reader john h. criticize me postal So, regarding real mortgage rates:

With interest rates changing rapidly this month, results could change overnight, making the date of the data crucial. I provided my inflation assumptions and my mortgage rate assumptions. These are not provided in the table above. And no actual data was provided.

Also, after-tax calculations depend heavily on assumed tax brackets. All information about tax brackets appears in the statement about “even the highest tax brackets”.

at this Spreadsheets, I included all the series used to build the three charts below. The layout of the spreadsheet is so simple I’m sure an idiot can understand it.

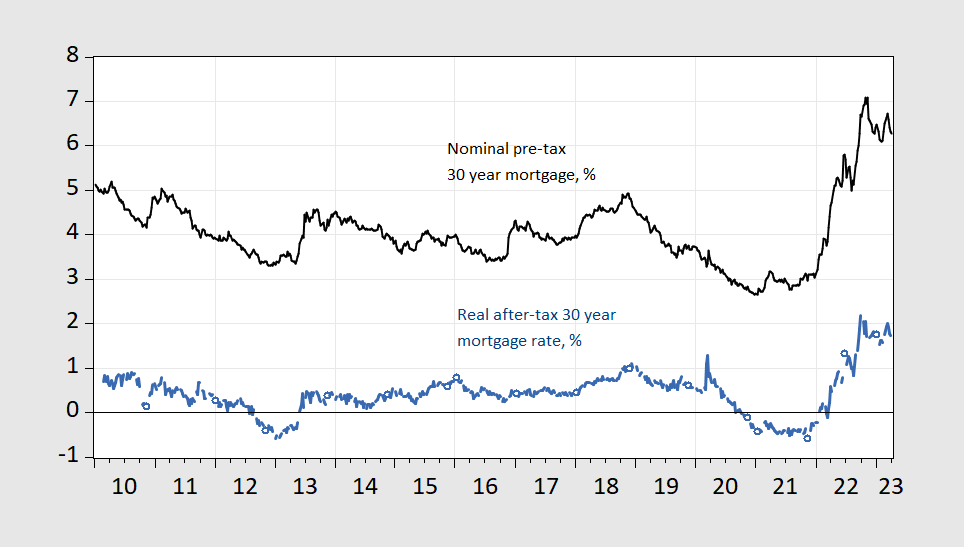

First, calculate the after-tax tax rate for the highest income bracket. If one is trying to show that all real interest rates are above zero, then one wants to use the highest marginal tax rate to minimize the after-tax rate. In Figure 1 below, I show the top marginal tax rate (black line, right scale) and the 30-year fixed tax rate (blue line, left scale). Applying the adjustment for the top tax rate produces the tan line below. If any other tax bracket is used, the after tax rate will be higher.

figure 1: 30-year fixed mortgage rate before taxes (blue, left scale) and after taxes (tan, left scale), both in percentages; top marginal tax rate (black, right scale, %). SOURCE: Fannie Mae via FRED MORTGAGE30US, Treasury Department via FRED, author’s calculations.

at this SpreadsheetsI included all the data needed to replicate all the series shown in the image below.

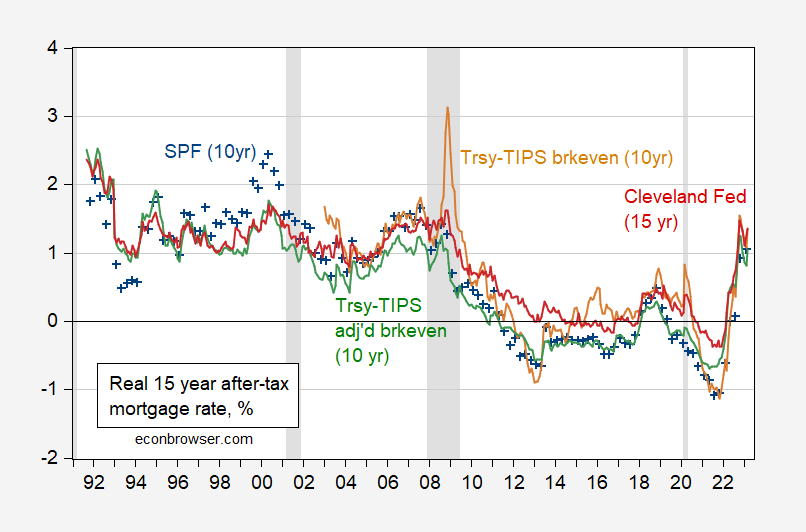

Now, consider the 15-year after-tax mortgage rate. I only have one measure of expected inflation in 15 years (the Cleveland indicator). I use the 10-year metrics of Treasury-TIPS breakeven, adjusted breakeven, and SPF 10-year median to represent 15 years. This gives the following plot.

figure 2: 15-Year After-Tax Mortgage Rate 10-Year Inflation Expected Median (Blue+) Adjusted by Professional Forecasters Survey, Adjusted by Treasury-TIPS 10-Year Breakeven (Tan), Treasury-TIPS 10-Year Breakeven Adjusted for risk, liquidity premium (green) and adjusted for Cleveland Fed’s 15-year inflation forecast (red). Sources: For mortgage rates, Fannie Mae via FRED series MORTGAGE15US; FRED’s Treasury and TIPS (GS5, FII5), the adjusted break-even kilowatt (Access 4/8), for SPF Federal Reserve Bank of PhiladelphiaForecast inflation for 15 years cleveland fedand National Bureau of Economic Research.

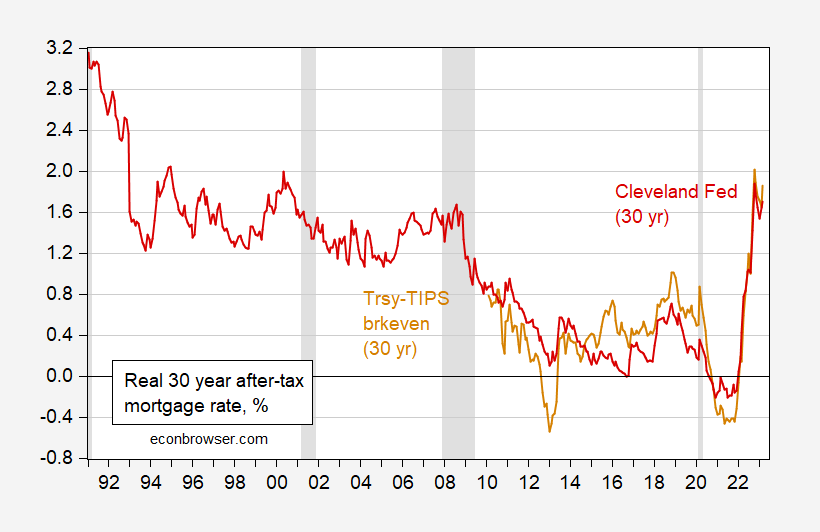

For the 30-year mortgage, we can use the 30-year break-even and 30-year Cleveland Fed forecasts for an exact match.

image 3: 30-year after-tax mortgage rates adjusted for Treasury-TIPS 30-year breakeven (tan) and adjusted for Cleveland Fed’s 30-year inflation forecast (red). Sources: For mortgage rates, Fannie Mae via FRED series MORTGAGE30US; FRED’s Treasury and TIPS (GS30, FII30), the adjusted break-even kilowatt (Access 4/8), Forecast Inflation for 30 Years cleveland fedand National Bureau of Economic Research.

In case the casual observer wasn’t clear, I’d note that real mortgage rates, even after assuming the highest marginal tax rate that produces the lowest nominal rate, are now above zero.

Reader JohnH asserts that it is appropriate to use inflation lagged by one year.I document CPI inflation with a one-year lag is not a good predictor of subsequent five-year inflation; the situation may be even worse for subsequent 15 or 30-year inflation.

Finally, the claim that rapid changes in interest rates lead to inappropriate monthly characteristics is not substantiated. In Figure 4, I show the weekly nominal pre-tax mortgage rate, and the weekly rate adjusted for inflation expectations. No violent fluctuations were shown.

Figure 4: Nominal 30-year fixed mortgage rate, weekly as of Thursday (black), and nominal yield adjusted for top tax, minus 30-year inflation breakeven (blue), both in %. Sources: Fannie Mae via FRED, Treasury Department via FRED, and author’s calculations.

So, I conclude: ex ante mortgage rates are currently positive.

{kind=link}

{kind=link}