I’ve read an interesting report over the past few months that suggests a shift in perceptions about inflation – no longer those that try to imply government spending is excessive, poorly designed monetary policy (particularly QE) or The cliché that drags down the usual suspects – exorbitant wage demands from workers. All the usual narratives are very convenient frameworks in which those with financial power can extract more real income at the expense of the rest of us. At least, we’ve been taught that we don’t have power. But, of course, if we organize well enough, whether we can overthrow the entire system of capitalist domination is another matter. Back to the inflation frame. While it can be argued that distributional struggles between workers (organized into powerful unions) and companies (with significant pricing power in less competitive industries) helped spread the initial OPEC oil shock of 1973 into a long-term Inflationary events such as 2022-23 are under-narrated. Workers are now largely disorganized and submissive. New thinking began to focus on the role of corporations—a term now being used is “greed inflation”—to describe this new era of profit fraud and its impact on the trajectory of inflation. This shift in focus is justified and welcome, as it highlights the imbalances in the capitalist system and another way in which it is prone to crises.

A recent report by British Unite the Union (published March 2023) – Unite Investigates: Windfall profits across the economy — and it’s systemic – Provide convincing evidence of:

We live in a crisis of profiteering…

…the key industries between them are driving inflation above 57%: the energy, food, auto and transportation sectors, including road freight and shipping, which keep our economy running…

…profiteering results in exorbitant prices we all have to pay – not workers’ wages. …

Rampant corporate profiteering exacerbates cost of living crisis…H1 2022 margins are 89% higher than 2019 H1,,,

The crisis is systemic: Encouraged by governments, corporations and investors have won enormous power to set the rules and reap the rewards. Their economy has failed the vast majority of us, both as workers and consumers.

This well-researched Unite report is truly breathtaking, even for someone like me who examines the data on a daily basis and has a keen sense for the way capital leverages its power.

Unite researchers looked at the accounts of the FTSE’s top 350 companies and found that:

1. Profit margins “jumped 73%” in 2021 compared to 2019 (on average).

2. “The profit margin in the first half of 2022 is 89% higher than the same period in 2019”.

3. Profit margin in the first half of 2019 was 5.7%.

2. Increase to 10.7% in the first half of 2022.

The report notes that the company’s unit costs have risen due to supply constraints caused by the pandemic:

The initial triggers for inflation are “supply shocks,” including the climate crisis, post-pandemic bottlenecks, and most recently, the war in Ukraine. But many companies have used the opportunity to boost profits, driving prices up even further.

Consequently, the price increases observed in the UK far exceeded any justification that could be justified by rising input costs (whether raw materials or labour).

The mechanisms that companies use to make a profit are identified as:

1. An initial “supply crunch” – creating an imbalance between spending (demand) and supply (constrained), creating an environment where prices start to rise as unit costs increase.

It should be noted that many of the factors that created the supply crunch have dissipated (transportation shortages, etc.) or are being resolved – which would make the inflationary impulse temporary.

2. A “demand surge” – at the end of the “constraint phase” of the pandemic, consumers again began spending freely on a range of goods and services before supply constraints were resolved – reinforcing the environment for price increases.

Short-term fluctuations in demand do not justify viewing this period of inflation as a “demand-pull” event, as consumers quickly adjust back to more normal behavior and the supply side catches up anyway.

This temporary imbalance between supply and demand is what central banks use to justify their rate hikes.

But their logic is wrong, because the main source of initial inflationary pressure is supply constraints, and they are easing.

That leaves us with the question: Will interest rates fix “greedy inflation” — companies that jack up profits?

The answer is unlikely.

3. “Market windfalls” – this has to do with “centralized market structures” that favor companies – such as energy markets, etc.

In Australia, for example, large gas companies have shifted domestic supplies to world export markets, where prices are much higher due to the disruption caused by Russia’s invasion of Ukraine.

Then, as this creates a threat of shortages in the domestic market, they are driving domestic prices significantly higher.

However, Australia produces far more natural gas than we use domestically.

Mistakes: Poor government regulation and corporate profits.

4. “Market Concentration (Oligopoly)” – We see this in energy, shipping, ports, supermarkets, banks, etc.

The idea that capitalism is about “competition” is a myth.

Companies do their best to eliminate competition through aggressive takeovers, acquisitions, etc., and then use their market power to drive prices excessively high.

5. “State-sanctioned monopoly” – Privatization effectively transfers public wealth into the hands of profit-seekers in the private sector who then exploit the “essential service” nature of their activities to profiteer.

The problem is again the lack of state regulation and privatization.

We are told that privatization increases competition, reduces unit costs, and improves product and service quality.

The reality, after about 4 years of this folly, is that the promise to justify the sell-off and massive transfer of public wealth is hollow.

The Unite report clearly states “who is responsible”.

1. “Politicians, the media and the Bank of England are still largely ignoring the profiteering crisis”.

Remember the Governor of the Bank of England warned workers and told them they had to take pay cuts because they caused inflation.

With real wage cuts happening, but inflation accelerating the attack on workers is just masking disregard for what companies are doing.

2. The survey evidence clearly shows that most businesses are using inflation as a veil to drive prices “beyond what is needed to offset cost increases”—in other words, rebalancing the income distribution in favor of workers at their expense.

3. Another key finding is that it is not just a few rogue companies that are making huge profits.

The Unite report said it was a “systemic” activity where “(e) the entire industry chose to take advantage of the crisis, leading to ever-increasing prices for commodities we all need.”

The findings of the Unite report are also consistent with the Guardian analysis (April 27, 2022) – https://www.theguardian.com/business/2022/apr/27/inflation-corporate-america-increased-prices-profits.

The study found that in the United States:

…Top corporations … enjoyed rising profits while passing the costs on to customers, many of whom were struggling to afford gasoline, food, clothing, housing and other basics.

But it’s not just about passing on higher costs.

What is happening is different.

Companies are using the mechanisms described above to readjust the distributional balance by improving profit margins.

It’s one thing to pass on rising unit costs — keep raising prices.

But corporations are pumping up markups and being the source of an inflationary spiral, not just fighting inflation.

I have referred to the initial shocks of these events, and then the role of the mechanisms that propagate the initial shocks to broader, longer-lasting inflationary events.

In the 1970s, the initial shock was OPEC’s oil price hikes, propagated by the interaction between powerful unions and corporations over who would bear the real loss of income from higher import prices.

What is shocking in the current period is the pandemic, OPEC and Russian folly.

And now, the shock is spreading to something more permanent through profit fraud.

Isabella Weber also has an interesting column (March 13, 2023) – New Economic Policy Handbook – Discussed the topic and made the case for price controls to stop companies from pumping up prices.

I will consider price control issues in a future blog post.

What about Australia?

There is strong evidence that the same factors are at play in Australia that the Unite report and the Guardian study of the UK and US found.

Between the December 2019 quarter (just before the pandemic) and the December 2022 quarter, total operating surplus as a share of total factor income rose by 3%, while labor compensation’s share fell by 2.4% (see The following figure) ).

Gains in the profit segment were mostly captured by companies in the small business sector, which experienced smaller profit growth.

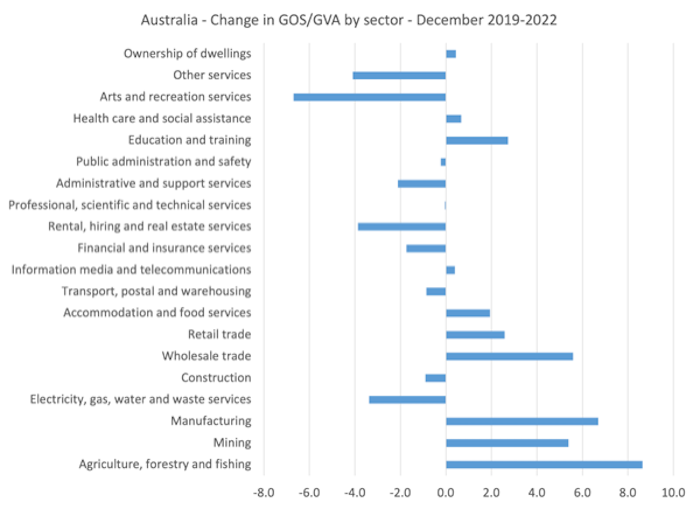

In terms of GOS’s share of gross value added (output), there is wide variation across industry structures.

The chart below shows the percentage change for all industries between the December 2019 quarter and the December 2022 quarter.

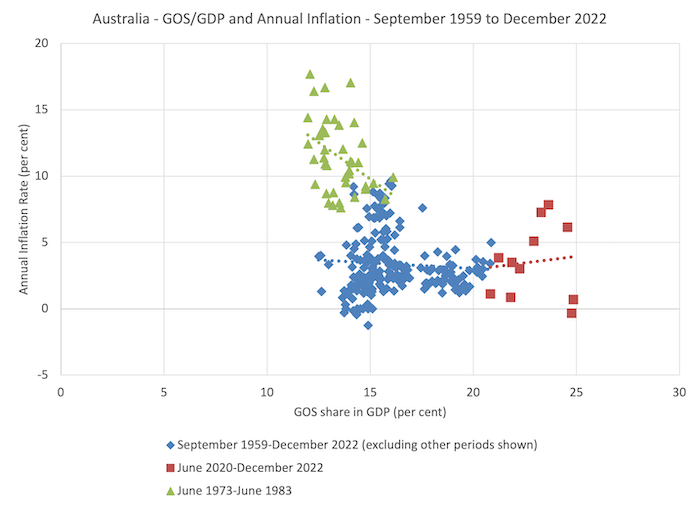

Another way of thinking about it is to track the GOS/GDP ratio since the September 1959 quarter (the start of modern national accounts data) and match that to the evolution of inflation in Australia.

The graph below shows the GOS share on the horizontal axis for three different periods:

1. June Quarter 1973 to June Quarter 1983 – “Inflation in the 1970s”.

2. June 2020 quarter to December 2022 quarter – “Pandemic Inflation”.

3. All other quarters between September 1959 and December 2022.

The dashed lines are just the respective least squares trendlines for the above subsamples.

Thus, during the inflationary period of the 1970s, it is difficult to say that the annual rate of inflation was driven solely by changes in the GOS’s share of GDP.

But in the near term, the relationship between these two variables is quite different and positive – the higher the GDS share, the higher the inflation.

While a cross plot like this (known in the industry as an “eyeball”) doesn’t tell us what drives what — i.e. causation — it gives us a clue to drive further research.

If I do a detailed regression analysis, I find that a higher GOS share – that is, a higher profit share – is a significant factor driving the trajectory of inflation in the most recent period.

in conclusion

Along the lines of the Unite study, a more detailed analysis of companies’ financial statements will help to really pinpoint where and to what extent profit fraud is occurring in Australia.

But the sectors where Unite found the worst breaches also occurred in Australia – energy, supermarkets, utilities.

Our banks will also be affected.

I’ll probably do that exercise at some point, but for now it distracts me from the lengthy project I have to complete.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}