Today, we are honored to present the Laurent Ferrara (Professor of International Economics, SKEMA Business School, Paris, Chairman of the French Business Cycle Measurement Committee).

After strong growth in the second half of 2021, economic activity in France stagnated in the first quarter of 2022. Here we review the factors behind the sharp slowdown in economic activity and discuss the possible risks of a future recession.

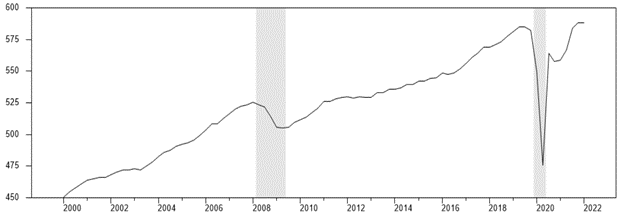

April 29, 2022 Eurostat releases preliminary GDP estimates for the first quarter of 2022 Eurozone as a whole: 0.2% month-on-month, or about 0.8% on an annualized basis, on par with US standards (see here Economy Browser Posts for analysis of U.S. GDP). This figure hides a huge heterogeneity within the region: Portugal +2.6%, Italy -0.2%. A striking figure is France’s zero growth after strong economic growth in 2021 (1.5% in the second quarter of 2021, 3% in the third quarter of 2021, and 0.8% in the fourth quarter of 2021). The French economy did recover quite quickly in 2021, with an annual GDP growth rate of 7% (see Figure 1), after a fairly stable few months of economic activity following the end of the Covid-19 recession (Q2 2020).

Figure 1. French GDP and recession since 2000

source: Insee (real GDP in billions of euros) and the French Economic Association (AFSE, Business Cycle Dating Commission)

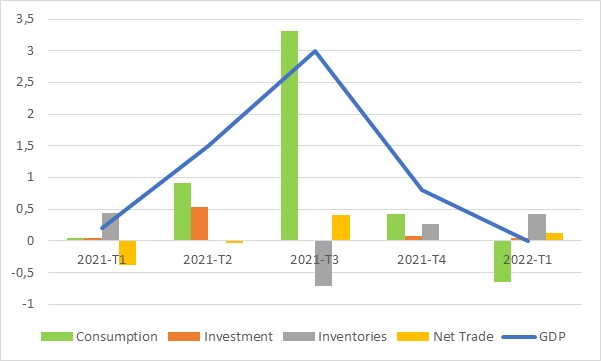

If we look at the various components of French GDP (Figure 2), the decline in Q1 2022 is due to a -1.3% drop in household consumption compared to the previous quarter. The negative contribution of consumption to GDP growth was -0.6 percentage points. Investment and net trade continued to contribute positively to GDP growth. In fact, much of the difference in GDP growth since last year has been due to changes in household consumption.

Figure 2. Contribution to GDP growth since Q1 2021

source: Insee, quarterly GDP growth rate and contribution of consumption, investment, inventory changes and net trade

What are the possible explanations for this negative evolution in household consumption in the first quarter of 2022? The first explanation is apparently the sharp rise in commodity prices, especially oil and gas, which in turn led to higher consumer prices. Strong global demand linked to supply constraints initially caused inflation to rise sharply from the end of the Covid recession.On top of that, Russia’s invasion of Ukraine from 24 February 2022 has added another layer of upward pressure on consumer prices, making Inflation in France is 4.8% in April 2022. Therefore, the decline in household purchasing power associated with rising consumer prices can be seen as the first explanation. However, we cannot rule out the fact that after months of consistent spending, we are currently seeing a normalization of household spending behavior, especially on services such as restaurants, hotels or transportation.It turns out that after the Covid recession, French families Excessive savings of approximately EUR 166 billion (12% of annual income) may be used to stimulate consumption in 2021.

Finally, heightened uncertainty in the first few months of 2022 has also led to a wait-and-see attitude among consumers, especially for big-ticket items, and precautionary savings. I am referring here to at least two types of uncertainty: (i) uncertainty driven by the Ukrainian war, seen as shock by public opinion, and (ii) political uncertainty prevailing ahead of the French presidential election in April. Certainty 24.

One of the issues currently debated in France is understanding whether the French economy is heading for a recession. Recession stages are often determined by economists using “3D” rules that simultaneously assess the duration, depth and spread of the phenomenon. So far, we’ve only seen a quarter of GDP growth at zero, meaning the “duration” criterion has not been met (at least two consecutive quarters). The “deep” criterion means that a recession would translate into a significant drop in economic activity. It turns out that periods of slightly negative GDP growth may not be considered a full-blown recession, but simply a slowdown. This was the case, for example, in France after the dot-com bubble burst in 2002-03 and during the Eurozone sovereign debt crisis in 2012-13 (see this working paper). Finally, the “diffusion” criterion means that the recession must be visible in various economic variables simultaneously (i.e. we should observe strong linkages). In this regard, in addition to GDP, French Business Cycle Dating Council Focus on employment, business investment, working hours and capacity utilization. So far, these variables have not shown any evidence of a sharp drop in economic activity. Strikingly, household consumption is not on this list because this variable is too volatile and does not exhibit characteristics consistent with business cycles.

All in all, as of today, the French economy appears to be far from recession, although it is too early to tell. In fact, identifying recessions requires more data and more time. For example, the average lag time between the onset of a recession in the US and the NBER Dating Commission acknowledgment is about 7 months.

However, it is fair to admit that some downside risks are currently affecting economic activity in France.First, the Russian invasion of Ukraine means that the macroeconomic risk for the entire euro area today is now three times that of the United States (see this post). The most important channel of transmission was the sharp rise in commodity prices, mainly oil and gas, which reduced the purchasing power of French households.In addition, the Russian government has threatened to cut off gas supplies to European countries, as it did with Poland and Bulgaria, and the EU is currently discussing the possibility of Russian oil embargo, leading to expectations of higher energy prices and final consumer prices.At some point, the ECB will have to tighten monetary policy, like Fed and Bank of England by doing so, thereby jeopardizing economic activity.

Second, the political uncertainty is not yet fully resolved, as we will hold two rounds of legislative elections from June 12 to 19, 2022, to elect the 577 members of the French Parliament. If the recently elected president, Emmanuel Macron, fails to secure a majority, he will have to nominate a prime minister with different political sensitivities, creating uncertainty about the political goals of the next presidency.

Third, the global economy is losing momentum due to the combined effects of the war in Ukraine, rising commodity prices, strict lockdowns in China, and rising central bank interest rates… According to the Global Economic Outlook, world GDP growth has been revised down to 3.6% in 2022. April IMF World Economic Outlook. This means that France cannot rely on exports to sustain economic growth.

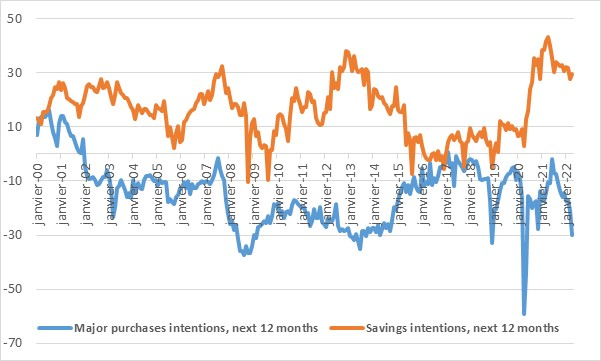

All in all, the behaviour of French families will certainly need to be closely watched over the next few months. As a preview, we can take a look at the last poll of households conducted by the French Institute for Statistics (Insee) in April (see Figure 3). We note that the willingness to save in the next 12 months remains at a high level, while the main purchasing intention for the next 12 months fell in April to levels consistent with past periods of economic stress. The widening gap between the two components of the survey is clearly not a positive sign for future consumption. However, as I mentioned earlier, in addition to GDP, variables that help determine the occurrence of a recession in France are employment, investment, hours worked, and capacity utilization. These variables will have to be closely watched over the next few months.

Figure 3. Consumer Confidence Index since 2000

source: Yingsi

This article is by Laurent Ferrara.

{kind=link}

{kind=link}