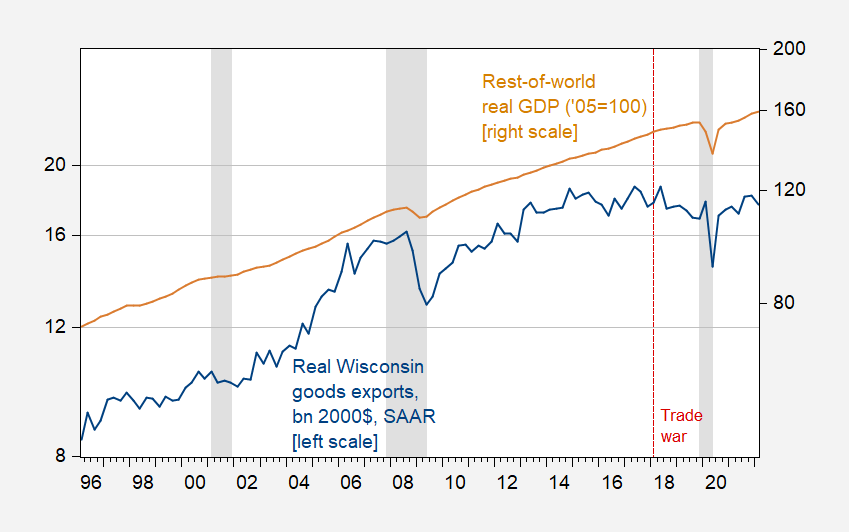

I’m covering the factors that determine Wisconsin exports. This is an interesting finding – since 2018, real merchandise exports have underperformed expectations based on the rest of the world’s GDP and the real value of the dollar.

This is the Wisconsin Merchandise Exports (from BEA) export price index of all commodities using the BLS, plotted in real terms with the rest of the world’s real trade-weighted GDP index.

figure 1: Wisconsin’s merchandise exports in billions of dollars in 2000, SAAR (blue, left logarithmic scale) and rest of the world real GDP, 2005 = 100 (brown, right logarithmic scale). The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA/Census, BLS all from FRED, Dallas Fed DGEI, NBER and author’s calculations.

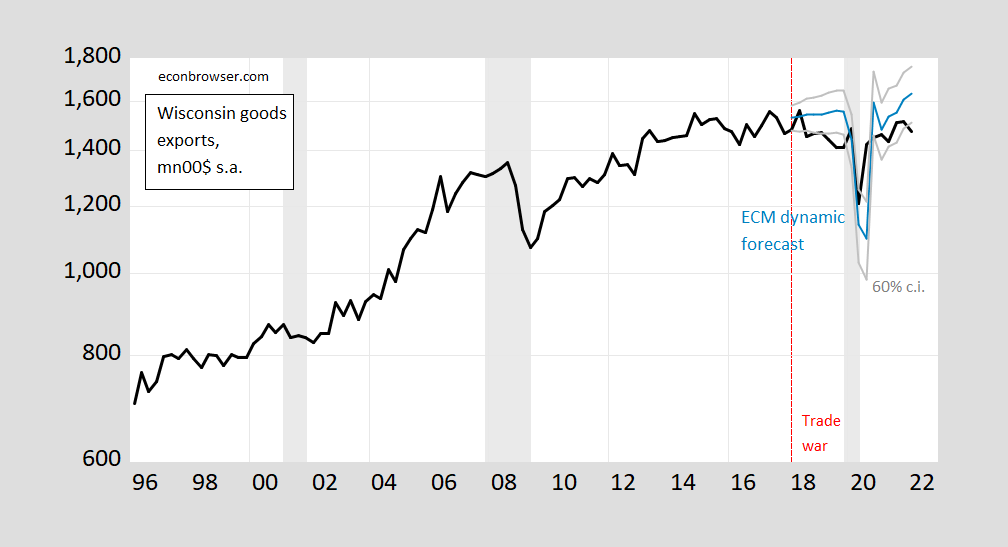

I use an error-corrected model involving exports, rest of the world GDP, and real exchange rates to estimate 1996-2017. The long-run elasticity of Wisconsin merchandise exports to Rest of World GDP is about 1.1, and the elasticity relative to the exchange rate is about 0.40. I use this equation to dynamically forecast 2018Q1-after, and get this (note: units are in millions, monthly rate):

figure 2: Merchandise exports from Wisconsin, $ million, $2000, seasonally adjusted (black, log scale), and dynamic forecast from ECM (blue), +/- 1 standard error confidence interval (gray line). The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA/Census, BLS calculated by FRED, NBER and authors.

Growing forecast errors have been linked to the start of the trade war. In other words, the historical correlation as of 2017 suggests that real exports will continue to grow (albeit slowly) through 2019, in line with world economic growth and a strong dollar.

Quantity matters? In the two-year trade war before the outbreak of covid-19, forecast errors averaged about $1 billion (2000 dollars). The actual export value in 2021 is about $14.6 billion in 2000, a decrease of 0.7%.

Forecast errors can be attributed to model specification errors, or the effect of other important determinants omitted from the specification of these three variables (adjusted R2 about 36%). Arguing on the basis of residuals is always dangerous, but at first glance, given what we know about trade partners retaliating against swing states, trade wars and retaliatory actions do not appear to be an implausible source of forecast error.

So (again), thank you Trump!

{kind=link}

{kind=link}