Today we publish a guest article written by: Danilo Leyva-Leon (European Central Bank), Hervé Lebihan (France Bank) and Matthias Paes (Bank of Spain). The views expressed in this article are those of the author and do not necessarily represent the views of the Bank of France, the Bank of Spain, the European Central Bank or the Eurosystem.

inflationary regime shift

Model-based underlying inflation indicators are often based on the assumption of linearity in price dynamics. In particular, unobservable component models often assume that the dynamics of underlying inflation follow a random walk, so that underlying inflation can only exhibit smooth changes over time. However, the recent sudden surge in energy and raw material prices, and the subsequent rapid transmission to other items in the consumption basket, has challenged this assumption. Furthermore, several works emphasize the importance of considering nonlinearity and state dependence when modeling inflation (e.g., Ascari and Haber (2022), Klenow and Kryvtsov (2008), Cavallo, Lippi, and Miyahara (2023)).

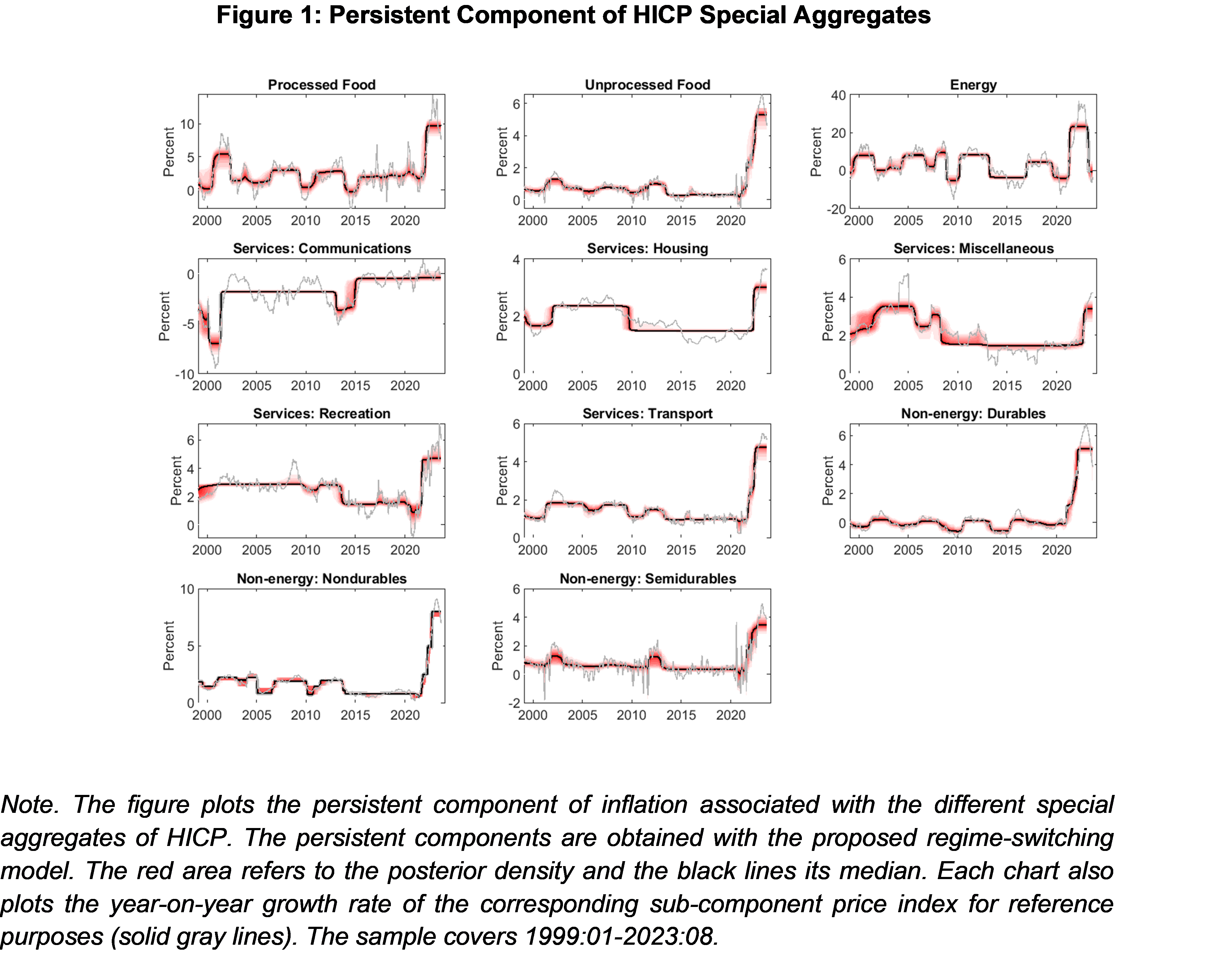

In this context, Le Bion, Leyva-León and Paes (2023) A multi-regime transition framework is relied upon to estimate the persistence component of inflation at the disaggregated level.[1] Unlike previous related approaches in the literature, each sustained component of interest is assumed to exhibit unique magnitudes of transitions between high- and low-inflationary regimes.[2] Figure 1 shows the estimated persistence component of euro area inflation at the category level, showing considerable heterogeneity over time and across categories. The estimates show that the proposed framework is flexible enough to accommodate various inflation dynamics present in different types of goods and services.

A non-linear measure of underlying inflation

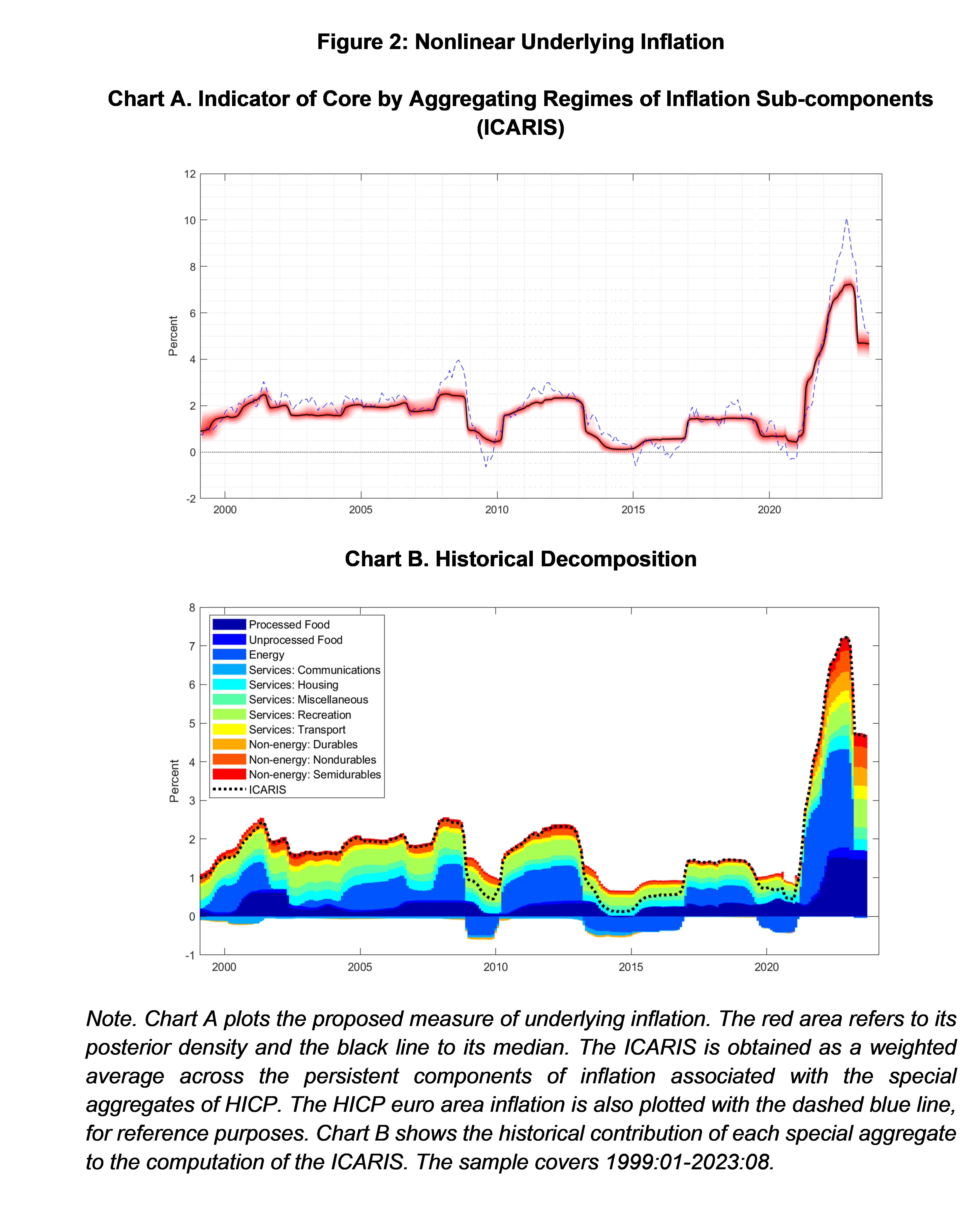

Consistent with underlying inflation being defined as the persistent component of overall inflation, by using weights to construct the HICP, we summarize the persistence components associated with each sub-aggregation into a single measure that constitutes our proposed underlying inflation. A nonlinear measure of expansion. The resulting indicator is labeled “ICARIS”, which stands for Core Indicator of the Inflation Subcomponent Aggregation Mechanism. Panel A in Figure 2 plots our measure of core inflation over the period 1999:01-2023:08. ICARIS is characterized by strong persistence. This is an attractive feature because this underlying inflation measure is not subject to the erratic movements often seen in idiosyncratic aggregate inflation rates. Despite its persistence, ICARIS was able to adapt quickly to the new inflationary environment. For example, this was the case in 2013 when the Eurozone entered a period of sustained low inflation.

Looking at the post-pandemic period, ICARIS shows that euro area underlying inflation experienced a sudden and unprecedented jump starting in early 2021, peaking in December 2022, and then declining rapidly until March 2023. Thereafter, underlying inflation remained almost unchanged until the end of the sample in August 2023, showing a value of nearly 4.6%. This suggests that underlying inflation has peaked, as a check of other indicators confirms, although it remains well above the ECB’s target level.[3] Panel B in Figure 2 plots the historical contribution of each HICP subcomponent to ICARIS, showing the prominent role of energy prices in driving underlying inflation from early 2021 to March 2023. It also suggests that while energy prices currently have a negative impact on underlying inflation, other sub-components of the HICP (particularly food inflation) face persistently higher inflationary pressures, as shown at the end of the sample in Figure 1.

risk assessment

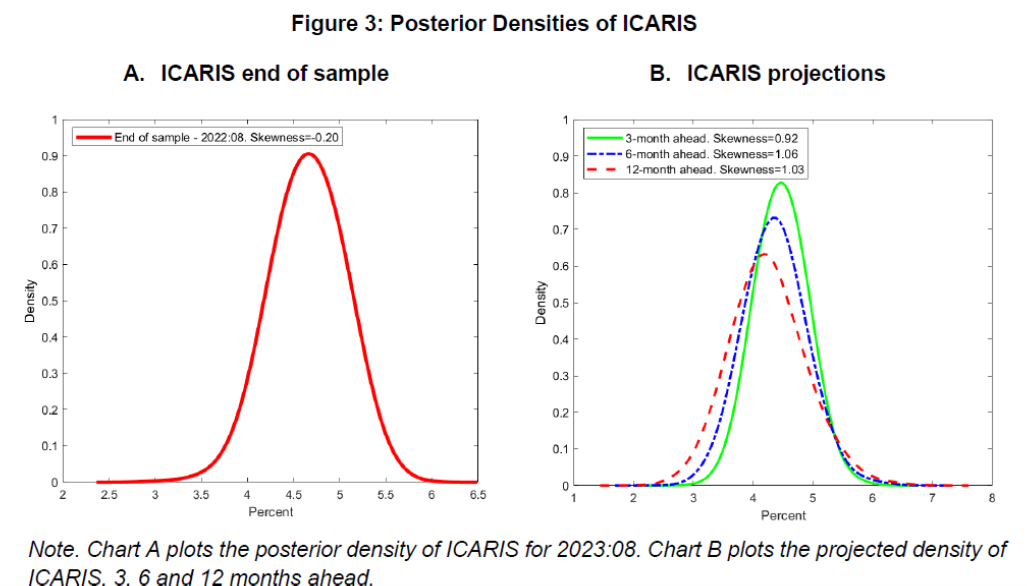

ICARIS can also be used to measure asymmetric tail risks associated with potential future inflation. This asymmetry is caused by induced nonlinearities in our model. This feature may be highly relevant for policy in forecasting activities, or from a “risk management” perspective, especially in periods of high uncertainty. Panel A in Figure 3 plots the posterior density of ICARIS in August 2023 with a skewness of -0.20, indicating modest downside “risk” associated with current underlying inflation. In contrast, Panel B of Figure 3 shows projected ICARIS densities for the next 3, 6, and 12 months, starting with September 2023. The density series shows that the expected path of underlying inflation in the coming months is associated with a slight downward trend, but risks are pointed significantly to the upside. This information can be inferred from the leftward shift of the density on the projected horizon and its positively related skewness.[4]

refer to

Ascari, G., and T. Haber (2022). “Nonlinear, state-dependent price and monetary policy transmission mechanisms”, Economic Journal, 132(641), 37-57.

Cavallo, A, Lippi F and Miyahara F. (2023) “Big Shocks Propagate Fast, NBER Working Paper 31659”

P. Klenow and O. Kryvtsov (2008). “Country-Dependent or Time-Dependent Pricing: Does it Matter for Recent U.S. Inflation?” Quarterly Journal of Economics, 123(3), 863-904.

Le Bihan, H., D. Leiva-León, and M. Pacce (2023). “Potential inflation and asymmetric risks”, Bank of Spain Working Paper N.2319.

Leiva-León, D., G. Pérez-Quirós, and E. Rots (2023). “Immediate Weakness in the Global Economy,” Journal of Applied Econometrics, forthcoming.

[1] Monthly HICP inflation data are broken down by “product type” into 11 specific categories related to certain “special aggregate” indices or sub-components of inflation published by EUROSTAT and commonly used by the European Central Bank for analytical purposes.

[2] The proposed methodology is based on the work of Leiva-León, Pérez-Quirós and Rots (2023) and also allows to understand transitions between inflationary regimes using information on real activity represented by the Eurozone Industrial Production Index.

[3] Inflation excluding food and energy, or core inflation, reached 5.3% in August.

[4] As a general rule of thumb, if the skewness of a given distribution is between -0.5 and 0.5, it can be considered approximately symmetric.

Conversely, if the skewness is above (below) 0.5 (-0.5), the distribution is considered asymmetric.

The author of this article is Danilo Leyva-Leon, Hervé Lebihan and Matthias Paes.

{kind=link}

{kind=link}