Survey Results (June 6-8), Re: GDP, Prices, Recession:

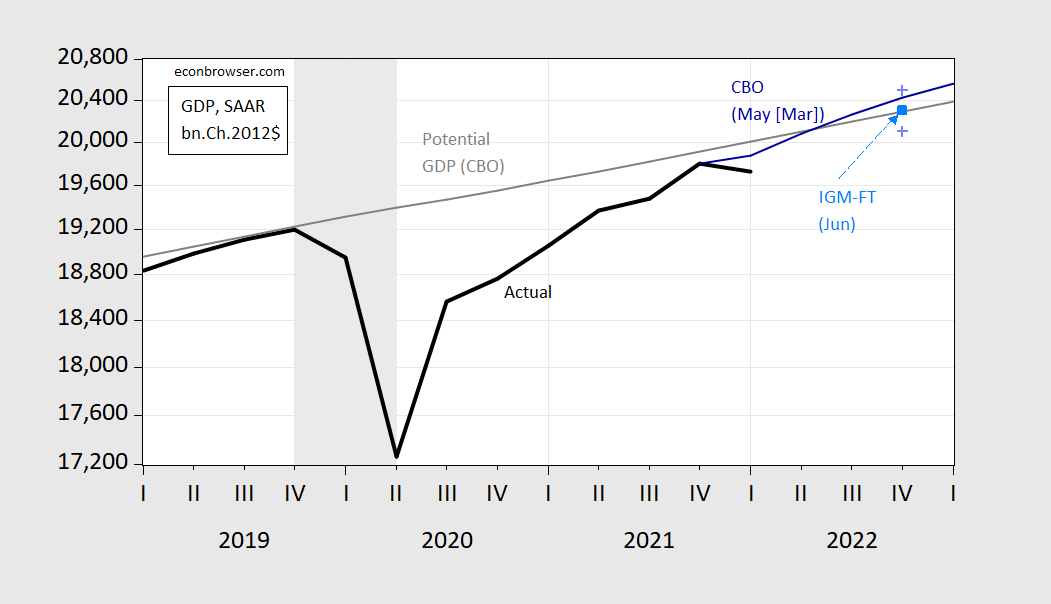

figure 1: GDP (bold black), potential GDP (grey), CBO forecast released in May (blue), professional forecaster survey released in May (red), WSJ Economist Survey (April), IGM -FT June Macroeconomist Survey Survey (Sky Blue), all in billions of Ch.2012$ SAAR, all in logarithmic units. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA (Second Edition), Congressional Budget Office (May 2022)SPF (May 2022), IGM-FT Survey (June 2022)NBER, and the authors’ calculations.

Note that unlike the previous episodes, the IGM-FT median survey and the SPF survey differ significantly in terms of GDP levels. The WSJ mean and IGM-FT median are not much different (as of the end of 2022), but this masks the fact that the IGM-FT forecast includes negative first-quarter growth, which the WSJ reported in April is not known in the survey. In this sense, therefore, the median forecast for the IGM-FT is much more optimistic than the outlook represented by the respondents to the WSJ and SPF.

The CBO’s forecast is more optimistic than others – but it’s important to remember that the CBO’s forecast is locked using data as of March 2 (that’s why it’s listed as May [Mar]) In the picture.

Interestingly, using the SPF or IGM-FT projections and the CBO’s measure of potential GDP, neither now nor through the end of the year will see a large positive output gap. Literally, this suggests that demand drivers are not the key to the inflation surge. Of course, the CBO estimate may be wrong (ie, overestimated). It cannot be said that the surge in demand occurred at a time when underlying GDP levels were overestimated, as the May 2022 year was higher than the July 2021 year, at least more than the 2021 year.

The averages for the 10th/90th percentile range provided by IGM-FT respondents are shown below.

figure 2: GDP (bold black), potential GDP (grey), CBO May forecast (blue), IGM-FT macroeconomist June survey (sky blue), 90th and 10th percentile Means (lavender +), all in billions Ch.2012 $SAAR, all on logarithmic scale. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA (Second Edition), Congressional Budget Office (May 2022), IGM-FT Survey (June 2022)NBER, and the authors’ calculations.

As for the likelihood of a recession, here’s where respondents put possible start dates.

resource: IGM-FT Survey (June 2022).

The modal response is 2023Q1-Q2; interestingly, this is earlier than 2023Q3-Q4 because Deutsche Bank forecast. as I am in In May, if using 10- to March or 10- to 2-year probabilities using the normal term diffusion model could yield very different results10 to 2 years yields a higher probability. Rashad Ahmed’s modelusing the offshore yield curve, gives a higher probability (although the increased probability is driven by financial conditions and oil prices).

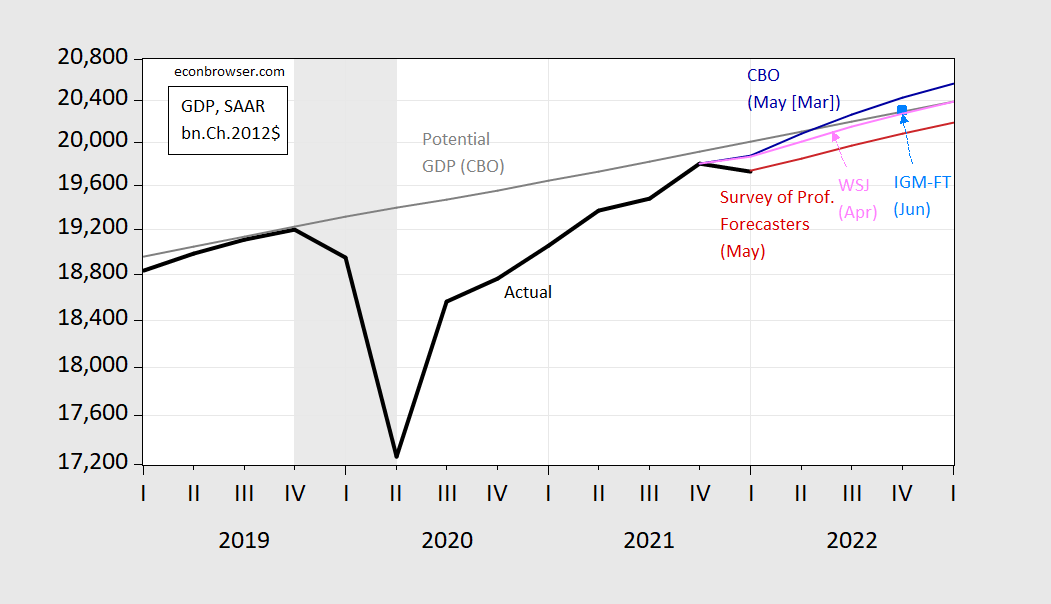

What about inflation? Here is a graph of the PCE deflator and median forecast from the IGM-FT survey.

image 3: Personal consumption expenditure chain type index (black), IGM-FT median forecast (blue square), and mean of 10th and 90th percentile forecasts (lilac+). The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, IGM-FT, NBER and author’s calculations.

The median forecast implies an annualized inflation rate of 5.07% from May to December (note that we only have numbers for April). This is lower than the inflation rate of 6.1 years in the preceding 12 months (both numbers are on a logarithmic basis).

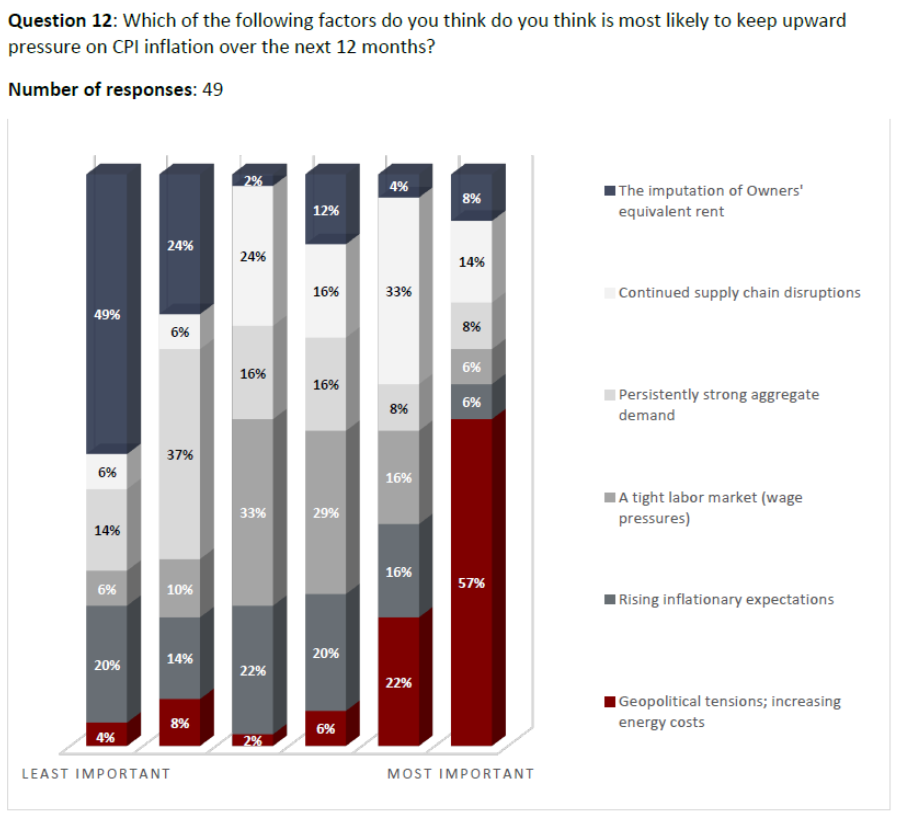

As for upward pressure on inflation over the next twelve months. Respondents said geopolitical tensions may be to blame. The main driver in second place is supply chain issues.

resource: IGM-FT Survey (June 2022).

Excess aggregate demand accounted for only 6% of the response, suggesting that demand-pull factors will not be central to driving inflation next year.

This Financial Times The article is. here (paywall).

{kind=link}

{kind=link}