Today we are happy to introduce Zhong Linhe (Senior Economist), M. Ayhan Coss (Chief Economist and Director) and Franziska Onzog (manager) From the World Bank Outlook Group. The findings, explanations and conclusions expressed in this blog are entirely the author’s. They do not necessarily represent the views of the World Bank, its executive directors, or the countries they represent.

The COVID-19 pandemic has plunged the global economy into its worst recession since World War II. In the context of the collapse of demand and the collapse of oil prices, global consumer price inflation fell by 0.9 percentage points between January and May 2020 (Figure 1). Compared with emerging markets and developing economies (EMDE), this decline in advanced economies is about one-third higher.

However, since May 2020, inflation has picked up. By April 2021, inflation in advanced economies and emerging markets and developing economies has risen to pre-pandemic levels. The rise in inflation is widespread, occurring in about four-fifths of countries. Therefore, of the five global recessions in the past 50 years, following the mildest decline in inflation, the global recession in 2020 is characterized by the fastest rise in subsequent inflation.

Figure 1. CPI inflation

source: Haver Analytics, IMF International Financial Statistics, World Bank. notes: The median year-on-year overall consumer price index (CPI) inflation for a sample of 81 countries, of which 31 are advanced economies and 50 are emerging market economies.

Looking ahead, as the global economy gradually reopens, monetary and fiscal policies continue to support the recovery, and the pent-up demand of advanced economies is being released. For major advanced economies, some people worry that the confluence of such factors may produce significant inflationary pressures (Summers 2021; Blanchard 2021; Landau 2021).

In contrast, others believe that there is nothing to worry about, at least for many advanced economies, because of the temporary nature of price pressures, solid inflation expectations, and structural factors that are still suppressing inflation (Ball et al. 2021; Gopinath 2021; Krugman 2021; Powell 2021; Clarida 2021).

In a new study, we analyzed the main drivers of recent developments in global inflation and considered the inflation outlook in the coming months (Ha, Kose and Ohnsorge 2021).

Drivers of recent inflation trends

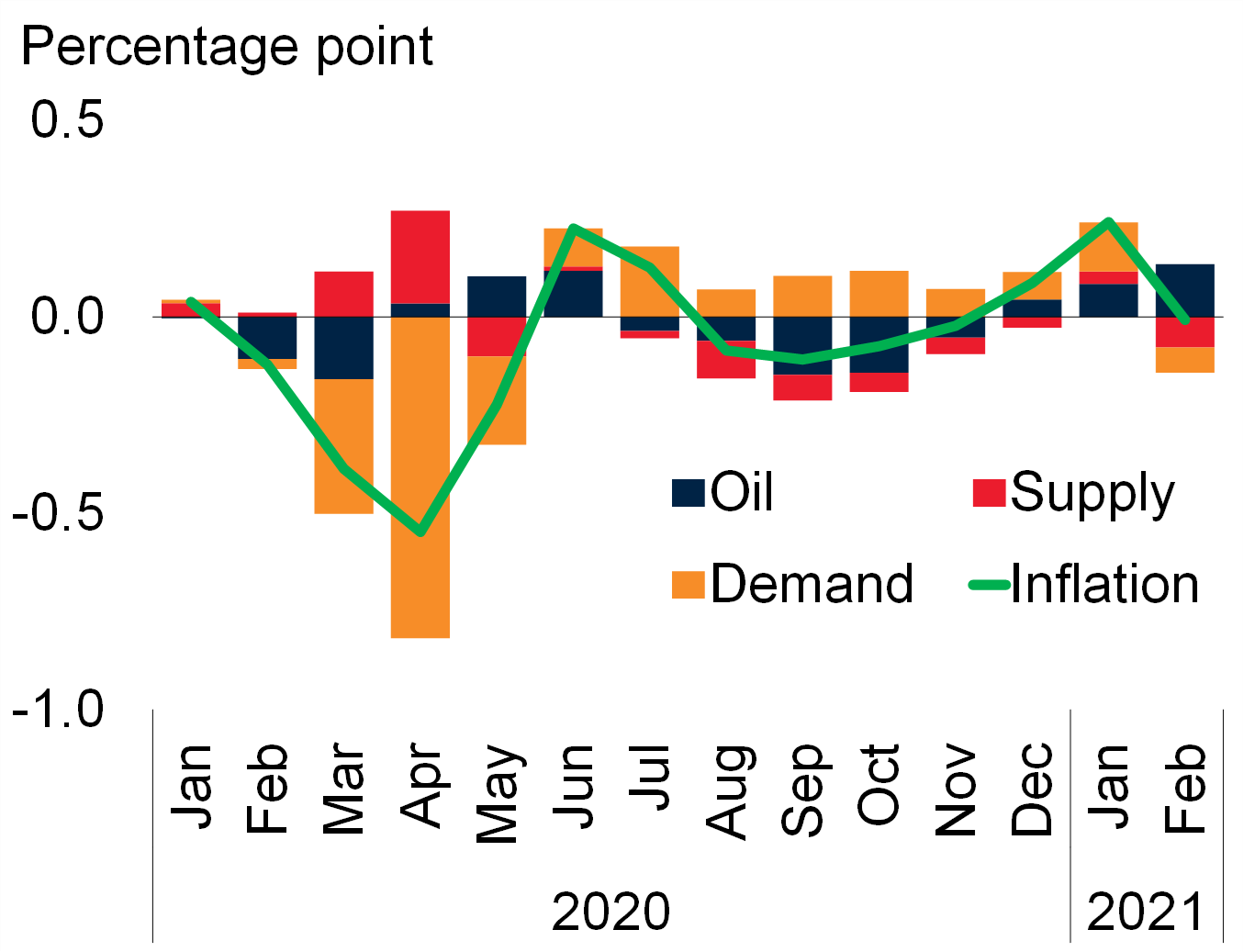

During the pandemic, fluctuations in aggregate demand, oil price trends, and supply disruptions have led to the development of global inflation. We estimate the role of each factor in the factor-enhanced vector autoregressive (FAVAR) model, which consists of global inflation, global output growth, and oil prices. The model deviates from recent work in this field in three dimensions (Charnavoki and Dolado 2014; Ha et al., 2019) to adapt to the 2020 pandemic. First, the model uses monthly data instead of quarterly or annual data to minimize concerns about the endogeneity between variables. When the pace of recession and recovery are different, it is especially important to use monthly data. Second, in addition to the standard symbol restrictions, an additional set of narrative restrictions was imposed during periods of large fluctuations in oil prices. Third, the model allows the volatility of global variables over time to reflect the huge fluctuations of these variables around the global recession and oil price shocks.

The estimation results indicate that a series of constantly changing anti-inflationary forces were subsequently lifted from January to May 2020 (Figure 2).

- January to May 2020Four-fifths of the decline in global inflation reflects the collapse of global demand, as consumption and investment have fallen sharply under the lockdown and uncertainties in policy and growth prospects. Another one-fifth reflects the plunge in oil prices. However, during these five months, the forces affecting inflation have changed. In February and March 2020, due to the collapse of oil prices and the collapse of global demand, the decline in global inflation was almost equal, but the impact of deflation in April of the collapse of global demand intensified.

- From June 2020 to February 2021. Starting in June 2020, with the rebound in international trade and global manufacturing activities, supply factors have begun to reduce inflation. However, as consumption shifts from face-to-face transactions to online transactions, the sharp rebound in demand has pushed up inflation. Between June 2020 and February 2021, demand pressures accounted for almost all of the reasons for the rise in global inflation, but these pressures were partially offset by improved supply conditions.

Figure 2. Contribution to monthly changes In global CPI inflation: 2020-21

source: Ha, Kose, and Ohnsorge (2021). notes: According to FAVAR estimates, 81 countries (of which 31 are advanced economies and 50 are EMDE) contributed to the year-on-year change in overall consumer price inflation last month. Monthly data. The residuals are omitted in the figure.

Near-term inflation outlook

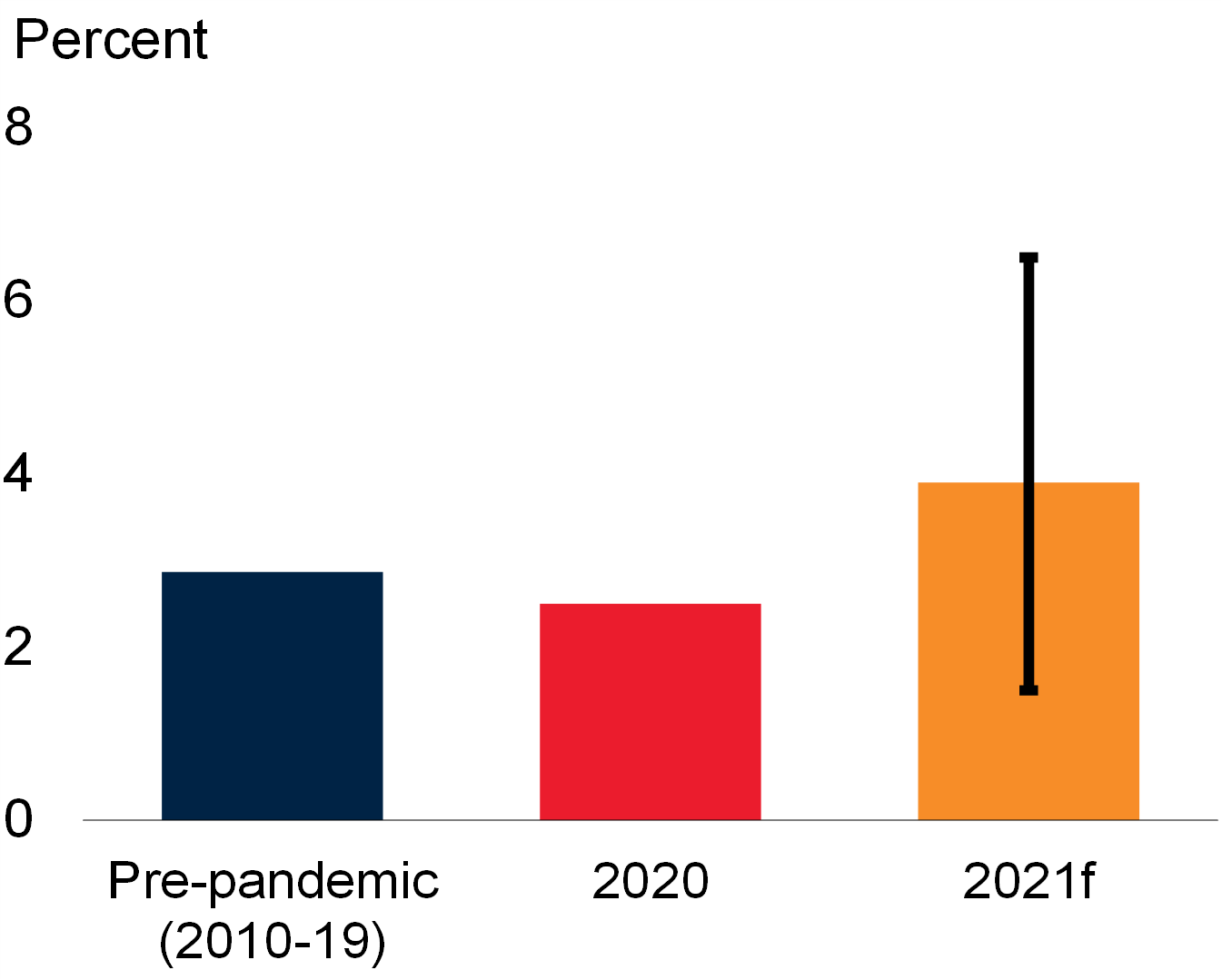

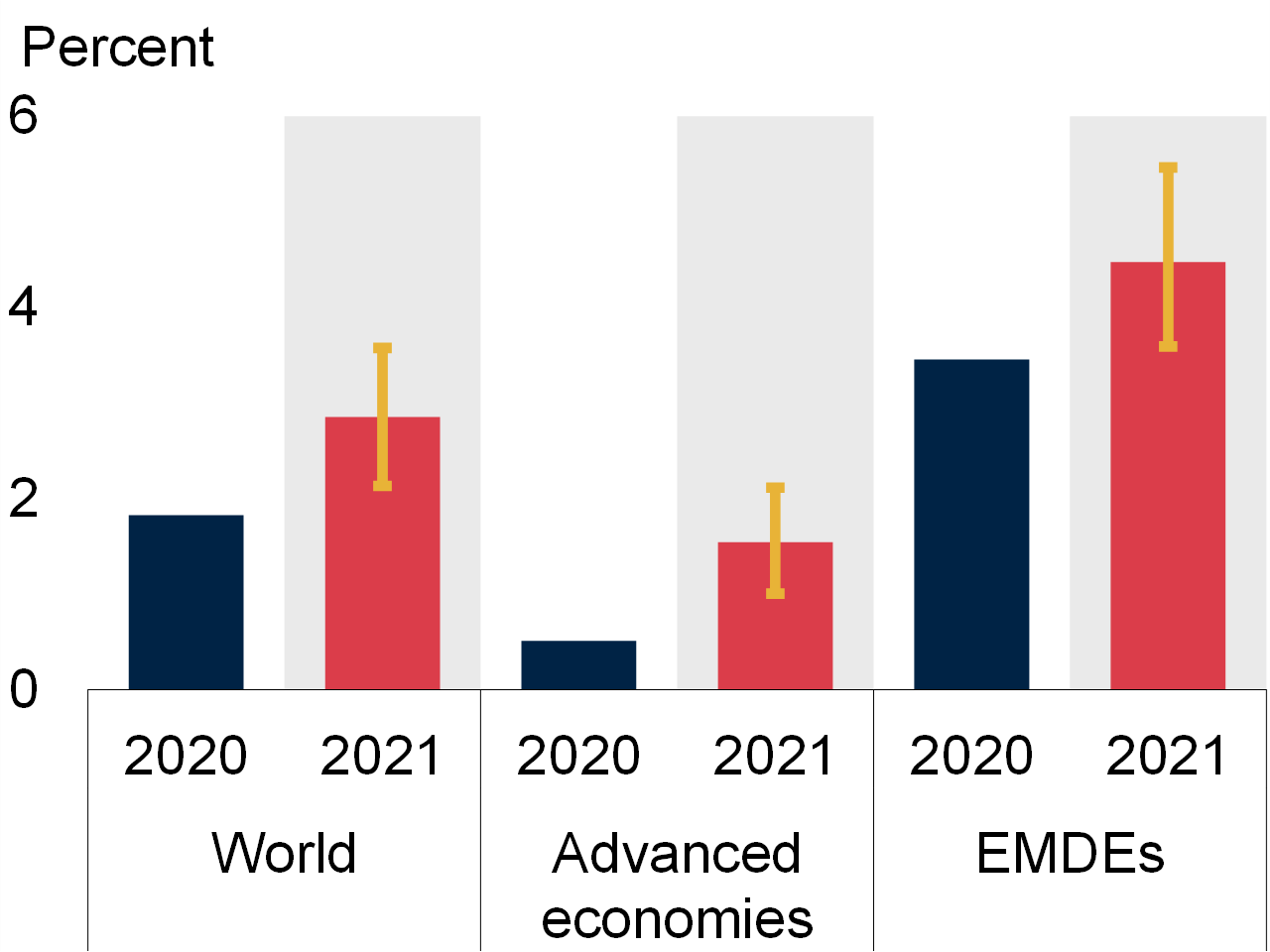

The global recession in 2020 is exceptionally severe, but it is short-lived. This is also reflected in the development of inflation. The accompanying decline in inflation was unusually mild and short-lived. Looking ahead, some factors indicate that inflation will rise in the short term, but inflation will remain stable in the long term.The same FAVAR model is used to predict global, advanced economies and EMDE inflation in the coming months, which is consistent with the growth and oil price forecasts proposed in June 2021 Global Economic Outlook World Bank report.

- Global inflation. The global output growth rate is expected to be 5.6% in 2021, and the annual average oil price is expected to be US$62 per barrel (World Bank 2021). This indicates that the global inflation rate will rise by 1.4 percentage points in 2021 (from 2.5% in 2020 to 3.9% in 2021; Figure 3).

Figure 3. Model-based inflation outlook

source: Ha, Kose, and Ohnsorge (2021). notes: Seasonal factors based on global inflation, global GDP growth and oil price growth enhance the VAR model’s conditional forecast of global inflation. The vertical lines represent 16-84 confidence intervals.

- Inflation in advanced economies. In advanced economies, the inflation rate is expected to rise to 1.8% in 2021 (from 0.5% in 2020)-slightly higher than the 1.4% average in the 2010s. For almost all advanced economies, the moderate increase in inflation predicted by the model will bring inflation closer to the inflation target.

- Inflation in EMDE. For emerging markets and developing economies, estimates indicate that the inflation rate will rise from 3.1% to 4.6%, much higher than the 2010s average of 3.8%. This will be slightly higher than the middle range (3.8%), but still below the 5.1% upper limit of EMDE’s target range for average inflation.

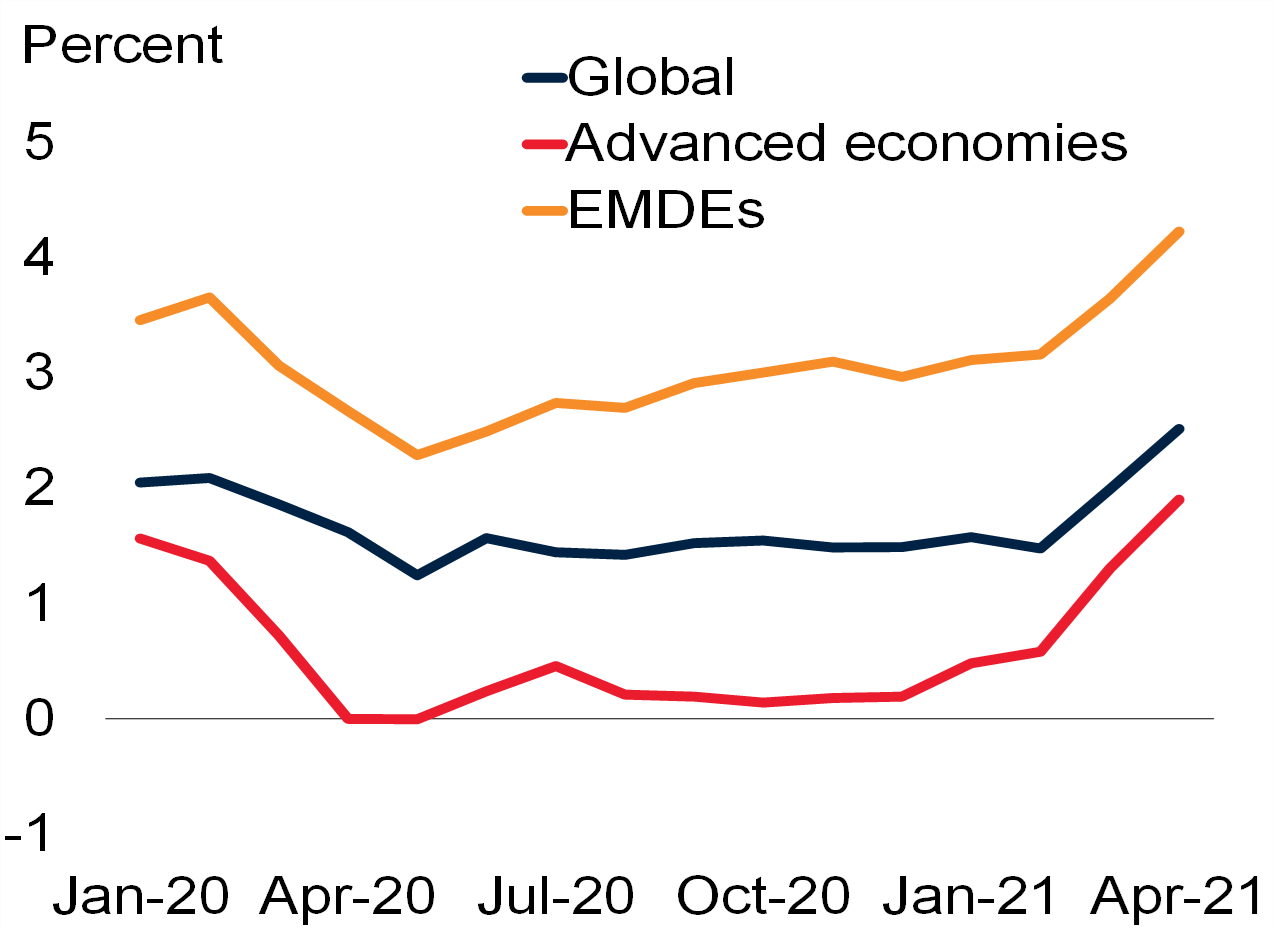

Inflation expectations. Consistent with model-based inflation forecasts, survey-based consumer price inflation expectations indicate that global inflation in 2021 is expected to rise by approximately 1 percentage point from the low level in 2020 (Figure 4). In advanced economies and emerging market economies, the expected increase in inflation is widespread. The forecasts of major central banks on overall CPI inflation also indicate that inflation will rise moderately in 2021 (the G7 economies will increase by 1.5 percentage points, and the seven large emerging market economies will increase by 1.2 percentage points). Finally, although the data is limited to a few advanced economies, market-based inflation expectations point to a similar conclusion: break-even implied inflation (measured by the spread between nominal and actual 5-year bond yields) since April 2020 It has risen since January, and rebounded to reach pre-pandemic levels in January 2021.

Figure 4. Survey-based inflation outlook

source: Consensus Economics, International Monetary Fund World Economic Outlook, World Bank. notes: According to the survey of 57 countries (31 advanced economies and 26 emerging market economies) in May 2021, the average overall CPI inflation expectation in 2021 is derived. 2020 represents the actual inflation rate. Yellow whiskers indicate maximum and minimum responses.

Policy impact

As global economic growth stabilizes at a low level, commodity prices stabilize and supply bottlenecks are eased, inflation is expected to slow after 2021. In the long run, well-anchored inflation expectations indicate that inflation will continue to be low and stable. As long as expectations remain stable and any increase in inflation-even above the target range-is temporary, a monetary policy response may not be required. However, if policymakers are unable to maintain inflation expectations at an anchored level, the short-term rise in inflation may continue in the long-term.

Structural factors—such as demographics, the forces of globalization, and improvements in policy frameworks—support the deflation of the past decade. However, if the recovery of the pandemic coincides with the turning point of some of these forces, the expected inflation rebound in 2021 may continue and, in emerging market economies, may undermine inflation expectations. Concerns about poorly anchored inflation expectations and the possibility of permanent increases in inflation may force the central banks of emerging markets and developing economies to tighten monetary policy earlier or more strongly than their cyclical stance guarantees.

If concerns about the inflation outlook in advanced economies cause investors to reassess inflation risks and lead to a sudden increase in global borrowing costs, some emerging market economies may also need to adopt similar policy responses. In emerging market economies with flexible exchange rates and limited financial vulnerabilities, currency depreciation may help cushion part of the impact of tightening financial conditions on economic activities. However, in other emerging market economies, concerns about financial stability may force the central bank to tighten monetary policy, which is beyond the range guaranteed by the strength of its economic recovery. Partly due to concerns about financial stability and inflation expectations, some EMDE central banks that implemented expansionary monetary policies in 2020 have begun to tighten their policies in 2021.

refer to

Ball, L., G. Gopinath, D. Leigh, P. Mitra, P. Mishra and A. Spilimbergo. 2021. “US inflation: ready to take off?“VoxEU.org, CEPR Policy Portal, May 7.

Blanchard, O. 2021. “Defend concerns about the $1.9 trillion rescue plan. ” Peterson Institute for International Economics Blog, February 18th.

Charnavoki, V. and J. Dolado. 2014.”The Impact of Global Shocks on Commodity Exporting Economies: Lessons from Canada. ” American Economic Journal: Macroeconomics 6 (2): 207-237.

Clarida, R. 2021. “U.S. Economic Outlook and Monetary Policy. “Speech at NABE International Symposium, May 12th.

Gopinath, G. 2021. “Structural factors and central bank credibility limit inflation risk. ” IMF blog, February 19.

Ha, J., MA Kose, F. Ohnsorge, and H. Yilmazkuday. 2019. “Sources of inflation: global and domestic drivers. ” exist Inflation in emerging and developing economies: evolution, drivers and policies, Edited by J. Ha, MA Kose, and F. Ohnsorge, 143-204. Washington, DC: World Bank.

Ha, J., MA Kose, and F. Ohnsorge. 2021. “Inflation during the pandemic: what happened? What’s next?“Working paper DP 16328, CEPR.

Krugman, P. 2021. “Re-examine stagflation. Have we got the whole macro story wrong?” Krugman out (Blog), February 5th.

Landau, J. 2021. “Inflation and Biden Stimulus. “VoxEU.org, CEPR Policy Portal, February 8.

Summers, L. 2021. “Inflation risk is real. ” Washington post. May 24.

World Bank. 2021. Global Economic Outlook. June. Washington, DC: World Bank.

This article was written by Jongrim Ha, M. Ayhan Kose, and Franziska Ohnsorge.

{kind=link}

{kind=link}