Today we are pleased to introduce to you from Jamel Saadawi (University of Strasbourg).

Business is the antidote to the most destructive prejudices…Business will flourish wherever we find agreeable manners; Wherever we can find pleasant manners, commerce will flourish; Wherever we can find pleasant manners, commerce will flourish; ;As long as we can find pleasant manners, business will flourish there. Wherever there is trade, we meet in a friendly manner.

When two countries come into contact with each other, they either fight or trade. If they fight, both sides lose; if they trade, both sides gain.

Peace is a natural effect of trade. Two countries dealing with each other became dependent on each other…their alliance was based on their common needs.

Montesquieu, The Spirit of the Laws, 1748

From these few sentences, it is not difficult to see that the French philosopher Montesquieu (Charles Louis de Secondat, whose real name was Charles Louis de Secondat, born in 1689 and died in 1755) had great views on business and trade. There is a positive view on the impact on political relations between countries. Maybe that was true for his time.Related to this question, Menzie Chinn recently wrote here Perhaps increased trade is not always a good predictor of peaceful relations. Montesquieu may have been wrong.

An interesting question is to examine the case of China, whose emergence was not fully understood in the early 1990s (cf. here), hoping that the business community will fully realize the huge consequences of China’s take-off.After China joined the WTO December 2001In recent years, China has played an increasingly important role in world trade. This trend continued until the global financial crisis (GFC). Has China's expansion of trade over the past 60 years led to more peaceful relations with its trading partners?

Antonio Afonso, Valerie MignonI investigated this issue in a recent article work documents. To answer this question with some empirical evidence rather than relying solely on intuition, we need three elements, namely (1) a variable measuring trade linkages, (2) a variable measuring bilateral political tensions, and (3) a statistical test that allows for random Causal relationships over time.For trade linkages, we use current account balances (including income balances) and bilateral exchange rates with the U.S. dollar (the U.S. dollar remains dominant in trade; see here).For bilateral political tensions, we use the Political Relations Index (PRI) established and maintained by Yan Xuetong and his team at Tsinghua University (see here).For time-varying non-causal tests, we rely on Shi et al. (2020). We will focus on China's important trading partners, namely the United States, the United Kingdom, and Germany. We also focus on three important latency partners: India, Japan and South Korea.

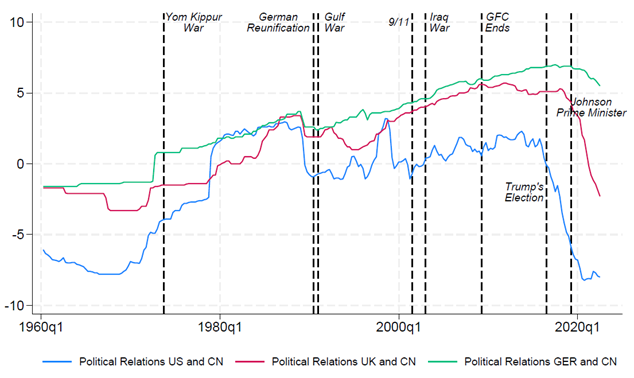

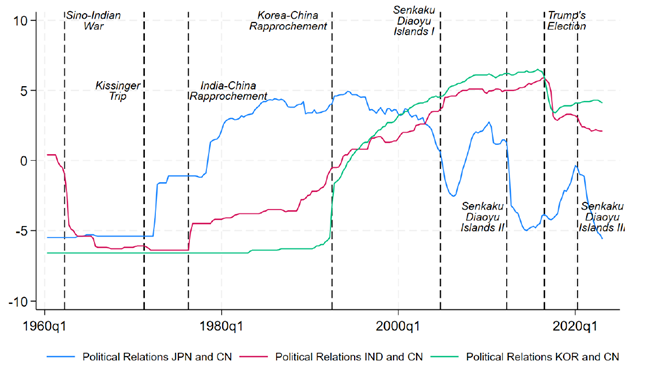

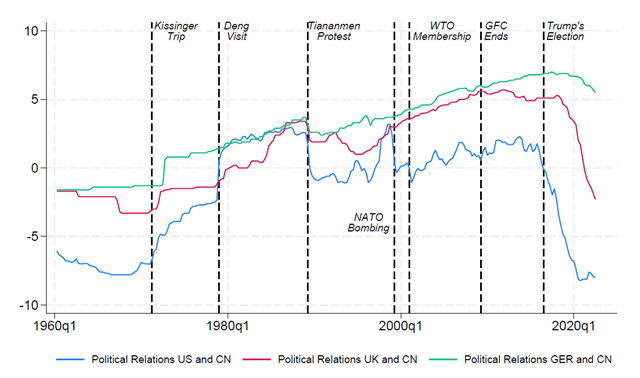

At this point, one might wonder about the quality of the PRI in measuring bilateral political tensions. In Figures 1 to 3 below, you will see the fluctuations surrounding major events reappearing with regularity.

figure 1: Bilateral Political Relations Index (PRI): Highlighting events between China and the United States

figure 2: Bilateral Political Relations Index (PRI): Focus on China-EU events

image 3: Bilateral Political Relations Index (PRI): Highlighting events in Asia and China

If you are sufficiently confident that these indices are reliable, we can now turn to tests of time-varying non-causality between trade linkages and political tensions to answer our questions.In this article we use an alternative political measure, the ideal point distance to China in UN General Assembly voting (see here), as a robustness check.For bilateral exchange rates, we also add lagged enhanced VAR, i.e. Ground Penetrating Radar Index Caladara and Iacoviello and the VIX, as these two variables may affect bilateral exchange rates.

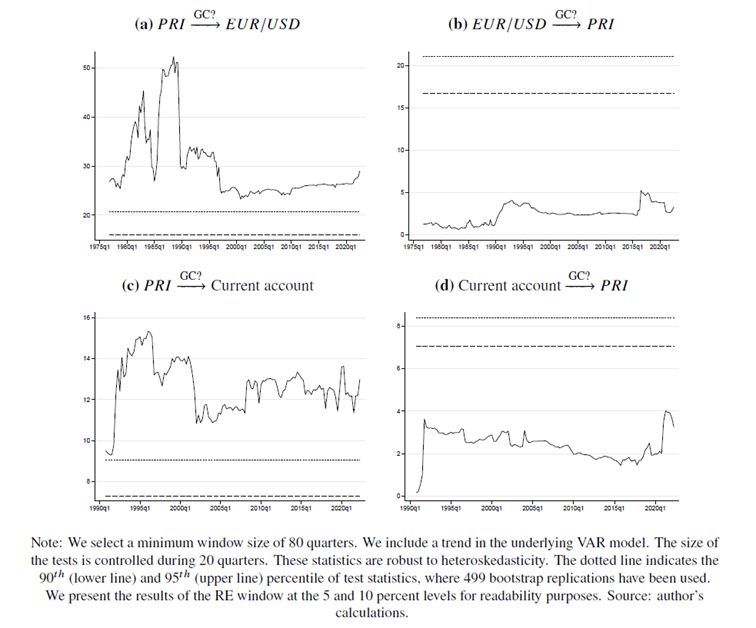

The German example is particularly interesting. As shown in Figure 4, there is a unidirectional causality from the PRI to the exchange rate and the current account over most of the time period considered. From a global perspective, Sino-German political relations continued to improve, accompanied by depreciation of the renminbi and an increase in current account surplus. However, at the end of the period, tensions began to emerge and the renminbi appreciated. After China joined the WTO, Sino-German relations were at the core of the global value chain. This special connection was strengthened during the Eastern European expansion in 2004, when Germany began to become the industrial core of the new EU and the center of gravity shifted to the east. Germany and China have become the two main players in trade flows (Miranda-Agrippino et al., 2020).

Overall, our findings suggest that Montesquieu's “double commerce” perspective does not always apply to the United States and Britain, let alone Germany. He argued that causality should extend from trade to political relations, as trading partnerships should produce more peaceful relations between individuals and nations. We find that both the “doux commerce” and “trade follow the flag” views are supported by empirical evidence from different periods in the United States and the United Kingdom, illustrating the relevance of norms that change over time. The most striking result is that for Germany and China, “trade always follows the flag”: we reject the null hypothesis of non-causality from political relations to macroeconomic variables, and the null hypothesis of non-causality from political relations to macroeconomic variables The relationship does not hold. This shows that good political relations are a prerequisite for the expansion of Sino-German trade.

Figure 4: Time-varying causality between China and Germany

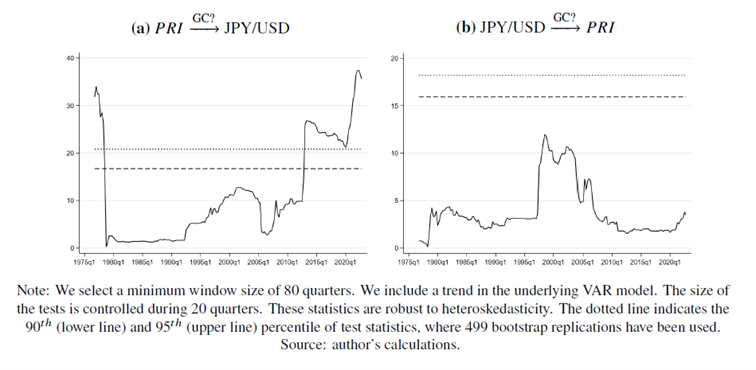

As far as Asian partners are concerned, although there is no causal relationship between PRI and exchange rates in most cases, it can be significant at certain times when certain events occur. Until the early 2000s, Sino-Japanese relations had been on an upward trend globally (Figure 5), and heated up significantly after Shinzo Abe and later Yasuo Fukuda became prime ministers of Japan in September 2006. The issue of territorial ownership of the Koh Zhu Islands/Diaoyu Islands has aggravated tensions. The deterioration in Sino-Japanese relations affected the yen exchange rate, as shown by the significant causal relationship observed in Figure 5 . PRI's causal exchange rates are mostly unimportant. The significant causal relationship observed in the Indian case in the mid-1990s can be explained by border issues and Indian nuclear testing, which were clearly a consequence of the tensions caused by the severing of diplomatic ties between Taipei and Seoul in 1983. , in terms of the PRI exchange rate, this was particularly important for India in the 1990s, when the rupee depreciated sharply due to current account deficits and loss of investor confidence.

Figure 5: Time-varying causality between China and Japan

The author of this article is Jamel Saadawi.

{kind=link}

{kind=link}