Today, we are happy to introduce John G. Fernard, Jack Muller and Mark M. Spiegel (All San Francisco Federal Reserve Bank). Our views are our own, not necessarily the views of the Federal Council or the Federal Reserve Bank of San Francisco.

China announced quarterly growth data for 2021 as of the third quarter, which is far below its strong pre-pandemic trend. In the first half of 2021, the announced quarterly average annual growth rate was 2.8%, but the annual growth rate in the third quarter slowed to only 0.8%. Not surprisingly, these numbers are far below the super-large growth rate in the last three quarters of 2020, when the economy rebounded from the deep trough of the pandemic, with an annual growth rate of 24%. The data for 2021 is also far below the trend rate of about 6% before the pandemic in China.

In this Ecobrowser article, we use the quarterly version of the FRBSF China Cyclical Activity Tracker (China CAT) to assess the recent pace of China’s economic slowdown. Chinn (2021) discussed the discrepancies between China’s reported quarterly GDP growth (the data we calculated annually and quoted above) and other published GDP data. In addition, multiple studies have raised widespread concerns about the accuracy of China’s GDP data. Nakamura, et al (2016) found that official total consumption data is “too smooth” relative to the standard theoretical expectations. Pinovsky and Sala-i-Martin (2016) found that, as measured by satellite data, China’s reported GDP growth rate appears to be unusually high relative to its light emission growth. Chen, Chen, Hsieh, and Song (2019) used both value-added tax data and local indicators that are not conducive to manipulation, and estimated that the 2010-2016 GDP growth was 1.8 percentage points lower than the report.

FRBSF China CAT [Fernald, Hsu, and Spiegel (2021)] Use economic activity indexes (such as electricity, railway transportation, and industrial production) to check the accuracy of China’s statistical data. These indexes are converted into weighted averages of various economic activity indicators in China. The statistical technique we use to create these weighted averages, called principal components (PC), provides an indicator that captures as much of the variability in a single series as possible. Conceptually, the index is similar to the Chicago Fed National Activity Index in the United States (see, for example, Brave 2008).

In order to choose among a large number of possible activity indicator combinations, Fernald, Hsu, and Spiegel (2021) considered the relationship between various indicator combinations and China’s actual imports, as measured by trading partners’ exports to China. For countries with reliable statistical agencies, actual imports are closely related to actual GDP. Importantly, our method provides external verification because trading partners’ exports are not subject to manipulation by the Chinese authorities or statistical errors. (We estimate all the relationship between the U.S.-China trade dispute in the late 2010s and before the pandemic.)

The resulting China CAT series is updated quarterly, including data and additional documents (Available on the website of the Federal Reserve Bank of San Francisco). This series uses year-on-year data and has a mean of zero and a unit standard deviation. (Hence, the series focuses on volatility and remains silent on whether the trend is properly measured.)

However, we are currently interested in the latest decline in China’s economic growth, and the year-on-year data has been severely affected by the large fluctuations in the level a year ago. Therefore, we have now constructed a new quarterly version of China CAT, which we call “QCAT”. Although the base series are normalized to have zero mean and unit standard deviation, we report them here as “GDP units” by scaling them by the standard deviation of GDP and adding back the estimated trend to the reported GDP .

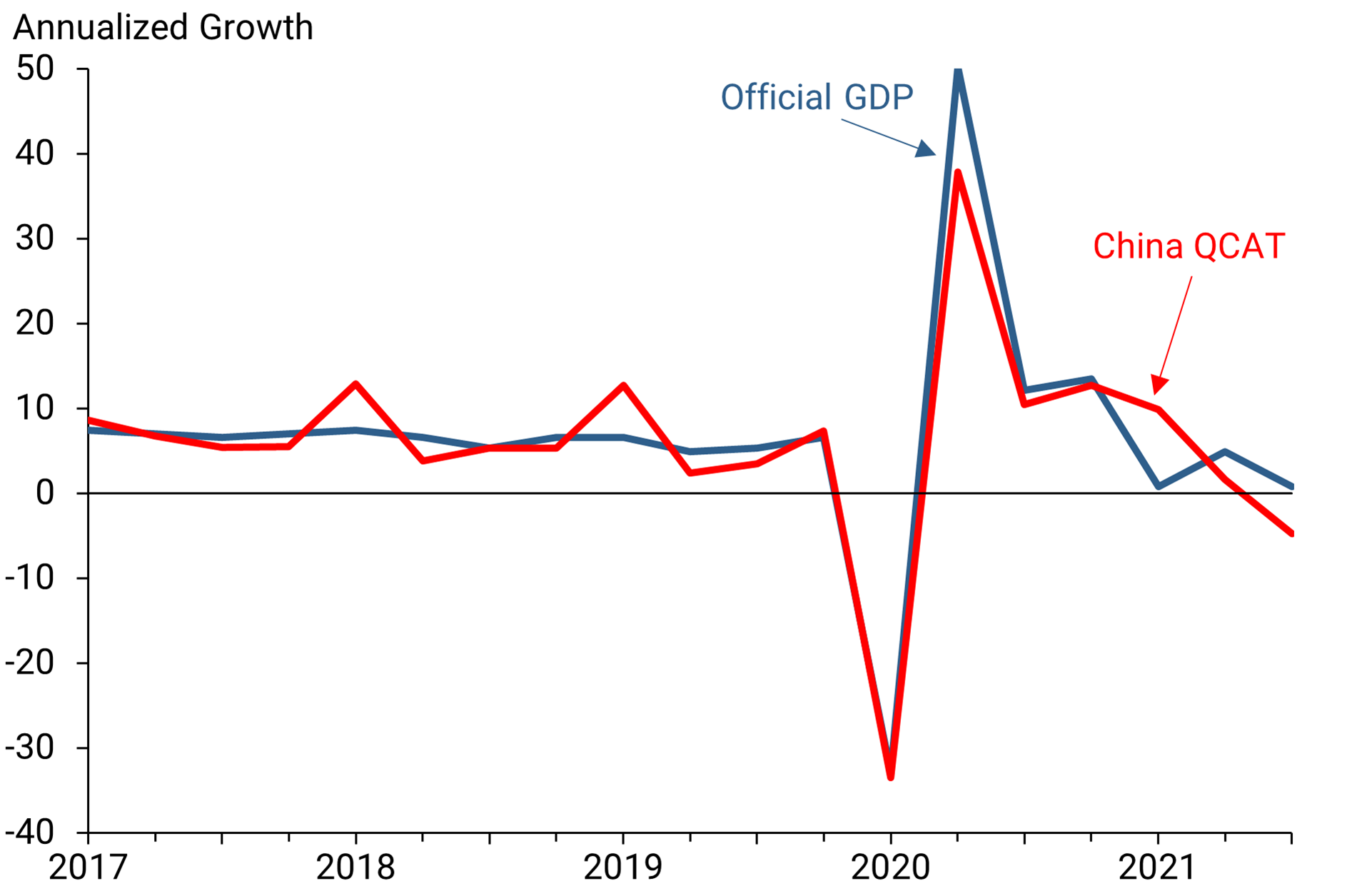

Our result is shown in the figure above. Before the pandemic, GDP was smoother than QCAT, which is consistent with the “over-smoothing” of GDP data published since 2013 (see Fernald et al., 2020). But in 2020, during the most turbulent period of the pandemic, QCAT’s quarterly results are similar to official GDP growth data.

However, we start to see significant differences in 2021. In the first quarter of this year, QCAT’s corresponding GDP annual growth rate was close to 10%, which was much higher than the tepid official annualized growth rate of 0.8%. But QCAT in the second quarter was much lower, with an annualized rate of 1.6%, compared to the official figure of 4.8%. Recently, in the third quarter, QCAT was sharply negative, at -5%-this is the second time since 2000 (when our data began) that, apart from the pandemic, China’s GDP growth has been negative ( The other is -4% increase during the Great Recession in the fourth quarter of 2008). Although the official data for the third quarter was weak, it was still positive, albeit below 1%.

Among the various components of QCAT, the growth of freight and retail growth in this quarter was particularly low, and the corresponding GDP growth was -6.1% and -5.9%, respectively. There are also some bright spots, such as investment in fixed assets, which entered at a rate of 1.9% higher than the trend. However, the latest data in October and November show that there has been a net decline in fixed asset investment in the past few months.

in conclusion

Before the pandemic, China’s CAT index, a non-GDP indicator, indicated that the published GDP was “too stable”. Nonetheless, during the worst period of the 2020 pandemic, our quarterly QCAT closely tracks quarterly GDP.

However, in the second and third quarters of 2021, there is a significant gap: the non-GDP indicators captured by QCAT seem to be more worrying than the (already weak) GDP data. In fact, QCAT shows that China’s economy is actually shrinking.These findings are related to Qin (2021)He also found evidence that, using typical seasonal adjustment methods, other published GDP data in China imply negative growth in the third quarter. In view of this, China recently announced measures to provide additional monetary stimulus measures by lowering the legal deposit reserve ratio, even if other central banks in the world are adopting austerity policies, it may not be surprising.

John G. Fernald is a senior research consultant in the Economic Research Department of the Federal Reserve Bank of San Francisco and a professor of economics at the European School of Business Administration.

Jack Mueller is a research assistant in the Economic Research Department of the Federal Reserve Bank of San Francisco.

Mark M. Spiegel is a senior policy advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco.

refer to

The brave Scott (2008). “Economic Trends and the Chicago Fed National Activity Index.” Chicago Fed Letter No. 250, May.

Chen, Wei, Xilu Chen, Chang-Tai Hsieh, and Zheng Song, (2019), “Forensic Examination of Chinese National Accounts, NBER Working Paper No. 25754, April.

Chinn, Menzie, 2021. “The extent and impact of China’s economic slowdown.” Econbrowser, October 25, 2021. http://econbrowser.com/archives/2021/10/the-extent-and-implications-of-the-China-Slowdown.

Fernald, John G., Eric Hsu, and Mark M. Spiegel, (2021), “Is China Fabricating Its GDP Data? Evidence from Data from Trading Partners,” International Journal of Monetary and Finance, 114, June, 102406. [ungated working paper version]

Nakamura, Emi, Jon Steinsson, and Miao Liu, (2016), “Are China’s growth and inflation too stable?: Evidence from the Engel Curve”, American Economic Journal: Macroeconomics. 8(3): 113-144.

Pinovsky, Maxim, and Xavier Sala-i-Martin (2016). “Lights, cameras…income! Light up the national accounts-household survey debate.” The Quarterly Journal of Economics, 131(2): 579-631, May.

Stock, James H. and Mark W. Watson, (2016), “Dynamic factor models, factor-enhanced vector autoregressive, and structural vector autoregressive in macroeconomics.” Handbook of Macroeconomics, Volume 2A, John B. Edited by Taylor and Harald Uhlig. Amsterdam: North Holland Province.

WikiLeaks (2007). http://wikileaks.org/cable/2007/03/07BEIJING1760.html.

{kind=link}

{kind=link}