from Article 4 Consulting:

resource: International Monetary Fund, U.S. Article IV Consultation Report, July 2022.

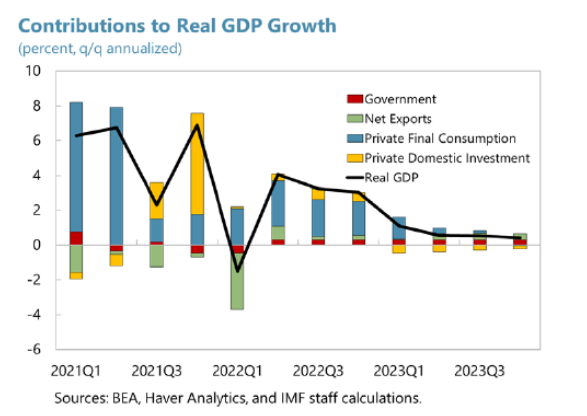

The sharp rebound in gross domestic product in the second quarter did not match the near-term forecast. The change (in a mechanical sense) in the contribution of net exports from a large negative to a small positive does much to restore the projected growth. The report states:

All in all, growth is expected to decline to 0.7% q4/q4 by the end of 2023, before gradually picking up to 2024. The U.S. is expected to narrowly avoid a recession. Still, the risk of the economy “stagnating” and slipping into a brief downturn remains high. In particular, the expected slowdown could turn into a short-lived recession if the economy suffers another negative shock. As economic activity slows and supply-demand imbalances are resolved, PCE inflation is expected to decline steadily, falling 2% year-on-year by the end of 2023.

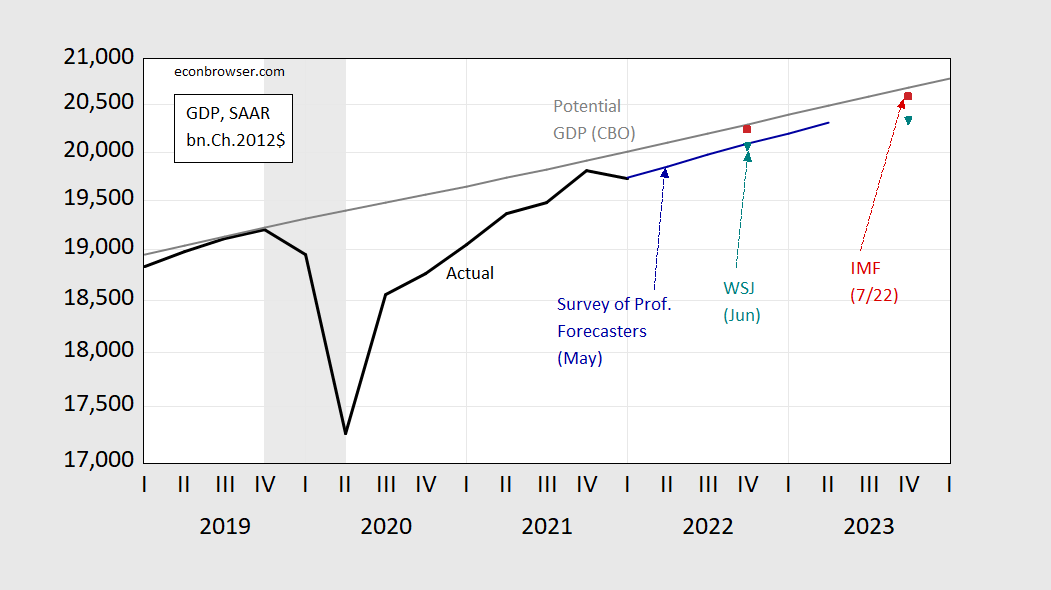

Figure 1 below shows the IMF forecast for Q4/Q4 2022 of 2.2% (this is a Downgrade from 2.9% forecast At the end of last month’s team visit) compared to other forecasts and potential GDP.

figure 1: GDP (black), Potential GDP (grey), Professional Forecaster Survey May Consensus (blue), Wall Street Journal June Survey Average (turquoise) and IMF Article IV Advisory Forecast (red), all in billions Unit Ch.2012$ SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, CBO, Philadelphia Fed, Wall Street Journal (June survey), IMF, NBER, and author’s calculations.

The IMF’s forecast – in terms of levels – is more optimistic than the Wall Street Journal’s June consensus and the May poll of professional forecasters.

{kind=link}

{kind=link}