Today we publish a guest article written by: Lindsay JacobsAssistant Professor, Robert M. La Follette School of Public Affairs, University of Wisconsin-Madison.

Social Security retirement benefits are an important source of income for older American families. While the program is a distinguishing feature of modern life, it faces well-known funding challenges: its “pay-as-you-go” financing model, increasing life expectancy, and declining worker-to-retirement ratios all point to possible future funding challenges shortage. There are a number of policy changes that could address this problem, including raising the age at which people can receive “full” Social Security retirement benefits. In fact, the filing age has changed, with the full retirement age (FRA) gradually rising from 65 to 67 years.

In my ongoing research [paper]I am exploring how people in different professions have responded to these increases in FRA in the past, and how they may continue to do so in the future.

Although it is not part of the design of Social Security benefit structures, late-life work, disability, and Social Security claims patterns vary widely across populations, particularly for people in different occupations. All else being equal, people in less physically demanding white-collar jobs can and do work longer hours, while FRA increases are relatively harder to swallow for people in blue-collar jobs.

Key findings on employment and Social Security application timing.

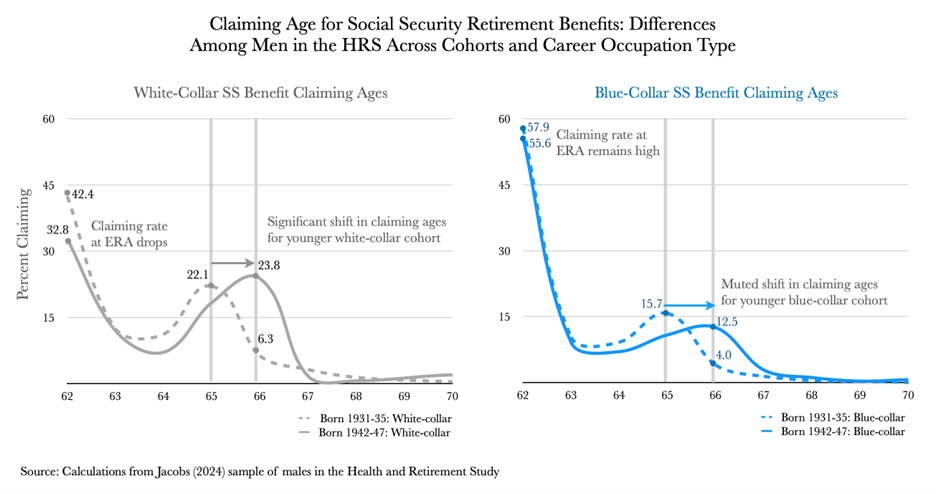

The chart below shows two interesting facts about the ages of the men born between 1931 and 1947 in the Health and Retirement Study (HRS). The first is that there are far fewer people (left) whose careers involve more white-collar jobs.Claims may be made reduce Compared with those with blue-collar work experience, the earliest age to receive Social Security benefits is 62 (right). The second is the difference in how people in later groups respond when faced with higher FRA and reduced early benefits. The solid line represents the FRA for an age group of approximately 66 years, while the dashed line represents an FRA for an older group of 65 years. Young white-collar workers tend to adjust by fewer claiming benefit reductions at age 62 and deferring them. The new FRA claim rate is 66. By comparison, the early claims rate for blue-collar workers was 62, which remained essentially unchanged despite facing significant reductions in benefits.

To understand how filing age would change with potential future increases after a future retirement age (ERA) of 62 and an FRA of 67, I estimated a behavioral model that matched the facts in the HRS data and measured Responses of different occupations to hypothetical policy changes.

Generally speaking, I find that raising the ERA by two years has a much larger impact on blue-collar workers, while raising the FRA has a much larger impact on white-collar workers. This is reflected in many measures. The major change is in filing age behavior, with approximately 70% of blue-collar workers now claiming benefits under the ERA of 64 years. The new policies also resulted in longer working years, a modest increase in pre-retirement savings, and, most importantly, an increase in the share of people applying for Social Security Disability Insurance (SSDI).

Why is this important?

This is not to say that the ERA or FRA should or should not be increased, or that the design of Social Security retirement benefits or any reform should explicitly take career history into account. However, understanding the response and the mechanisms that generate it are important for several reasons.

One motivation for thinking about the relationship between occupations and social security is to more accurately predict distributed responses to policy, something that estimates of average responses might miss, including how we might expect to see spillovers to adjacent programs like SSDI.

But another motivation is political feasibility. Last year, France's pension reform raised the retirement age from 62 to 64, which was a bit sudden for people in their 50s. This prompted an outcry, an experience that underscores the importance of accounting for idiosyncratic effects: average losses in well-being for all workers would ignore more severe losses for half of workers and underestimate the political (un)popularity of such policy changes .

A copy of the paper can be found here: https://lindsayjacobs.github.io/papers/VariedResponses-Policy.pdf.

The author of this article is Lindsay Jacobs.

{kind=link}

{kind=link}