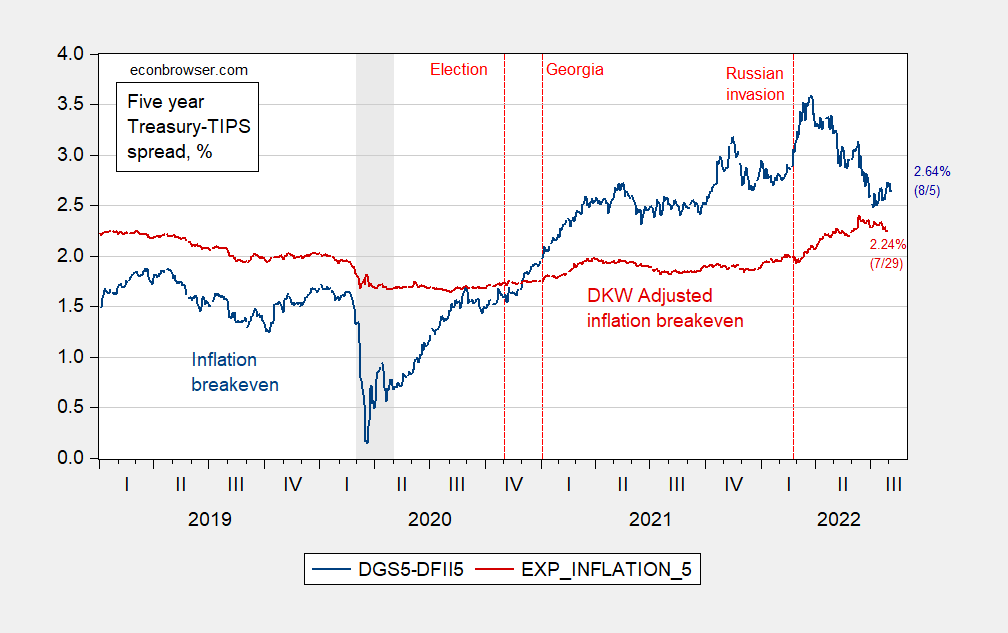

Expected inflation inferred from the US Treasury-TIPS spread is influenced by Risk and Liquidity Premium. The difference between expected future short-term rates and current short-term rates is also masked by a risk premium. Here are the adjusted spreads:

figure 1: Five-year inflation breakeven calculated as five-year Treasury yield minus five-year TIPS yield (blue, left scale), five-year breakeven adjusted for inflation risk premium and liquidity premium per DKW (red, left scale), both In units. Recession dates as defined by NBER are shaded in gray. Source: FRB via FRED, Treasury, NBER, KWW Following D’amico, Kim and Wei (DKW) access 8/4, and author’s calculations.

The adjusted series shows that inflation is expected to rise as Russia expands its invasion of Ukraine, but it is lower than that indicated by the simple Treasury-TIPS spread (which has not been trending lower recently).

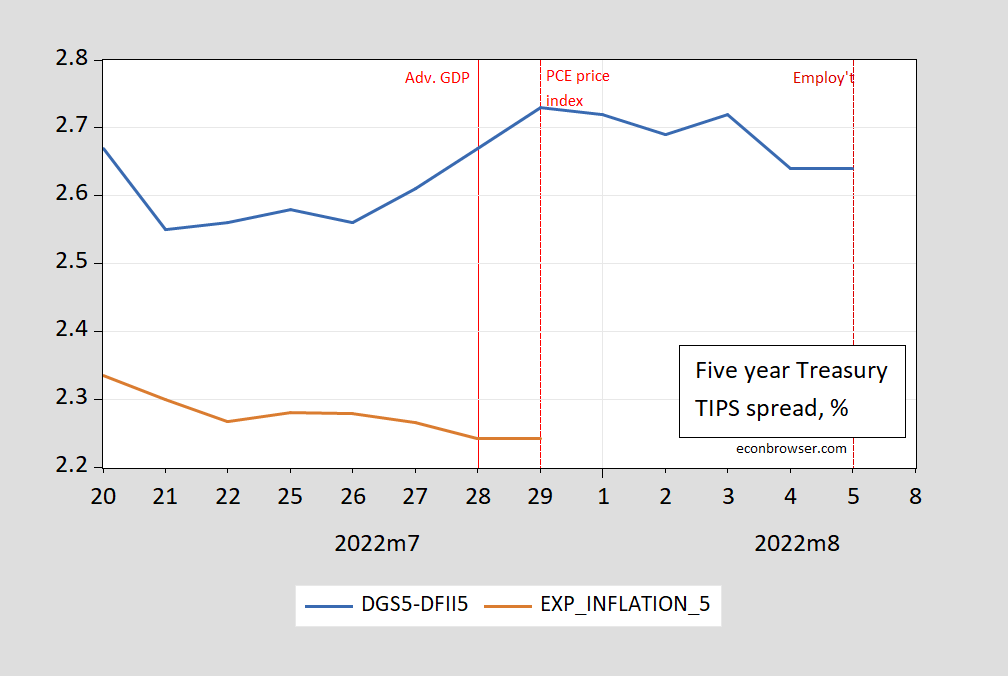

How do recent data affect inflation expectations? Figure 2 gives a detail.

figure 2: Five-year inflation breakeven calculated as five-year Treasury yield minus five-year TIPS yield (blue, left scale), five-year breakeven adjusted for inflation risk premium and liquidity premium per DKW (red, left scale), both In units. Source: FRB via FRED, Treasury, KWW Following D’amico, Kim and Wei (DKW) access 8/4, and author’s calculations.

Inflation breakeven rose with GDP growth and the PCE deflator release, but was unchanged (oddly) with today’s jobs data. However, as far as the US Treasury-TIPS spread miscalculation is concerned, we should be wary of this result (inflation expectations do decline with the release of adjusted GDP).

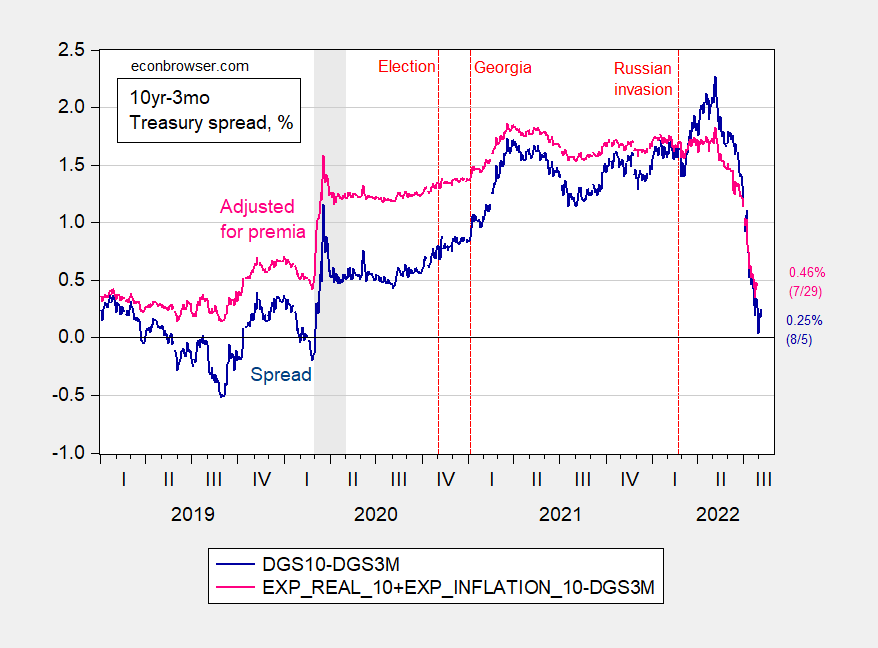

How about the 10yr-3mo spread? Unadjusted prices have fallen sharply in recent weeks and are close to inversion.

image 3: 10-year to 3-month Treasury spreads (dark blue) and implied nominal interest rates over the next ten years (pink), both expressed as a percentage. Recession dates as defined by NBER are shaded in gray. Source: FRB via FRED, Treasury, NBER, KWW Following D’amico, Kim and Wei (DKW) access 8/4, and author’s calculations.

The gap between 10 years and 3 months was negative in 2019 and reappeared as the pandemic hit. The yield curve steepened sharply with the Georgia special election result, then counter-intuitively rose again as Russia expanded its invasion of Ukraine. Since May 6, the spread has dropped sharply.

Spreads contain an inflation risk premium, so on average, the yield curve slopes upward. Therefore, the standard 10yr-3mo spread is not necessarily equal to the difference between the 3-month yield over the next 10 years and the current 3-month yield. I show the sum of the next 3-month real yield and the next 3-month inflation rate as the pink line in Figure 2. This line may be a better indicator of Q1-Q2 2021 growth expectations and the decline in the perceived growth outlook in May.

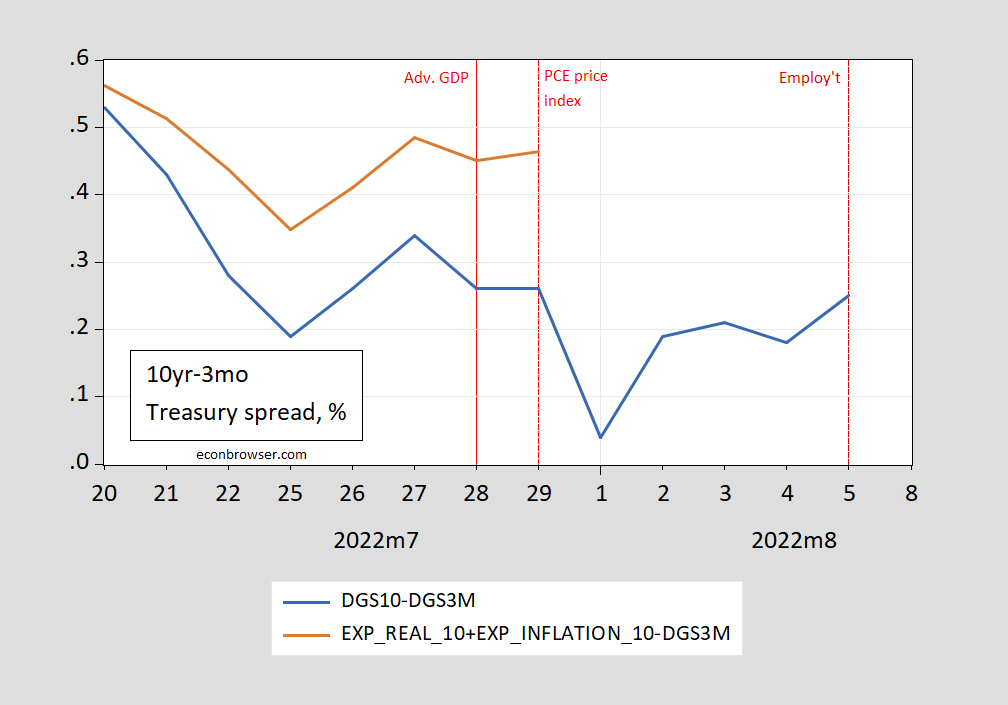

Details also indicate the expected reaction of asset prices to recent releases.

Figure 4: 10-year to 3-month Treasury spreads (dark blue) and implied nominal interest rates over the next ten years (pink), both expressed as a percentage. Source: FRB Follow D’amico, Kim and Wei (DKW) via FRED, Treasury, KWW Access 8/4, and author’s calculations.

{kind=link}

{kind=link}