It’s Wednesday and I have a few observations about a few things today. I have written before that, far from causing deflation, rising interest rates in many countries have significantly increased inflationary pressures. This effect occurs in two ways: first, through increased creditor wealth combined with a large number of fixed-rate mortgages providing the equivalent of a fiscal stimulus, and second, through overdrafts and the direct impact on business costs. landlord. The former only passes on the increase in unit costs to consumers, while the latter increases rents and affects the consumer price index. But I’ve also been tracking another negative outcome of rising interest rates – the impact on investment in renewable energy. Here are some relevant notes, followed by some renewable energy-themed music.

RBA thinks rate hikes will slow housing market – data says otherwise

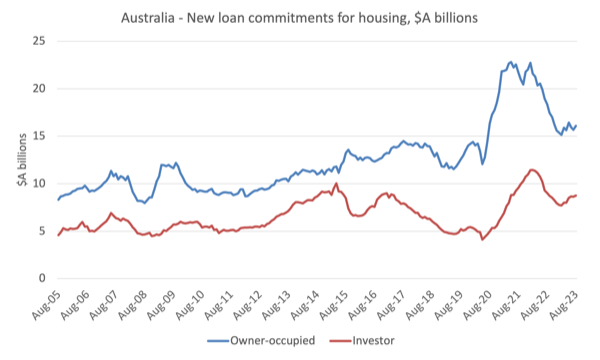

Yesterday (October 3, 2023), the Australian Bureau of Statistics released the latest data— loan index – This tells us about new borrowings for “home, personal and business loans”.

Earlier this week (October 2, 2023), we learned that Australian house prices are now heading towards record highs after a slight decline.

Australian Broadcasting Commission (ABC) article – Australian house prices are on track to hit new highs, latest real estate data shows – A summary of the latest data is provided.

In September, “housing data showed house prices rose 0.8 per cent nationally in September, led by gains in Adelaide, Brisbane and Perth, where housing supply remains about 40 per cent below the five-year average.”

The ABS data released yesterday was consistent with the house price data.

Data shows that new loan commitments in August 2023:

1. Housing rose 2.2%.

2. Personal loans grew by 6.1%.

3. Commercial construction grew by 17.2%.

4. Business purchases of real estate increased by 10.8%.

These totals have declined during the past 12 months, but there has been a shift in new loan commitments since March 2023.

The chart below shows seasonally adjusted new loan commitments for homes (owner-occupied and investment properties) from 2005 to August 2023.

The remarkable boom during the pandemic was largely driven by low interest rates, with the RBA governor at the time saying the central bank would not raise interest rates until 2024.

He later denied the claim, but everyone heard it and borrowed money based on it.

Subsequently, the Reserve Bank of Australia began to raise interest rates in May 2022, and subsequently raised interest rates 12 times, raising the target interest rate by 400 basis points.

All this is said to be an attempt to dampen the dynamism of the housing market and reduce borrowing.

The chart shows that rising interest rates may have temporarily reduced home borrowing, but now new loan commitments are rising again.

So on the face of it, the RBA’s monetary policy changes are not having the impact they claim.

This will come as no surprise to anyone who understands the uncertainty created by these impacts.

The RBA likes to sound like it knows what it’s doing.

The fact remains that changes in interest rates trigger complex and contradictory forces, and the RBA has no idea what the ultimate impact will be.

That’s not to say rising rates won’t hurt certain groups in the economy — typically low-income borrowers with adjustable-rate mortgages who also carry large amounts of credit card debt because their incomes aren’t growing.

But from a macro level, the real estate market is heating up again.

Monetary policy changes undermine future sustainability

One of the benefits of the period of low interest rates that preceded the recent phase of rising rates was that it stimulated funding for investment in renewable energy.

The cost of capital is only one factor that affects investment, but it is clear from the data that when interest rates are low, the renewable energy industry expands faster than most initially expected.

Another major factor stimulating this expansion is the development of technologies that shift the competitiveness of energy towards renewable energy sources.

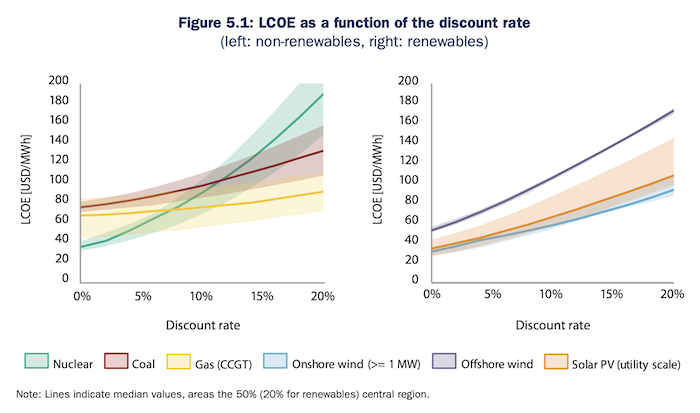

I read a report a few years ago – Estimated power generation costs – 2020 edition – Published by the International Energy Agency (IEA).

These reports are published every five years and:

It presents plant-level generation costs for baseload electricity generated by fossil fuel and nuclear power plants, as well as a range of renewable energy generation, including variable energy sources such as wind and solar.

The latest version found:

…The average power generation cost of low-carbon power generation technologies is falling and is increasingly lower than the cost of traditional fossil fuel power generation” – this is one of the reasons for the rapid shift in the power generation mix to renewable energy.

The graph (replicated in Figure 5.1) shows the sensitivity of different energy sources to changes in the “discount rate” or interest rate, and they point to “multiple aspects that influence the cost of LCOE, such as construction, refurbishment and decommissioning expenses”.

If you study the graphs on the left and right, you will see that natural gas technologies have been virtually unaffected by the rate increases we have observed over the past year or more, while renewable energy technologies have been significantly affected in terms of their “levelized costs” of electricity”.

The report states:

Within the group of flexible baseload plants (i.e. nuclear plants, coal-fired plants and natural gas combined-cycle gas turbines), the latter are least susceptible to discount rate changes. The average cost for the median case increases by approximately 40% compared to the 0% and 20% discount rate cases…Variable renewable energy technologies wind and solar exhibit relatively high upfront costs and low operating costs— Since no fuel costs are incurred, the latter only include operation, maintenance and refurbishment costs. These characteristics make them particularly susceptible to changes in discount rates.

But the IEA report was released in 2020.

So what now?

In April this year, Lazard Group, a long-established global financial services company, released its latest forecast: Cost of electricity – This confirms that “the cost… and availability of capital… are particularly important for renewable energy generation technologies”.

Between 2021 and 2023, wind’s LCOE (USD/MWh) has increased from $50 to $75, while solar has increased from $41 to $96.

Interestingly, Lazard’s analysis of sensitivity to rising interest rates, compared to the IEA’s sensitivity analysis (shown above), shows that while LCOE for solar and wind (onshore) will rise significantly as interest rates rise, Natural gas will remain higher than renewables at all rates.

Offshore wind is the most vulnerable of renewable energy sources when interest rates rise.

Also note that coal, natural gas peaking, and nuclear are no longer competitive at any rate (cost of capital), and despite many progressives’ claims of nuclear’s superiority, nuclear will clearly never be a realistic option.

Today EUobserver published an article on the same topic (2 October 2023) – Is the ECB undermining the European Green Deal?.

They asked questions like:

The Frankfurt-based bank’s management board, which grew by 4.5 percentage points in just over a year, has knowingly or unknowingly conducted what is essentially an experiment: Can the EU’s green transition succeed, even if funding is so expensive?

They note that higher interest rates make the transition “significantly more costly – which in turn could test the limits of what governments and businesses are willing to pay to go green.”

Importantly, however, and this is the point I made above, the ECB (or any central bank) doesn’t know exactly what will happen when they push interest rates higher:

It doesn’t help that the ECB’s modelers have predicted a wide range of real-world consequences of its policies, leaving even the most seasoned ECB observers skeptical that the bank has a clear understanding of what their actual impacts will be.

This is all guess work, and the difference between guess and guess in the real world is often huge.

The article reported that a Dutch consultancy “estimated the transition costs of eight major climate technologies, including solar, wind, geothermal and electric boilers” and found that “the cost of reducing emissions has increased by €17 billion to 2030.” , compared to 2021 prices with interest rates still below zero.”

Another question is:

…The models they typically use for energy and climate-related decisions ignore interest rate dynamics…

More needs to be done, but the long-term negative impact of unnecessary rate increases during this period will certainly be significant.

For example, the article reports:

… In 2022, there were no investments in offshore wind farms in Europe.

Interestingly, what follows is a discussion of what fiscal policy can do:

The government can provide developers with better deals or increase subsidies. But relying solely on the government may be a risky choice as rising debt costs have led to spending cuts. Higher costs could also exacerbate right-wing backlash against green legislation, which is already underway in Europe.

This is a scenario that the Europeans have created for themselves, and member states using a common currency will certainly be constrained in terms of fiscal policy because they use foreign currencies.

But for the rest of the world, fiscal policy is limited only by the actual resources available for productive use, with the caveat that if resources need to be transferred from one use to another, action other than spending is required. policy.

This includes tax reform – not to fund spending, but to free up needed resources so that they can be spent in the public sector.

I will be writing more soon about the choices the government faces in this regard.

Music – Mary the Wind Cries

Given today’s theme of renewable energy, I thought this great song would be appropriate.

The Wind Cries Mary – go through – Jimi Hendrix – is one of my favorite songs of all time.

It came out in 1967 and was reportedly recorded at the end of a 20-minute recording session.

Master level.

This is a live version released by the Jimi Hendrix family, recorded in Paris on October 9, 1967.

That’s enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}