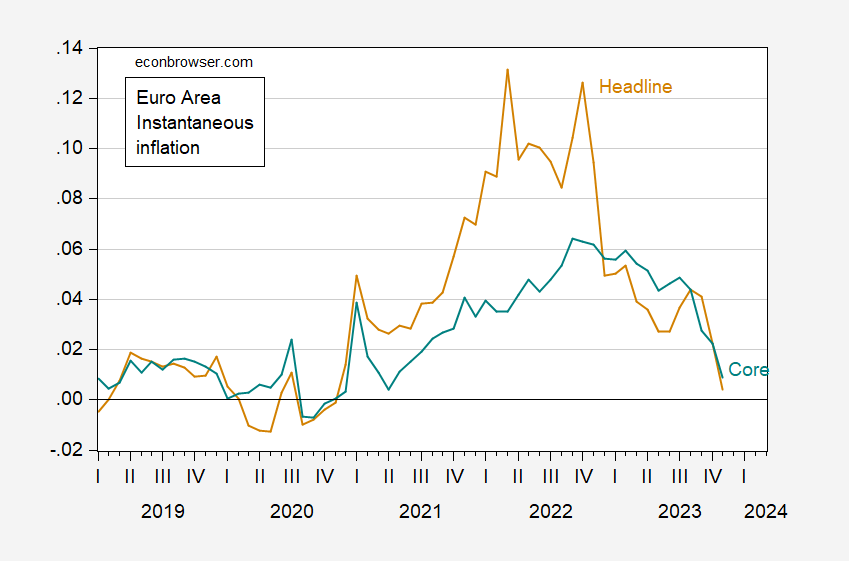

Headlines showed that the Eurozone HICP inflation rate was 2.4%, reaching consensus. The instantaneous inflation rate for each Eeckhout (T=12,a=4) is 0.4%.

figure 1: Euro area instantaneous inflation headlines (tan), core (cyan).Seasonally adjusted using X13 (log transformed; X11 ARIMA), calculated using Eckhout(2023) Definition, T=12, a=4. Source: Eurostat via FRED, author's calculations.

The wide gap between the headline and core data shows the role of energy in euro zone inflation. A comparison of the core inflation series suggests that demand-side factors in the United States and the euro area may play a greater role by August 2022. But it may also indicate the role of supply-side factors, as non-energy non-food prices may be driven by labor market tightness or non-food non-fuel import prices (i.e. supply chain disruptions).

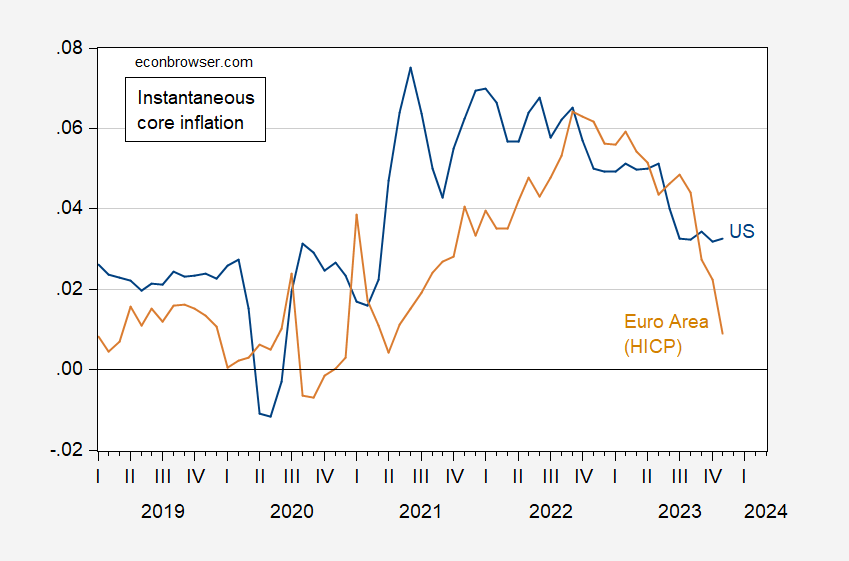

figure 2: Eurozone instantaneous core inflation headlines (tan), US CPI core inflation (blue).Seasonally adjusted using X13 (log transformed; X11 ARIMA), calculated using Eckhout(2023) Definition, T=12, a=4. Source: Eurostat via FRED, author's calculations.

Figure 2 shows that core inflation in the United States has been more persistent than in the euro area. This could be seen as bad news; or it could be seen as a sign that the eurozone is heading towards recession faster.

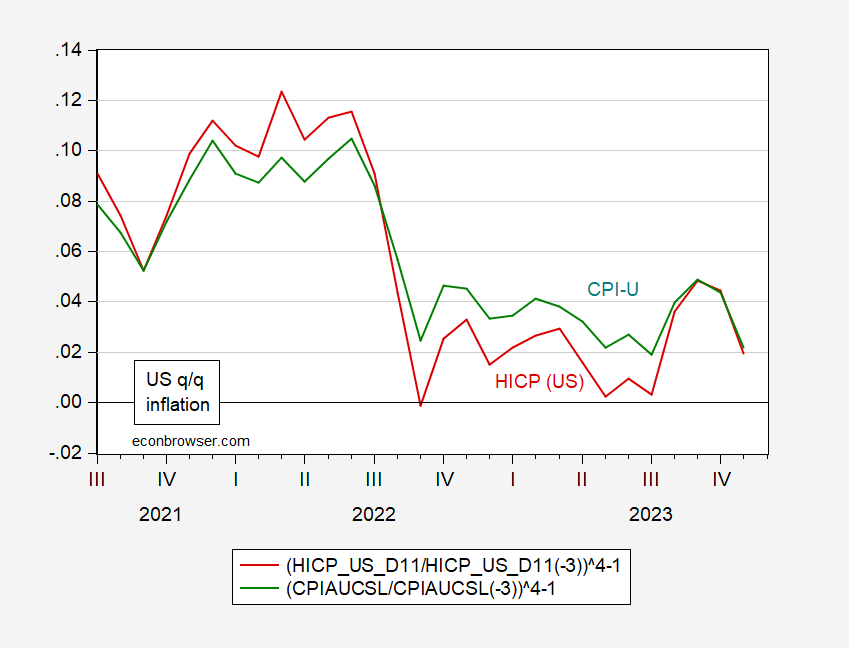

Note that HICP and CPI move in somewhat different ways in the United States, but not completely. To illustrate this, I plotted q/q CPI and HICP inflation rates in Figure 3.

image 3: US HICP quarterly inflation (red). Seasonally adjusted using X13 (log transformed; X11 ARIMA) and US CPI q/q inflation rates, both annualized. Source: Eurostat via FRED, author's calculations.

{kind=link}

{kind=link}