Today we publish an article by Jeffrey FrankelHarpel Professor at Harvard University's Kennedy School of Government and former member of the White House Council of Economic Advisers. A shorter version Appearing in Project Syndicate. He thanks Sohaib Nasim for research assistance.

May 2, 2024 — Many countries are vote. Recent elections in a number of emerging market and developing economies (EMDEs) have reaffirmed the view that major currency devaluations are more likely to occur immediately after elections rather than before. Nigeria, Turkey, Argentina, Egypt and Indonesia are the five countries that experienced post-election currency devaluations last year.

election-devaluation cycle

Economists will remember 50 year old paper Proposed by Nobel Prize winner Professor Bill Nordhaus, who essentially pioneered the study of political business cycles (PBC). The People's Bank of China cited the government's general preference for fiscal and monetary expansion in the year leading up to the election in the hope of re-electing the current president or at least the current political party. The idea is that output and employment growth will accelerate before the election, boosting the government's popularity, while the main costs in terms of debt problems and inflation will emerge after the election.

But groundbreaking Nordhaus's paper (1965) also include forecasts of foreign exchange cycles that are particularly relevant to emerging market economies. That is, countries typically seek to shore up the value of their currencies before elections, depleting their foreign exchange reserves if necessary, only to experience currency depreciation after elections.

Nordhaus writes: “Concerns about reserve losses and balance of payments deficits are predicted to be greater at the beginning of an electoral system and less at the end of an electoral system… Making strides in a democracy The basic difficulty with period selection is that the implicit weighting function for consumption has positive weights during the election period and zero (or very small) weights in the future.

An incoming government may deliberately implement a currency devaluation, choosing to avoid an unpleasant step—an unwelcome increase in inflation—while still being able to blame the previous government. Alternatively, currency depreciation could manifest itself in the form of an overwhelming balance of payments crisis shortly after the election. Either way, governments have an incentive to hoard international reserves early in their term and use them more freely to defend the currency toward the end.

Political leaders are almost twice as likely lose office Within six months of a significant currency devaluation, especially in presidential democracies. Why is devaluation so unpopular that governments are afraid to devalue before elections? In the traditional textbook model, currency depreciation stimulates the economy by improving the trade balance. But devaluation always triggers inflation. In addition, currency depreciation in emerging market and developing economies tends to lead to a contraction in economic activity, particularly adversely affecting the balance sheets of domestic borrowers with dollar-denominated debt.

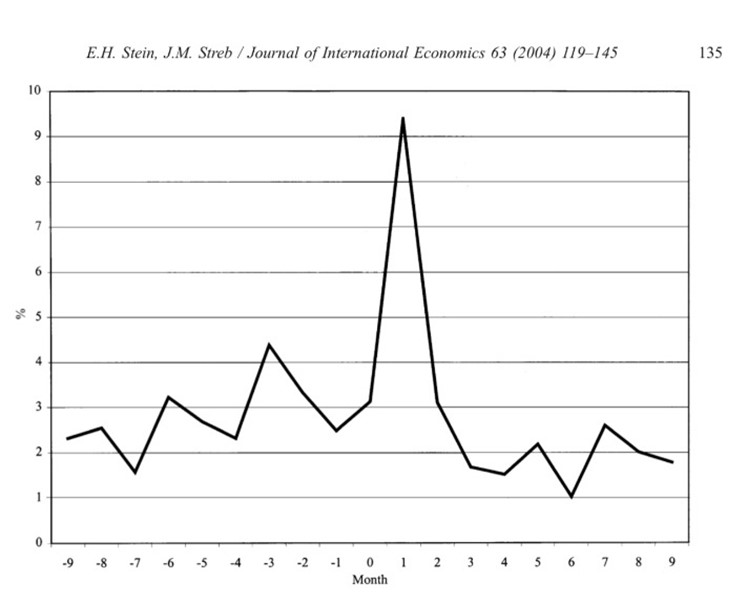

The development of political devaluation cycle theory series of document go through Ernesto Stein and co-authors. One might think voters would be wise to understand these cycles and vote against a leader who secretly delays necessary currency adjustments. But lacking information about the true nature of politicians, voters may actually act rationally. Stein and Streb (2005) chart shows that currency depreciation is more common after a change of government. (The sample covers 118 changes in 26 countries in Latin America and the Caribbean between 1960 and 1994, excluding coups.)[1]

figure 1: Average depreciation patterns before and after elections.

There has been some depreciation over the past year

Many emerging market and developing economies have been facing balance of payments pressures over the past two years. One factor is that the Federal Reserve will raise interest rates sharply in 2022-23, and interest rates will currently remain at higher levels for longer than the market expected. As a result, international investors find U.S. Treasury securities more attractive, while emerging market and developing economy loans and securities less attractive.

A good example of a political devaluation cycle is Nigeria. Africa's most populous country held a controversial presidential election on February 25, 2023. naira. Nigeria's new President Bola Tinab took office on May 29, 2023. depreciated Naira rises 49% [from 465 naira/$, to 760, computed logarithmically]. This soon proved insufficient to restore the balance of payments.at the end of January In 2024, the government abandoned efforts to prop up the official value of the naira, depreciation Another 45% [from 900 naira/$ to 1,418, logarithmically].

The second example is Türkiye's May 2023 elections. It was widely derided as the idea that it would reduce soaring inflation – while intervening to support the lira's value. Government guarantees that Turkish bank deposits will not depreciate in value, expensive and prolong currency overvaluation in an unsustainable manner. back election, lira used to be Instantly depreciated, as predicted by theory. The currency continues to lose value throughout the rest of the year.

Next, on November 19, 2023, Argentina A candidate, Javier Milei, was unexpectedly elected president.often describe A far-right liberal, he is not from any established political party. He ran on a platform of drastically reducing the government's role in the economy and abolishing the central bank's ability to print money. Mire was sworn in on December 10. peso go through more than half [a 78 per cent devaluation, computed logarithmically, from 367 pesos per dollar to 800].At the same time, he introduced restrictions on government spending such as energy subsidies, quickly achieved a budget surplus, and launched comprehensive reform.Argentina's inflation remains high, but central bank halts FX losses reserve After depreciation, it was again as predicted by the theory.

The fourth example is Egypt, where President Abdel Fattah el-Sisi just started his third term on 2 April. crisis It's been a while.Nonetheless, the government has ensured that its overwhelming re-election December 10-12, 2023, by Delay Unpalatable economic measures, not to mention prevention Serious Opponent runs.widely anticipated depreciation of this egyptian pound45%, last month, March 6, 2024 [from 31 pounds/dollar to 49, logarithmically].This is part of enhanced access International Monetary Fund Programwhich also includes the often unpopular monetary and financial disciplines [with disbursal approved by the IMF Executive Board on March 29].

Finally, in IndonesiaPopular but term-limited President Joko Widodo will soon be succeeded by Defense Minister Prabowo Subianto, who is less popular but has the support of the current president in the February 14 elections .Rupee has been depreciated since the results of the disputed presidential vote were announced on March 20.almost to all-time highs Record The exchange rate against the US dollar was at a low on April 16.

What's next?

Of course, the link between elections and exchange rates is not inevitable. India are experiencing election now and Mexico Will be in June. But neither seems particularly in need of major currency adjustments.

Bolivia is one of the candidates for the election-devaluation cycle. The country is deeply divided politically over former President Morales' ability to run in elections scheduled for 2025.

Venezuela is scheduled to hold presidential elections in July. Like some other countries, election It was expected to be a sham as no major opposition candidate was allowed to run.Due to long-term mismanagement, the economy has fallen into chaos, with recent hyperinflation and long-term overrated Bolivar. But the same government that essentially banned political opposition also essentially banned the purchase of foreign currency. Therefore, the foreign exchange market may not return to equilibrium for a long time.

To avoid currency devaluation, these countries are doing more than just spending their foreign exchange reserves. They often use capital controls or multiple exchange rates instead of allowing free financial markets. This does not mean that post-election currency devaluations no longer exist. It simply leaves the government longer without having to adapt to the reality of macroeconomic fundamentals. Unfortunately, many of these countries also do not allow for free and fair elections, which also eliminates the need for governments to respond to the verdict of voters.

refer to

Broz, J. Lawrence, Maya Duru, and Jeff Redden.Policy responses to balance of payments crises: the role of elections,” open economy review, 27, No. 2, pp. 207-227.

Frankel, Jeffrey, 2005, “Austerity Monetary Collapse in Developing Countries” International Monetary Fund Staff Papers. flight. 52, no. 2. NBER Working Paper No. 11508.

Pease, Jeffrey, and Ernesto Stein, 2001,”The political economy of exchange rate policy in Latin America: an analytical overview”. Edited by Jeffrey Frieden and Ernesto Stein. The Currency Game: Exchange Rate Politics in Latin Americapp. 1-20.

William Nordhaus, 1975, “political and economic cycle,” Economics revised edition. study Volume 42, Issue 2, April 1975, Pages 169-190.

Quinn, Dennis, Thomas Sattler, and Stephen Weymouth, 2023, “Do Exchange Rates Affect Voting? Evidence from Democracies Election and Survey Experiments”. International organizations 77. No. 4, 789-823.

Stein, Ernesto H., and Jorge M. Streb, 1998, “Political stability cycles in high-inflation economiess,” Journal of Development Economics,159-180.

Stein (Ernesto H.) and Jorge M. Streb (Jorge M. Streb). year 2004,”elections and this Timing of currency devaluation”. Journal of International Economics 63, no. 1:119-145.

Stein, Ernesto H., Jorge M. Streb, and Piero Ghezzi, 2005, “Real exchange rates revolve around election cycles.” Economics and Politics 17. No. 3:297-330.

David Steinberg, 2015, Demand for devaluation: exchange rate politics in developing countries (Cornell University Press).

Footnote:

[1] include Frieden and Stan (2001) and Stein and Streb (2001)1998, year 2004, 2005). recent, Quinn, Sattler and Weymouth (2023) find that voters punish leaders who devalue, especially when the currency is already undervalued. Steinberg (2015) find that in countries with strong manufacturing industries, they are more likely to welcome a weak currency.

The author of this article is Jeffrey Frankel.

{kind=link}

{kind=link}