Today, we are pleased to present the contribution of our guest Miklos Warri (Bank of France). The views expressed in this article are those of the author and should not be attributed to the Banque de France or the Eurosystem.

Some details were lost in the course of SVB’s demise, and with it potentially a lot of taxpayer money. The Fed announced seemingly innocuous details as it rolled out its latest program, Bank Term Funding Program (BTFP) Designed to stop panics:

“Additional funding will be provided through the creation of a new Bank Term Financing Program (BTFP) to provide loans for up to one year to banks, savings associations, credit unions, and other eligible depository institutions against U.S. Treasury, agency debt and mortgage-backed securities, as well as other eligible assets as collateral. These assets will be valued at par” (emphasize).

This may seem like a small accounting practice that most people won’t notice, but it could be a turning point for the Fed and central banks in general. In fact, it is common practice for central banks to value bonds held as collateral not at face value, but using their market value, or the best estimate of their market value when they are not traded in a liquid market . This is because when central banks lend money to banks, they demand protection in the event of bank default. In the event of a bank failure, the central bank becomes the owner of the pledged collateral. Central banks restore the value of assets by selling them in the market or by holding them to maturity. Since the current market value of bonds is generally strictly lower than the face value (also known as the face value), if the bank defaults, the loss of the central bank is equal to the difference between the face value and the market value. This difference can be attributed to the unexpectedly rapid rate hikes by the Federal Reserve since 2022, which mechanically depresses the market value of all bonds. Use the US authorities own world:

“Because of higher interest rates, longer-maturity assets that banks acquired when interest rates were lower are now worth less than their face value.”(FDIC, March 6, 2023)

Some estimates give us an idea of the size of the gap.example data form dallas federal reserve bank shows that, as of February 2023, the market value of the privately held total federal debt stock was $1.5 trillion below par. FDIC says Bank of America’s unrealized securities losses by the end of 2022 will be $620 billion.

When the BTFP was introduced, who could have predicted how many banks would have borrowed from it, failed to pay it back, and left behind collateral whose market value was strictly lower than the loan they had contracted from the US central bank?Intake at the facility has grown steadily since launch, surpassing $68 billion as of April 6day. So while it’s impossible to know whether the Fed will end up taking any losses, it’s safe to assume that it explicitly takes the risk of doing so by valuing the collateral at face value, and that loss could amount to around 8 cents ( difference between market and face value) for every dollar lent.

To be sure, these are not potential “paper losses,” “accounting losses,” or “subjective losses” facing the Fed. If failing banks were left with only face-value collateral in exchange for their defaulted loans, it would amount to a loss of real economic resources for the U.S. central bank.

The Fed would obviously suffer losses if it sold the acquired collateral in the market, but it would also do so if it held the debt until maturity. Statement that the market value of debt is less than its face value is equivalent to saying that US debt is paying a coupon below the market rate (coupon/par value < market rate).

For example, in the event of a default, the Fed could own debt that yields 1% on par per annum, while the Fed pays interest on its newly created liabilities (to “fund” bank loans), currently between 4.8% and 4.9%. This negative rate is carried forward over the life of the bond and is equivalent to the difference between the face value and the market value.

This discrepancy will cost the public institution the Federal Reserve dearly. But do Fed losses matter? I think it does. The Fed is backed by $25 billion in Treasury funds, which are also taxpayer property.[1] Beyond that $25 billion, things get a little more complicated, but not much better.

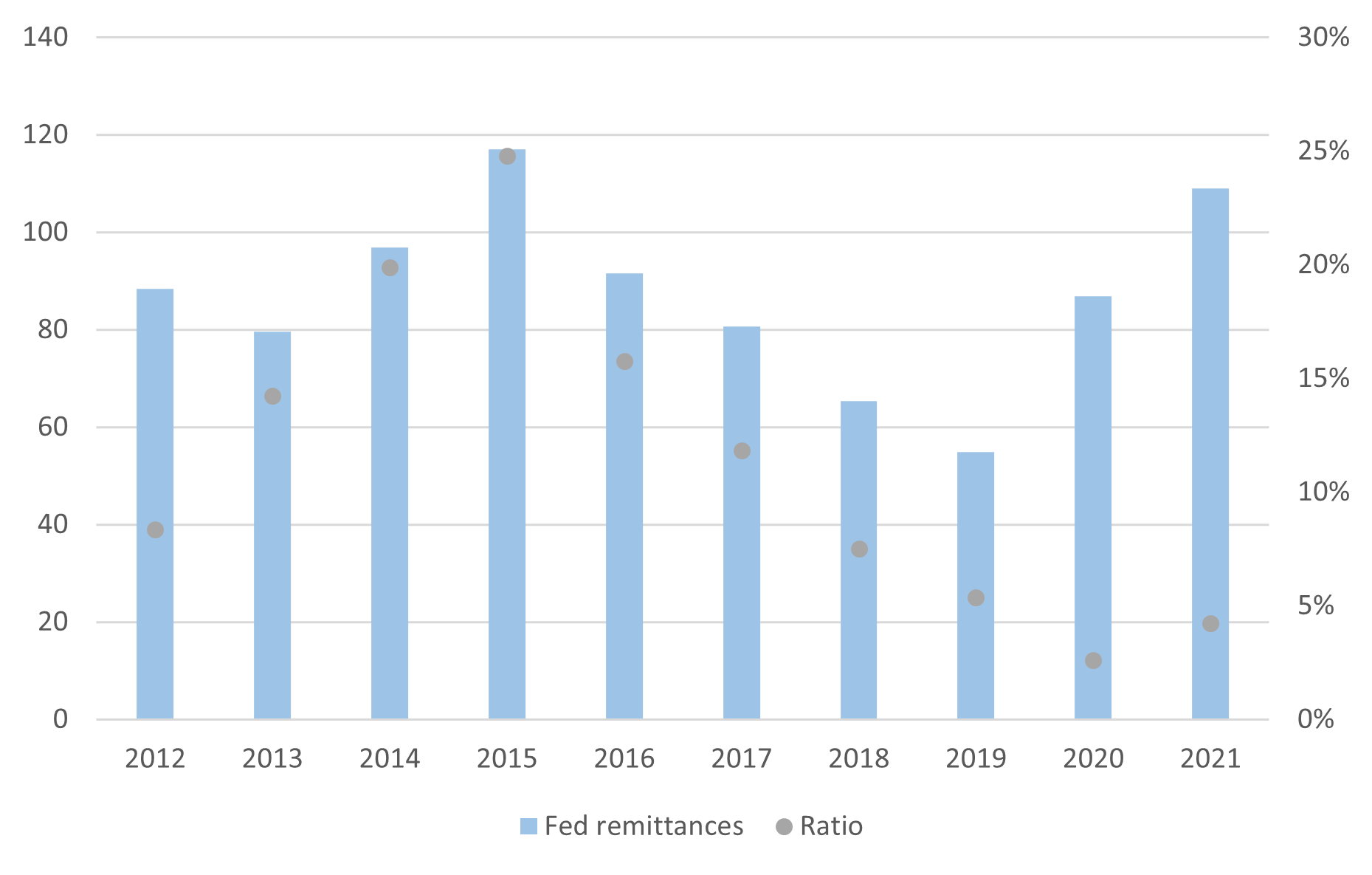

Over the period 2012-2021, the Fed remitted an average of $87 billion per year (Figure 1), accounting for 11% of the total annual deficit and as high as 25% of the deficit in 2015. In other words, the US federal deficit would have been 25% higher in 2015 without any revenue coming from the Fed. Higher deficits mean higher market borrowing, and taxpayers paying bondholders more interest. In short: Any losses to the Fed reduce payments to the Treasury, increase the federal deficit, and force the Treasury to borrow more money from creditors and pay more interest. The Fed has already suspended payments to the Treasury after taking losses on its bond portfolio in 2022. Any additional losses would delay the date of its return to practice.

Valuing collateral at face value isn’t just harmful to U.S. taxpayers. It also sets a precedent for central banks in other parts of the world.this International Monetary Fund Promote “appropriate valuation and risk control measures” to all countries when dealing with monetary policy collateral.[2] The Fed’s example may be replicated abroad. In addition to the central bank, the Federal Reserve, independent body of the executive branch There are concerns about the independence and distribution of power of the central bank that a decision has been made that could have important fiscal implications and thereby potentially interfere with the “fiscal powers” of Congress. Finally, I’ll quote a saying I’ve heard throughout my career in central banking: “In God we trust, all others must provide (good) collateral”

figure 1: Fed remittances to the Treasury (left axis, billions) and comparison to the US federal deficit over the same period (right axis, percentages)

source: the fed annual report For remittances, assume the reported figures are for the calendar year (i.e. not the U.S. fiscal year) and FRED Monthly Series deficit over the years.

notes

[1] this Congressional Research Service “This could be controversial as it was not the fund’s original intended use and similar conduct has been prohibited in the past,” it said.

[2]instant messenger Sayu wait. (2008)It also states that “valuing at face value is a simplistic approach that can substantially overstate the net present value of bank loans”, which is basically true for any asset.

This article was sponsored by Miklos Warri.

{kind=link}

{kind=link}