I just took the time to write about this Trump policy proposal: “Trump trade adviser plots dollar devaluation” . I'm confused about how the Trump think tank will effectively force the dollar to weaken: sterilize intervention, lower U.S. interest rates, or force foreign countries to re-peg their currencies to stronger exchange rates. They all seem to have problems.

sterilization intervention: There is not much evidence that this approach is effective on a long-term basis for countries with open capital markets (see Popper, 2022 for investigation).

US interest rates fall: If the U.S. can lower interest rates while forcing other countries to raise them, then (without potentially causing any turmoil in financial markets) the dollar will lose value. Furthermore, if lowering U.S. interest rates can convince financial market participants that inflation will accelerate, then most standard exchange rate monetary models would predict a depreciation of the U.S. dollar in the short term.

My estimates for the interim model for 2005-2023 are:

r = -5.61 + 2(yy*) + 9.6I – 9.7i* – 0.81p+ 1.51p* + 0.003VIX

Adjust-R2 = 0.88, SER = 0.031, DW = 0.60, N = 76.The coefficient is bold Significance at 10% MSL is indicated using HAC robust standard errors.

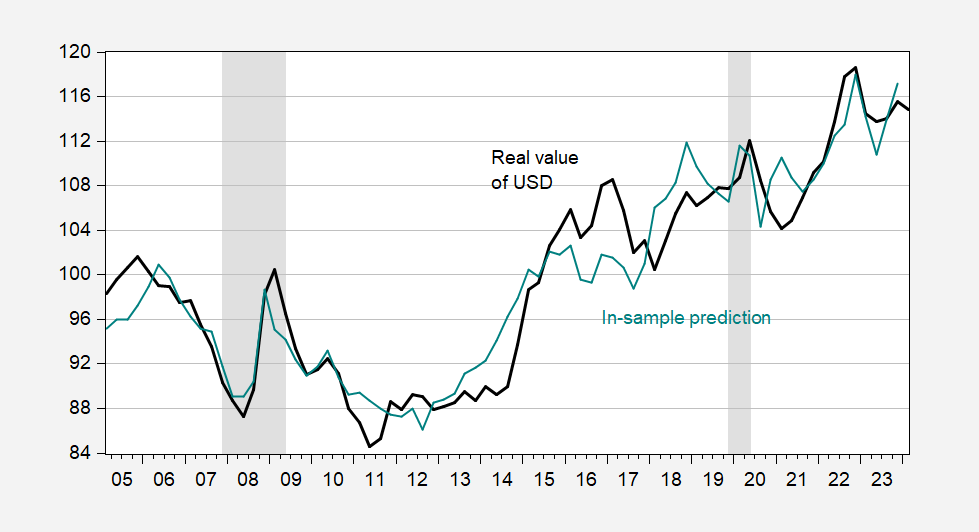

Where r is the log real trade-weighted dollar, y is the gross domestic product, I is the 10-year rate of return, PI is the year-on-year CPI inflation rate, * indicates other developed economies. The fitting is shown in Figure 1:

figure 1: Actual trade-weighted value of USD (bold black), in-sample forecast (cyan). NBER-defined recession peak-to-trough dates appear gray. Source: Federal Reserve through FRED, NBER, and author's calculations.

If this set of correlations persists into the future, the 10-year yield would fall by one percentage point Compared to foreign countries The dollar's real value will decrease by nearly 10%. Is this possible in practice? It's hard to say; after all, long-term rates are correlated, and long-term rates in other developed economies tend to move in tandem.

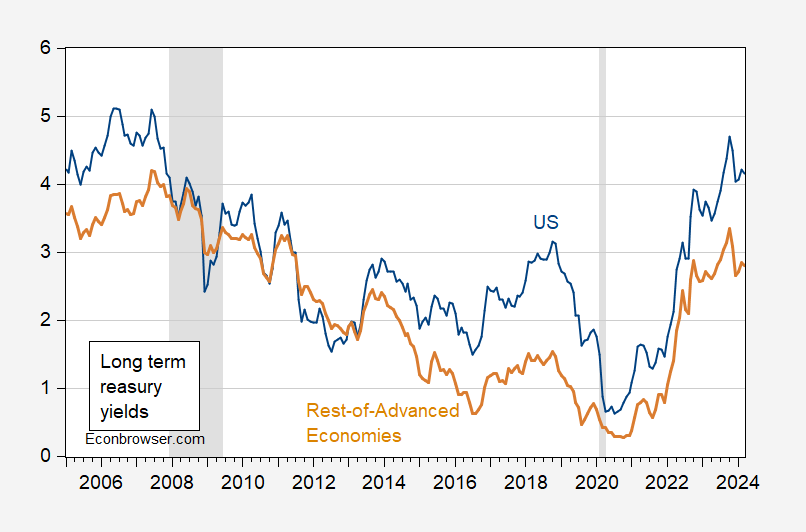

figure 2: U.S. 10-year Treasury bond yields (blue), long-term (5-10 year) government bond yields in other developed economies (tan), both in %. NBER-defined recession peak-to-trough dates are in gray. Source: Treasury via FRED, Federal Reserve Bank of DallasDGEIand the National Bureau of Economic Research.

Over the sample period, a one-percentage-point change in U.S. Treasury yields was associated with a roughly 0.6-percentage-point change in other developed economy yields.

Of course, if the US lowers interest rates, then US GDP may grow faster than otherwise, slightly offsetting the (already weakened) impact of interest rates. If the U.S. has to use some tough tactics to gain “cooperation” from other countries, the VIX could rise (as has often happened under Trump, especially during trade wars). Of course, in a market economy, the U.S. Treasury itself cannot control Treasury bond yields.Therefore, Fed compliance is necessary (which is probably why Trump’s think tank Thinking about how to make the Fed’s decision-making process more malleable).

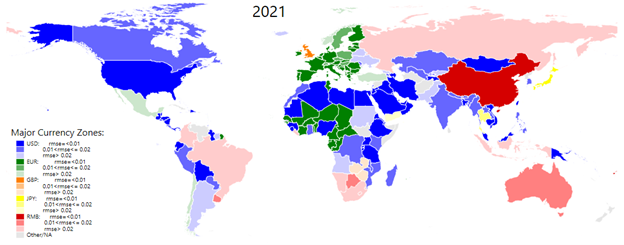

force other countries to appreciate: The nominal value of the dollar is a function of national policies pegged to the dollar. Ito and Kawai defined currency areas as areas pegged to their respective currencies. As of 2021:

image 3: The evolution of the major currency areas. Source: Compiled by the authors based on their estimates. source: This (2024).

Of those countries identified as part of the dollar area, not all are pegged or quasi-pegged to the dollar. But if it does so, the United States could induce the yuan to appreciate. How effective is it? Adler, Lisack and Mano (Emerging Markets Review, 2022) The study found that for every 1 percentage point reduction in GDP caused by foreign exchange intervention, the bilateral real exchange rate will appreciate by 1.4-1.7 percentage points.have Some question whether China will resume peg to US dollar in 2024, but we can examine the feasibility of a significant dollar appreciation by examining the extent of intervention now underway. The latest FX report released by the U.S. Treasury Department in November 2023 provides some statistics.

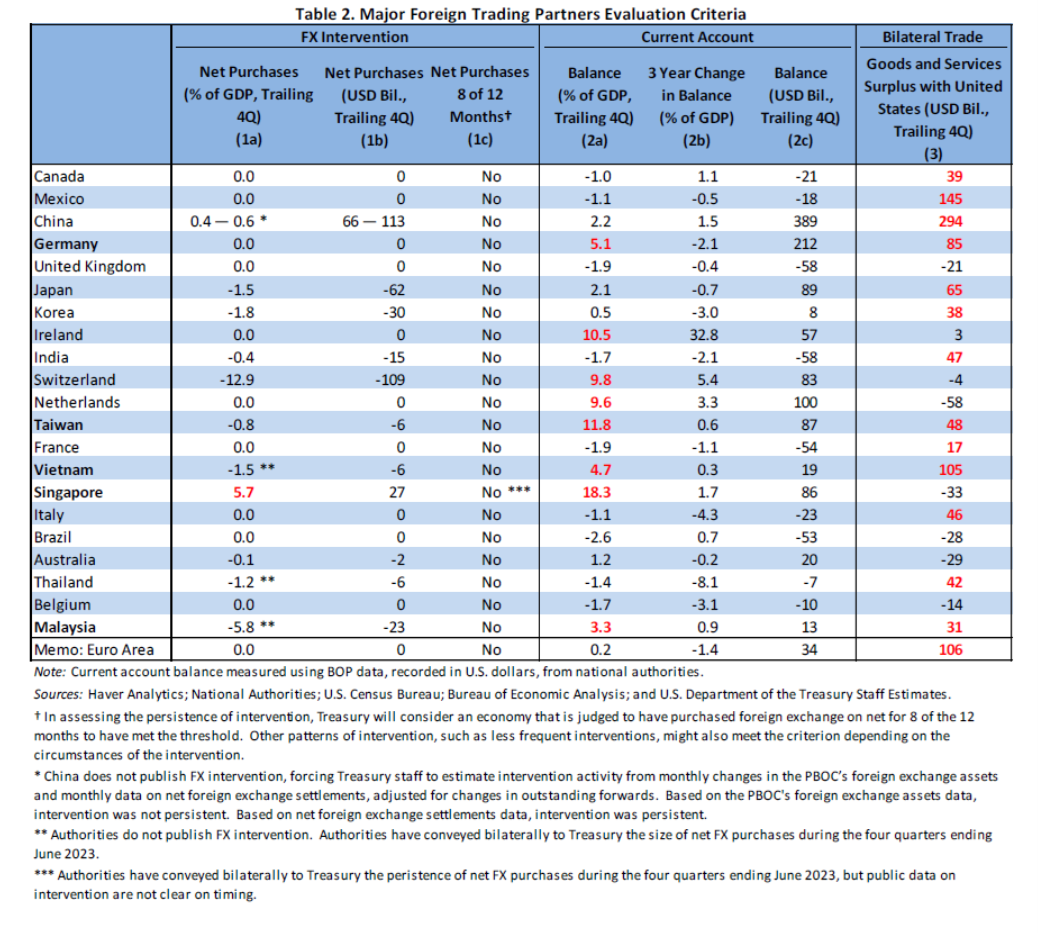

source: U.S. Department of the Treasury (November 2023).

Singapore is intervening heavily (as a share of GDP) but has a weight of only 1.9% in trade-weighted USD (broad Fed). China has a larger weight at 13.4% [1]. If China intervenes to reduce GDP by 1 percentage point (the Ministry of Finance estimates 0.4-0.6 percentage points), then the yuan will appreciate by 1.4-1.7%.What directly affects trade weighted dollar Then it will be 0.23 ppts to 0.28 ppts(!). If some countries peg their currencies to the yuan, they may be slightly more affected. Ultimately, however, it seems like a lot of work to make a small change in the value of a dollar.

More assessment of the desirability of this policy initiative Lamper (Wapo)also Holland (national review).

{kind=link}

{kind=link}