Annual benchmark revision (release) made a major change to reported GDP levels – but not to growth rates in the first half of 2022 – while GDO was revised down slightly as GDI was revised downward. Final sales to domestic private buyers, a measure of domestic demand, were revised up and higher.

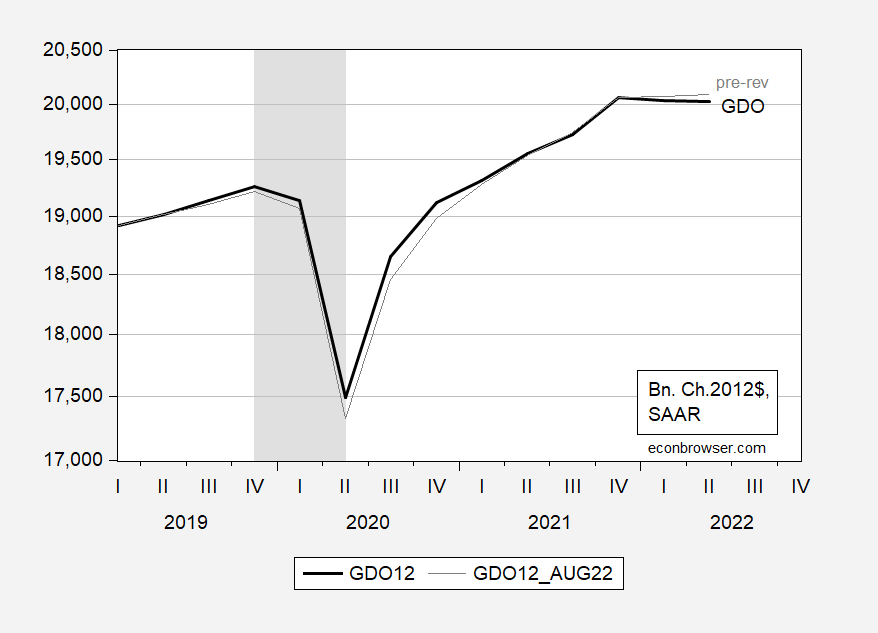

The first GDO, in dollars:

figure 1: Gross domestic product (bold black), pre-year benchmark revisions (grey), all in billions Ch.2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BEA via ALFRED, NBER and author’s calculations.

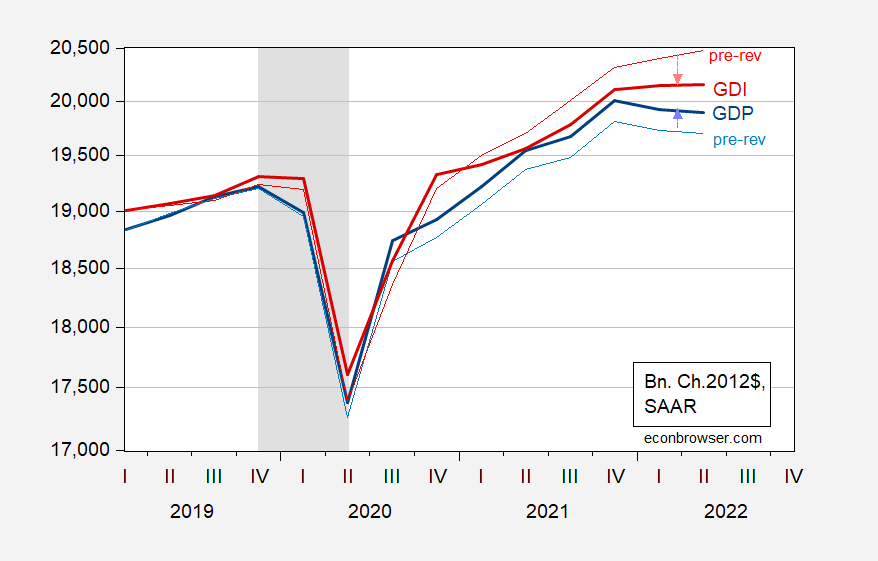

GDO declined at an annualized rate of 0.4% and 0.3% in the first and second quarters, respectively. The relative lack of change in levels is due to offsetting changes in GDP and GDI levels:

figure 2: GDP (blue bold), year-ago benchmark revision (light blue), GDI (red bold), year-ago benchmark revision (light red), all in billions Ch.2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BEA via ALFRED, NBER and author’s calculations.

GDP levels rose, while GDI, on the other hand, flattened out from the fourth quarter of 2021. This means that the gap between reported GDI and GDP has narrowed to a more normal level. Both GDP and GDI revisions accounted for about half of the revisions, as shown in the chart below:

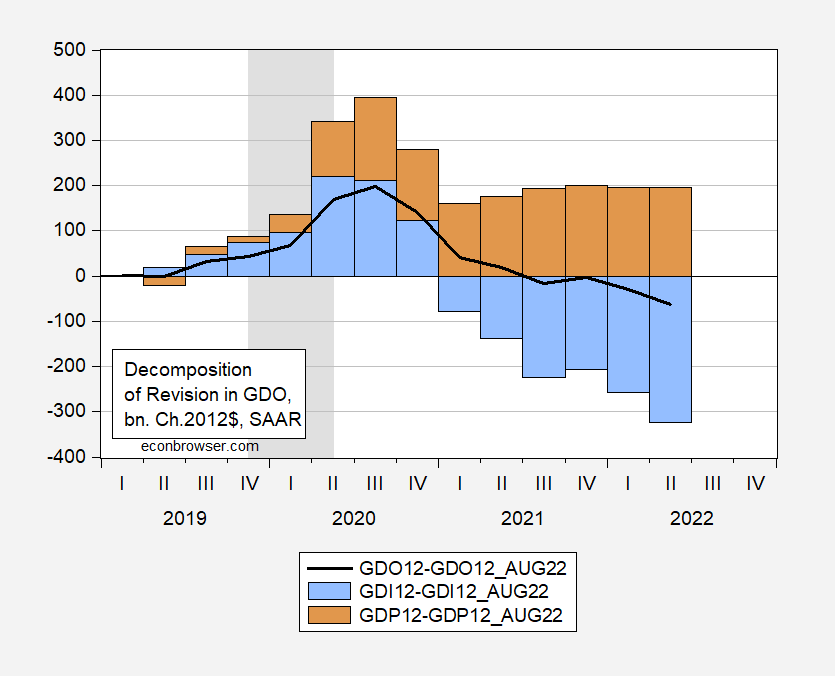

image 3: Revised GDP (bold black), GDP contribution (tan bars), GDI (light blue), all in billions Ch.2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BEA via ALFRED, NBER and author’s calculations.

from release:

real GDI Growth in the first quarter is now estimated at 0.8% (Table 1); in previously published estimates, GDI was estimated at 1.8% in the first quarter. The main reason for the downward revision is compensation, based primarily on new first-quarter wage and salary estimates from the U.S. Bureau of Labor Statistics’ Quarterly Census of Employment and Wages.This Average of real GDP and real GDI The first quarter is now estimated to have declined by 0.4%; in previously published estimates, the average GDP and GDI were estimated to have increased by 0.1%.

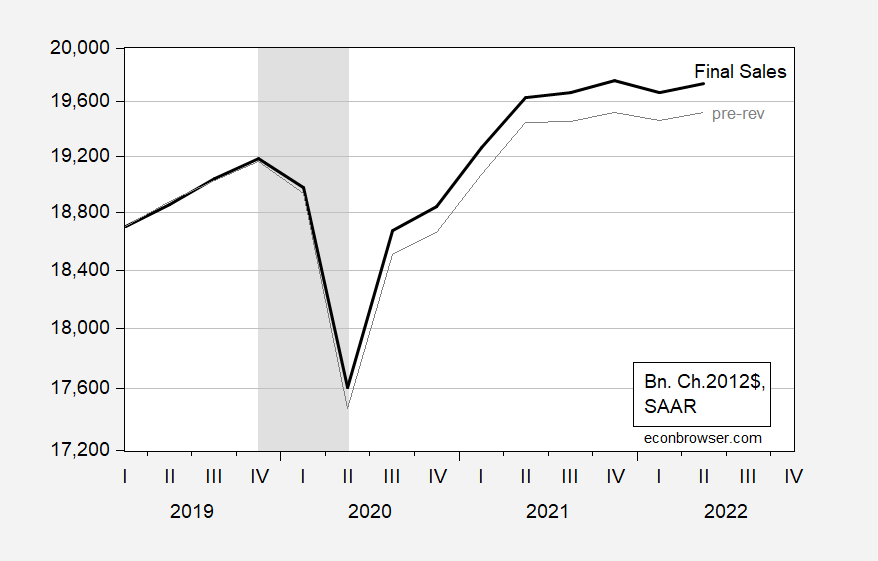

While GDP levels have risen, the downward trend in GDP over the last two quarters persists. It’s important to remember that GDP includes inventory accumulation, some of which may be needed and others not. Inventory build-up can be stripped for final sales.

Figure 4: Final sales (bold black), year-to-date benchmark revisions (grey), all in billions Ch. 2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BEA via ALFRED, NBER and author’s calculations.

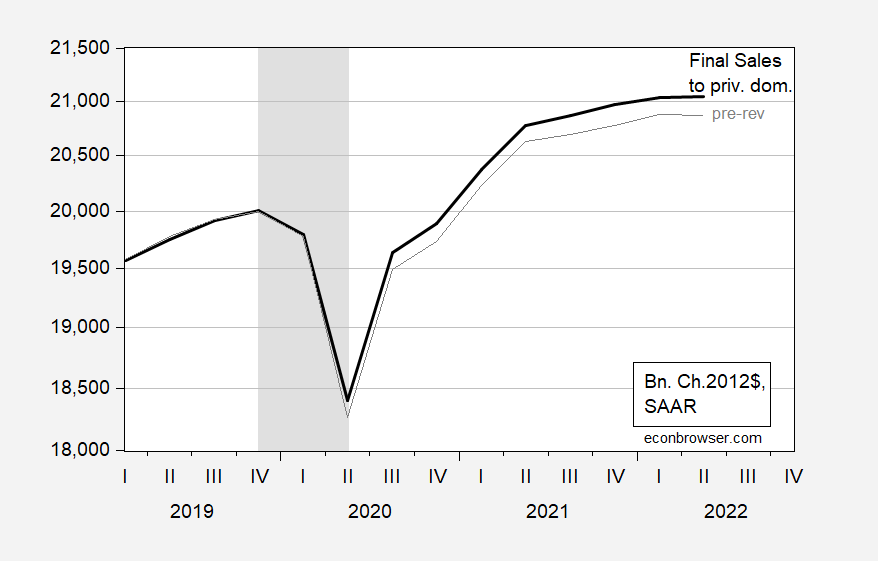

Final sales (both foreign and domestic) increased in the second quarter, but have trended sideways since the second quarter of 2021. Final sales to domestic private buyers—sometimes a measure of aggregate private domestic demand—show a similar pattern.

Figure 5: Final sales to domestic private buyers (bold black), pre-year benchmark revisions (grey), all in billions Ch. 2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BEA via ALFRED, NBER and author’s calculations.

Private domestic final sales showed more consistent growth over time, although annualized growth slowed to 0.2% q/q in the second quarter.

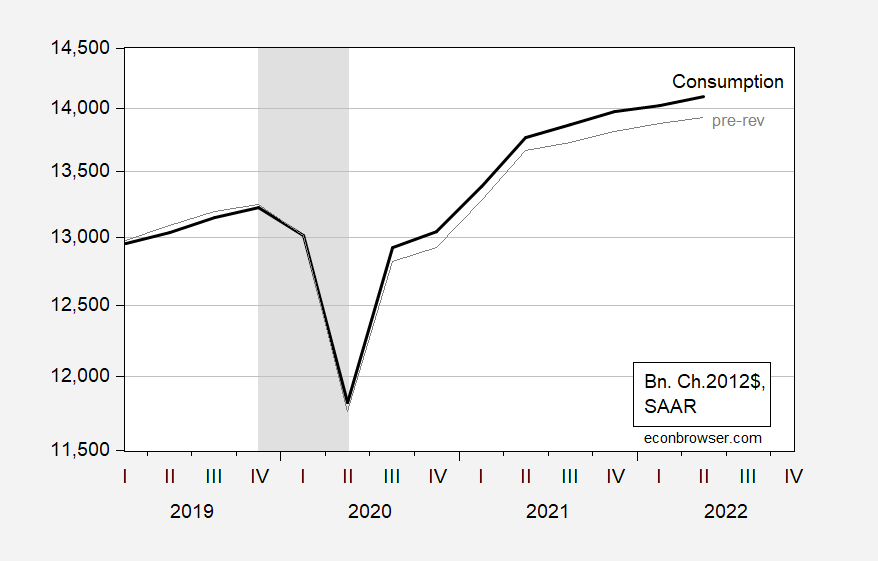

The biggest factor driving up GDP is consumption.

Image 6: Consumption (bold black), pre-year benchmark revisions (grey), all in billions Ch.2012$, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, NBER, and author’s calculations.

{kind=link}

{kind=link}