Today, we are pleased to introduce to you by Laurent Ferrara (Professor of Economics and Board Member, Skema Business School international association of forecasters).

On Friday, October 21st, we organized an international meeting with Catherine Dodds at the Paris School of Economics (PSE) Macroeconomic Nowcasting Workshopwith the support of PSE Chair “Econometric Measurement”. In times of global uncertainty, it is critical to understand where we are now before trying to predict where the future is headed.Macroeconomic nowcasting is based on Giannione et al. (2008) The idea of using all currently available information in the best possible way to assess the state of the economy in the current quarter is well ahead of the official data generally released by statistical offices around the world, but with a lag time.

Most of the papers presented at this workshop focused on recently developed methods for nowcasting important macro-variables by using standard or surrogate high-frequency variables. Alternative high-frequency variables are data that can be collected through various channels (website, satellite, social network, tensors…). They are usually fairly large databases, available every day, unstructured and have a weak signal-to-noise ratio. Therefore, statistical/econometric techniques must be implemented to filter out the data and extract readable signals.The recent Covid crisis has highlighted the need for high-frequency tools capable of tracking real-time economic activity (see, for example, Lewis et al., 2020, in New York Fed closely monitor U.S. economic activity on a weekly basis).

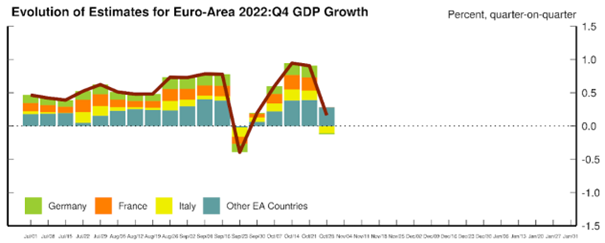

Modugno (Federal Reserve) joined D. Cascaldi Garcia (Federal Reserve), T. Ferreira (Federal Reserve) and D. Giannone (Washington and Amazon University) to present a new tool for tracking economic activity by Estimated dynamic factor models for the major euro area countries (Germany, France and Italy) to assess the euro area. The main idea is to consider the lead and lag between countries’ business cycles to improve nowcasting capabilities. Against this backdrop, opinion polls have proven to be very useful.Eurozone GDP weekly updates are available on the website in real time euronowcast.comThe latest GDP estimate for the fourth quarter of 2022, calculated on 28 October, was 0.2% (see Figure 1), indicating a sharp slowdown in economic activity in the euro area, consistent with extremely high inflationary pressures putting growth at risk.

figure 1: Eurozone Q4 2022 GDP growth (qoq) is approaching forecast. Source: euronowcast.com

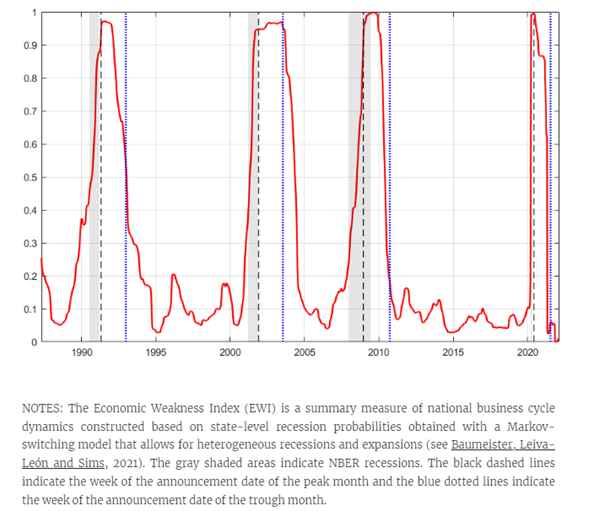

Danilo Leiva-Leon (Banco de España), along with C. Baumeister (Univ. Notre Dame) and E. Sims (Univ. Notre Dame), has built a new tool that tracks the state of the U.S. economy on a weekly basis. They managed to collect public databases of state-level economic indicators, including labor markets, mobility, actual activity, expectations, financial conditions and households. Estimates from the state-space model for each state lead to dashboards of economic conditions for each state at different frequencies.All estimation results can be found in website Promoted by the author. This piece of information is useful for economists interested in tracking U.S. economic activity at the state level. Also note that they calculated an economic weakness index that summarizes the number of states estimated to be in recession at each point in time (see Figure 2).

figure 2: US Economic Weakness Index

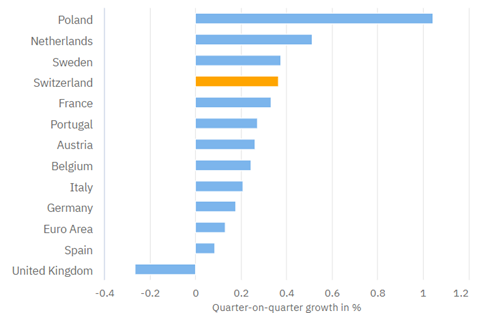

Heiner Mikosch, along with P. Kronenberg and S. Neuwirth (both ETH Zürich KOF), created a tool to track economic activity in many European countries using alternative datasets and various econometric models.This KOF Nowcasting Laboratory All available information for all countries is collected in real time. The model is updated daily as new data points become available. Interestingly, all nowcast estimates from all the various models are provided to users in a transparent manner, allowing each user to focus on their favorite model. The latest nowcast results for GDP growth in the fourth quarter of 2022 are shown in Figure 3 below.

image 3: Current GDP growth forecast for the fourth quarter of 2022.Source: KOF, Nowcasting Laboratory

The U.S. monthly retail trade index is one of the most closely watched economic indicators for market participants and economists because it reflects household consumption, the most important component of U.S. GDP growth. Scott Brave (Morning Consult) of the Chicago Fed and colleagues developed a tool to track the index on a weekly basis: Chicago Fed Advanced Retail Trade Summary (CARTS)The method relies on a mixed-frequency dynamic factor model that combines official data and high-frequency data from private companies reflecting credit and debit card transactions, retail foot traffic, gasoline consumption, or consumer sentiment. Unfortunately, in April 2022, the Chicago Fed temporarily suspended the release of the CARTS index due to changes in private data providers. The staff is currently working on a new version that will be released soon.

Two other technical papers were presented during this workshop. Gabriel Perez Quiros (Banco de España), in conjunction with S. Delle Chiaie (ECB), questioned the use of models containing only high-frequency surrogate data, which have weak signal-to-noise and often do have small sample sizes, leading to complex Estimation procedure. Using simulation exercises, they show that only high-frequency surrogate data leads to poor nowcast performance, and a good strategy for practitioners is to combine high-frequency surrogate data (i.e. daily or weekly) with low-frequency official data (i.e. monthly or Each quarter). Ivan Petrella (Warwick Business School), in association with T. Drechsel (University of Maryland) and J. Antolin Diaz (London Business School), proposes a new mixed frequency dynamic factor model for nowcasting that incorporates various important data features such as long-term time-varying GDP growth, heterogeneous dynamics among variables, and stochastic volatility. The latter feature has proven useful for explaining large shocks in economic time series, as observed during Covid-19. Real-time estimates from the model show that it can effectively track U.S. economic activity, including in the most recent period. In this regard, the integration of high-frequency data into models, in addition to more standard monthly and quarterly macro indicators, has proven to be very useful.

This article is by Laurent Ferrara.

{kind=link}

{kind=link}