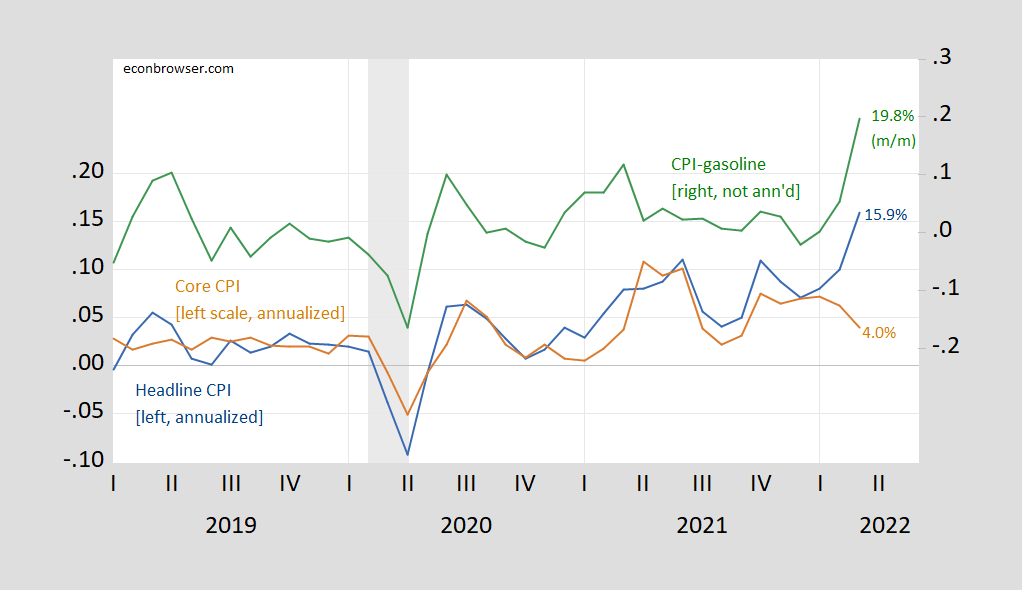

Clearly, gasoline (and energy prices) have a big impact on headline inflation. Monthly inflation hit a Bloomberg consensus of 1.2%, while core inflation was below 0.3% versus a consensus of 0.5%. However, it is useful to know exactly how many titles and core divergences have occurred over time.

figure 1: Month-on-month annualized CPI inflation (blue, left scale), core CPI inflation (brown, left scale), and CPI gasoline component inflation, unannualized (green, right scale). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: BLS, NBER, and author’s calculations.

Core inflation fell, while gasoline prices rose nearly 20% (month/month not yearly).

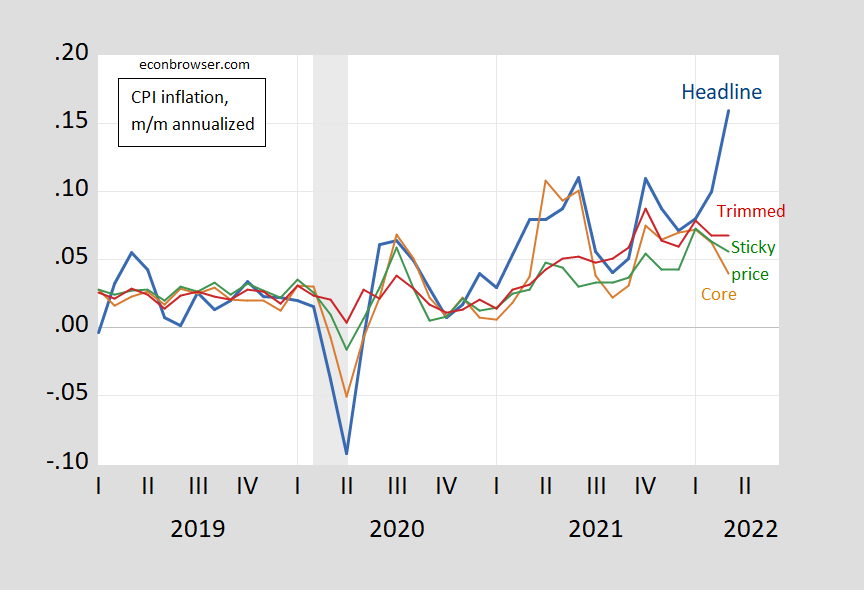

As shown in Figure 2, adjusted CPI inflation declined, indicating a reduction in the breadth of price inflation. Sticky price CPI inflation has also declined, suggesting that infrequently changing prices are also rising at a slower pace.

figure 2: MoM annualized CPI inflation (bold blue), core CPI inflation (orange), 16% cut CPI inflation (red) and sticky price CPI inflation (green). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: BLS, NBER, Cleveland Fed, Atlanta Fed, and author’s calculations.

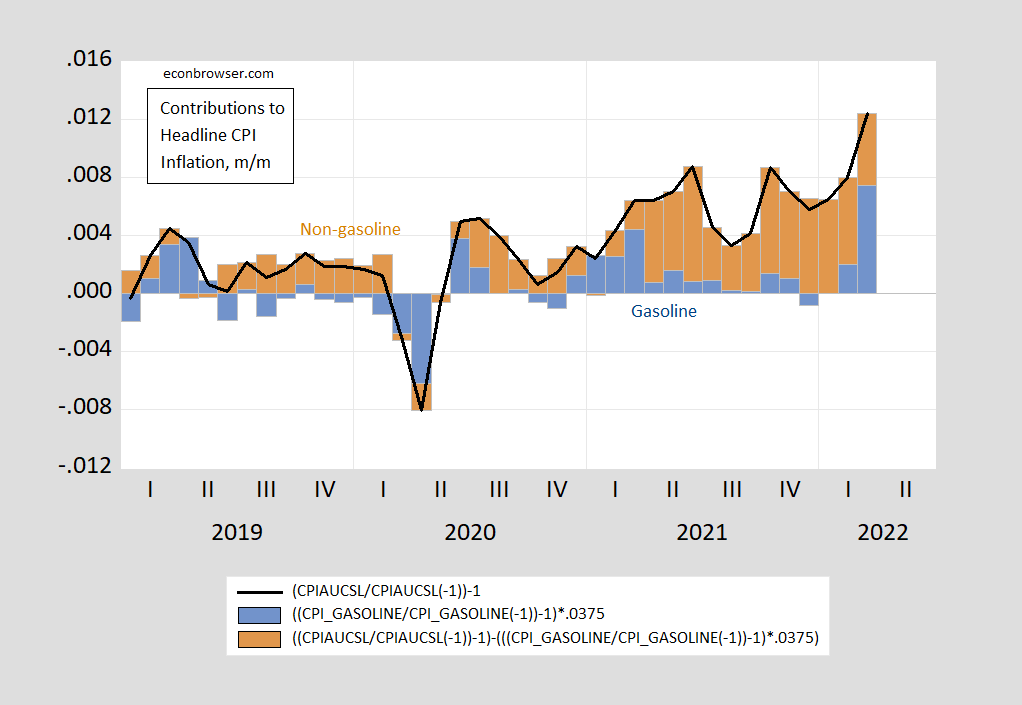

To isolate the contribution of gasoline prices to the rise in the CPI, I mechanically break down the CPI into gasoline and non-gasoline components (using the 3.75% weight of gasoline in the CPI).

image 3: Monthly headline CPI inflation (black line), gasoline contribution (blue bar), non-gasoline contribution (brown bar). Source: BLS and author’s calculations.

Gasoline alone accounted for 0.74 percentage points of the 1.24 percentage point month-on-month inflation rate.

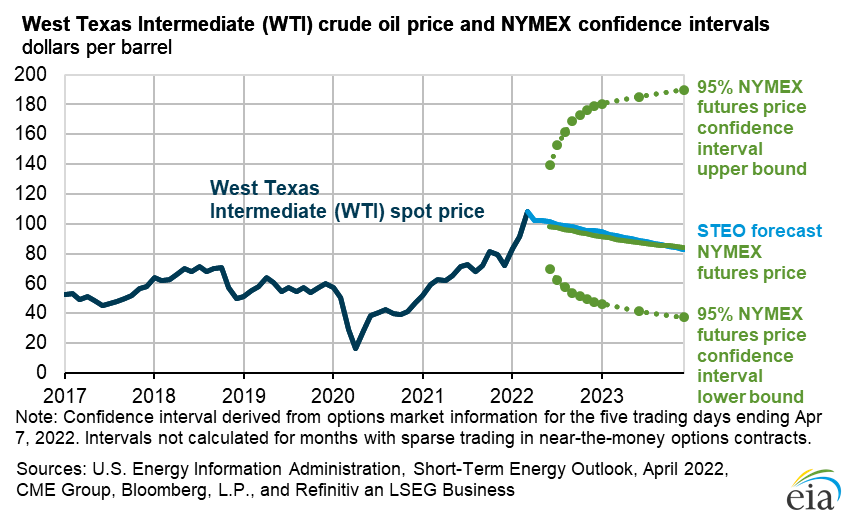

Obviously, as pointed out in yesterday’s post, gasoline price movements in relation to oil prices will determine the trajectory of inflation in the short term. Here, the forecast is down – but the confidence interval is very wide (I’m assuming the same forecast and uncertainty properties for Brent).

source: DOE EIA.

If oil prices do fall in April, gasoline prices should be deducted from headline inflation. But given the geopolitical conditions, I wouldn’t bet against that happening.

see more from thisespecially with regard to how vehicles increase CPI inflation.

{kind=link}

{kind=link}