this is a title Article written by S. Ganguly for Reuters.

A Reuters poll of bond market experts conducted from March 6 to 12 showed that nearly two-thirds of strategists (22 of 34) said the yield curve is no longer as predictive as it once was.

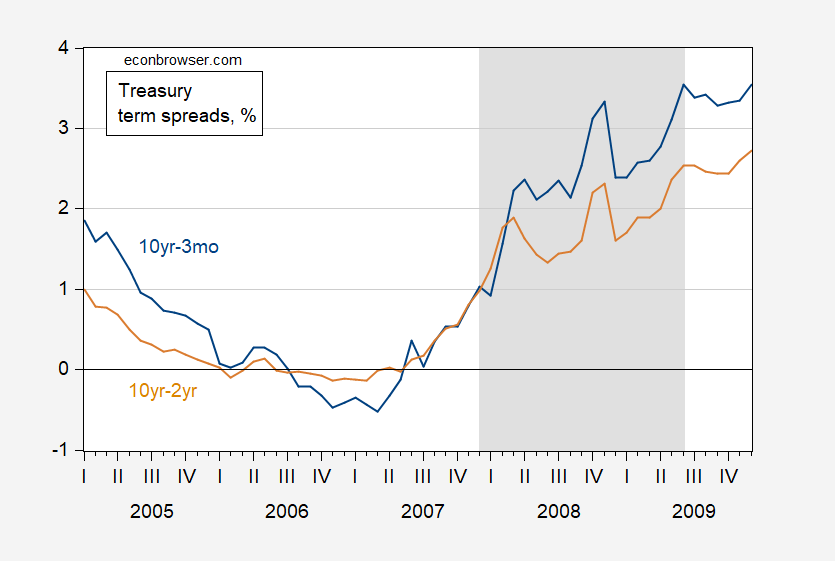

Here is a chart of the spread as of March 14th.

figure 1: The 10-year minus 3-month spread (blue) and the 10-year minus 2-year spread (tan), both expressed as a percentage. March data is as of March 14. Source: Treasury via FRED and author's calculations.

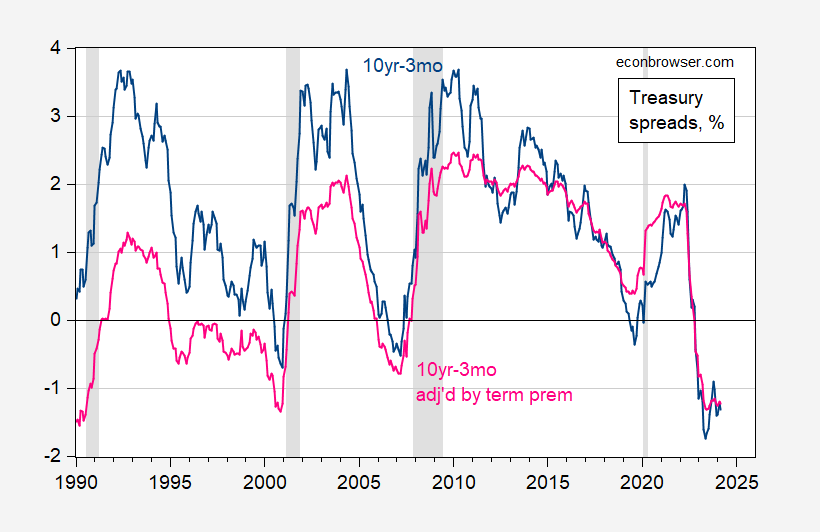

For comparison, note that the Great Recession was preceded by a reversal that began a year and a half before the NBER-defined peak.

figure 2: The 10-year minus 3-month spread (blue) and the 10-year minus 2-year spread (tan), both expressed as a percentage. NBER-defined recession peak-to-trough dates appear gray. Source: Treasury Department through FRED, NBER, and author's calculations.

We're currently about a year and a half away from the 10-year to 2-year spread becoming negative, so I would say that while the economy is clearly strong right now, it's too early to say we're safe (well, as of 2 month’s data)).

Why did some economists underestimate the predictive power of the reversal this time?

“If these two things happen at the same time – real money demands for long-term funding from pension funds and others are unable to be met, and the Fed keeps front-end rates higher due to the economy's resilience – the curve will remain inverted for some time.”

My interpretation is that the typical correlation between inversions and recessions is broken because the term premium on long-dated bonds is smaller than usual. consider:

Then the interest rate spread between 10 years and 3 months is:

![]()

along with TP terms are smaller than usual, then the pure EHTS rate may be higher than that of a typical inversion.

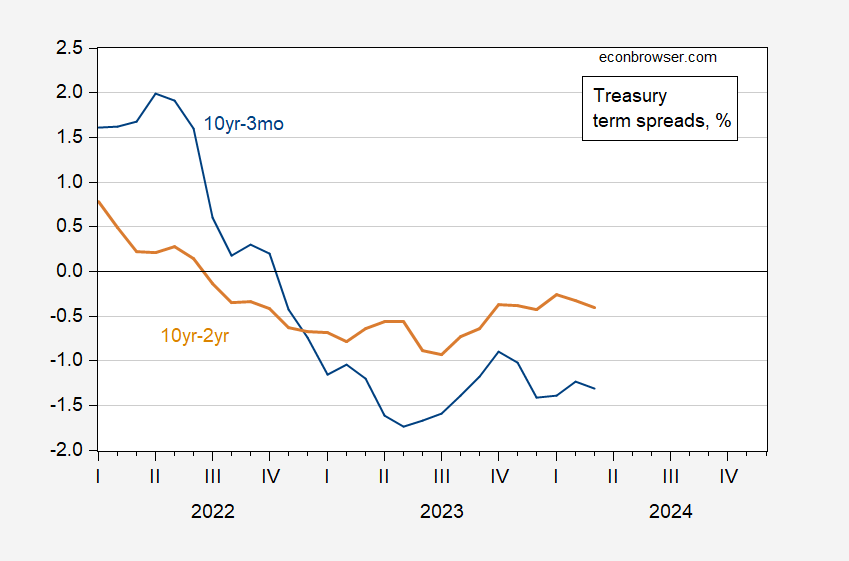

While the argument for a low or negative term premium sounds plausible, adjusting for the spread by the estimated term premium (FRED's Kim-Wright 10-year, series THREEFYTP10) does not seem to change our view of how inversions relate to subsequent recession-related perceptions.

image 3: 10-year minus 3-month Treasury spread (blue), 10-year minus 3-month Treasury spread adjusted for Kim-Wright estimated term premium (pink), both expressed as percentages. NBER-defined recession peak-to-trough dates appear gray. Source: Treasury, Kim-Wright, FRED, NBER, and author's calculations.

Therefore, I join Cam Harvey (He emphasized the yield curve as a predictor of recession.) He said it was too early to give up on recession predictions.

{kind=link}

{kind=link}