Paul Krugman This reminds me why “expected” inflation doesn’t necessarily translate to one-to-one actual inflation, because of nominal rigidities like staggered contracts.He also drew my attention to the company’s expected costs (rather than their expected prices), using Atlanta Fed’s “Business Inflation Expectations”. Here’s how these expectations compare to others, and how costs have actually evolved.

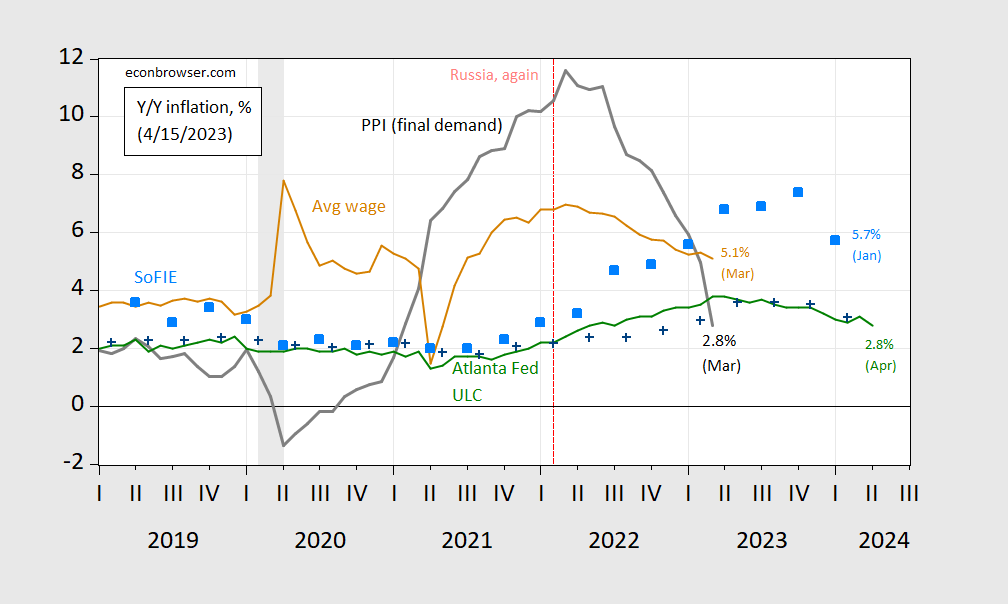

figure 1: Year-over-year PPI for final demand goods and services (black), average hourly earnings for production and non-management workers (tan), unit labor costs (green), and inflation (sky blue squares) from surveys of business inflation expectations and surveys of professional forecasters median of (blue +). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: BLS via FRED (FRED series PPIFIS, AHETPI), Federal Reserve Bank of Atlanta, Coibion-Gorodnichenko Sophie, Federal Reserve Bank of PhiladelphiaNBER and authors’ calculations.

I am interested to observe (as expected) that unit labor costs do not vary one-to-one with expected inflation as measured by the median Coibion-Gorodnichenko SoFIE. Given the strong composition effect during the pandemic, one shouldn’t take too much away from the gap between average wages and unit labor costs.

For various CPI inflation measures see here postal.

{kind=link}

{kind=link}