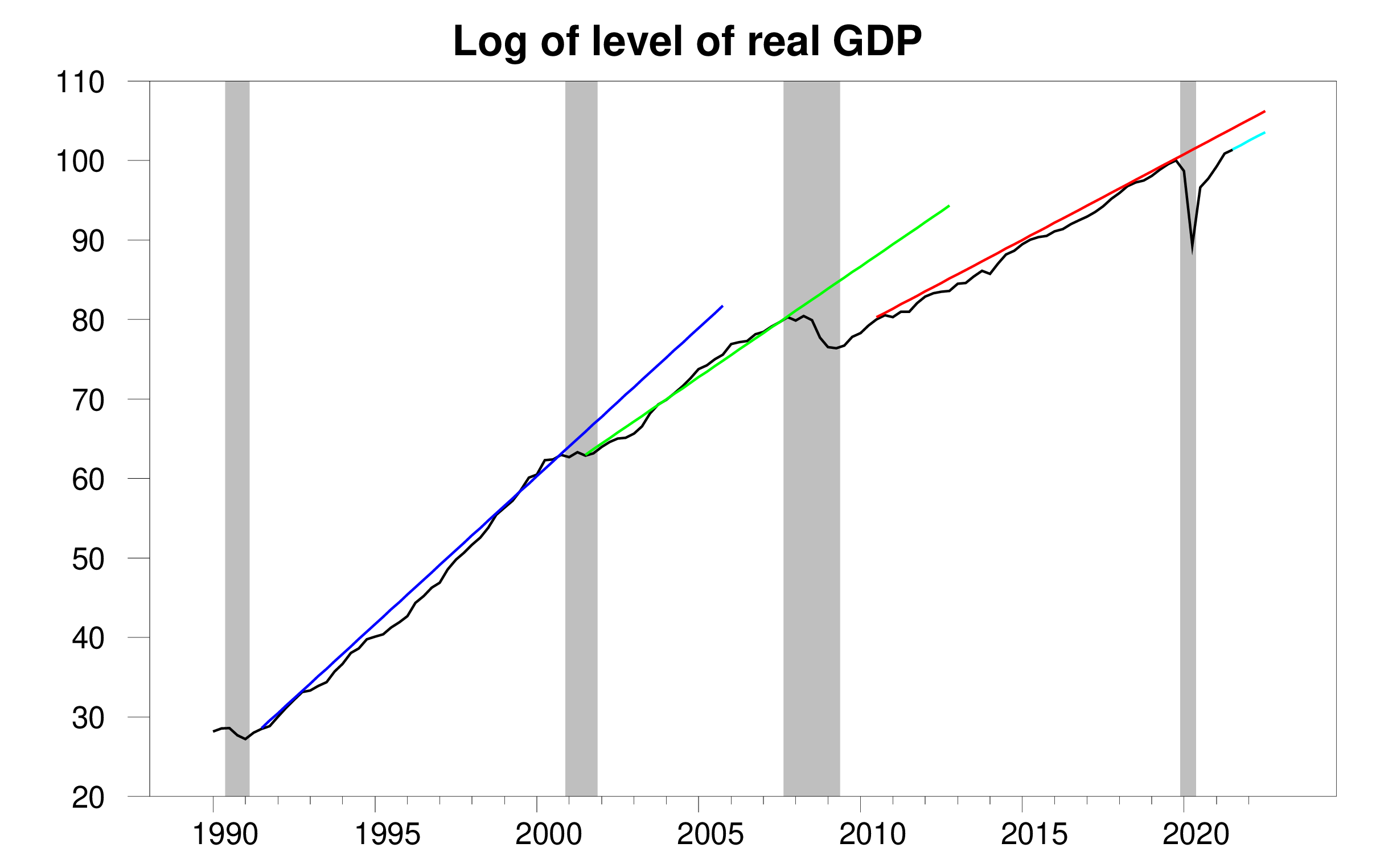

By the second quarter, the GDP level had returned to 2019: the fourth quarter before the start of the COVID recession. However, if we want to return to the trend line related to the previous expansion (shown in red in the graph below), we need to see a growth of more than 4% in the third quarter instead of 2%, and we must maintain the pace for the entire year.

100 times the natural logarithm of the real GDP level from the first quarter of 1990 to the third quarter of 2021, normalized to the fourth quarter of 2019 = 100. A movement of 1 unit on the vertical axis corresponds to a 1% change in the level of real GDP. The blue line infers the expansion trend in 1991-2000, the green infers the expansion trend in 2001-2007, and the red infers the expansion trend in 2010-2019.

However, once the recession is over, we will return to the previous trend of expectations and there is not much data to support. The economic recession seems to have a permanent impact on GDP levels. In the first few quarters of expansion (the “V”-shaped recovery phase), there will usually be above-average growth. But once GDP levels return to pre-recession levels, trend growth becomes the norm. We also see in the graph above that the average growth rate during the expansion period (the slope of the decision line) seems to decrease over time. An important factor leading to the decline in the average growth rate is the slowdown in labor and productivity growth.

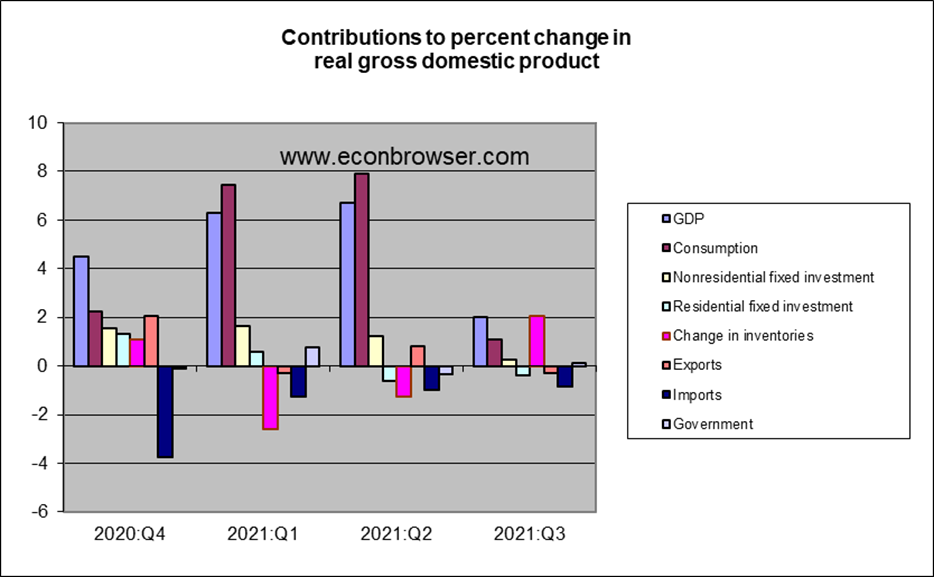

As far as the various components of GDP are concerned, a key reason why the economy grew by only 2% in the third quarter was the slowdown in consumer spending growth. Buying a car is one of the important factors.An important reason is Difficulties facing automakers Obtain the computer chips needed to assemble modern cars.

Another disappointment was the construction of new houses, which had a negative impact on the growth rate in the third quarter. We have seen a lot of residential fixed investment that stimulated low interest rates and sharp rises in housing prices. Some analysts The slow construction of new homes is also blamed on supply issues.

Inventory changes are a bigger factor in GDP data. If inventory investment does not make a positive contribution, GDP in the third quarter will actually fall relative to the second quarter. To understand what this means, it is important to remember how the inventory is entered into the GDP account. The inventory change in a quarter is called inventory investment. If the inventory is eventually higher than the beginning, the inventory investment is positive, if the inventory is lower than the beginning, the inventory investment is negative. The inventory investment in the second quarter of this year was significantly negative (ie, quarterly-$174B). Inventory investment in the third quarter was still negative (ie -$68B), but not as negative as in the second quarter. Therefore, the inventory investment in the third quarter was $106B (-68 – (-174) = +106) higher than in the second quarter. This alone basically accounts for all the GDP growth between the second and third quarters.

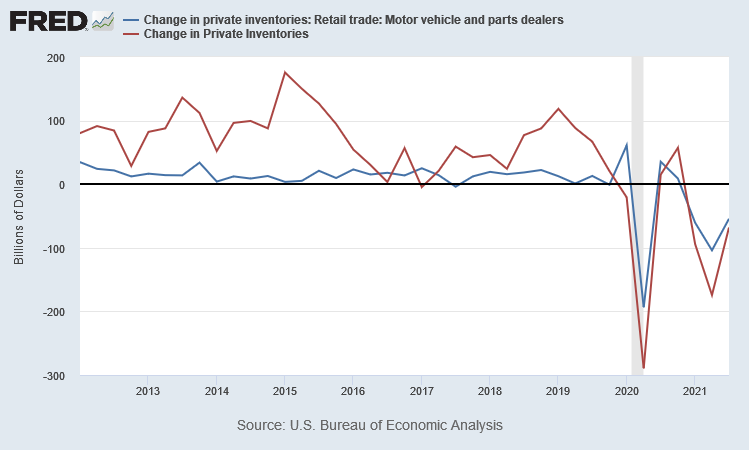

Nominal inventory investment, quoted quarterly, 2012:Q1-2021:Q3.Red line: changes in the value of the dollar All private inventory. Blue line: change in dollar value of dealer inventory Motor vehicles and parts.

The above chart also shows the source of these inventory changes: the car is the main story. Manufacturers did not deliver enough new cars to dealers, which is why the inventory at the end of the quarter was lower than at the beginning. This is another important way for automakers’ supply chain issues to have a significant impact on US GDP.

As these supply constraints ease, I expect consumer purchases and dealer replenishments to surge. Both of these changes should greatly boost GDP. Therefore, once the supply problem is relieved, the growth we should expect may be 4% instead of 2%.

But fiscal and monetary stimulus are not the policies we should seek to enable us to achieve faster economic growth.

{kind=link}

{kind=link}