Answer: No.

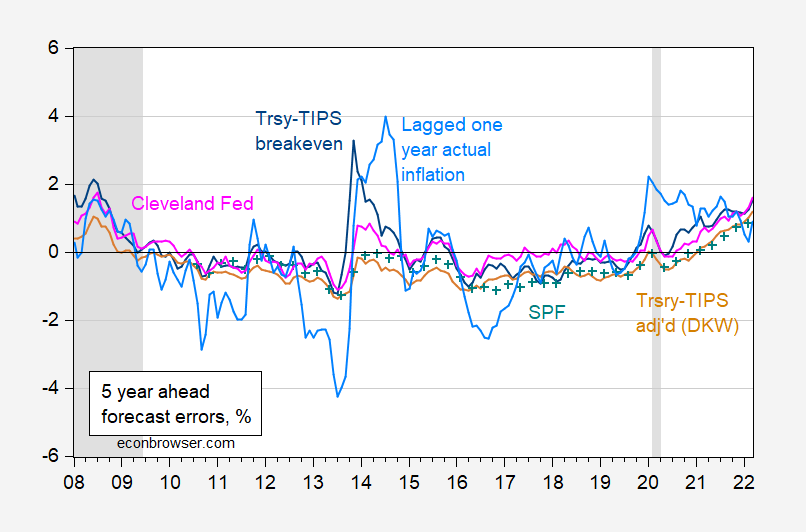

Here’s a picture of five-year CPI inflation expectations being wrong.

figure 1: Real 5-year ex-post inflation minus 5-year Treasury-TIPS breakeven expectations (dark blue line), from Treasury-TIPS breakeven, KWW-adjusted premiums after DKW (tan), from Cleveland’s Survey of Professional Forecasters Median (blue+) Fed (pink), lagged ex-post one-year inflation (sky blue). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: For CPI, BLS via FRED (CPIAUCSL); the inflation rate calculated by the author using the exact formula (not a logarithmic approximation). FRED’s Treasury and TIPS (GS5, FII5), the adjusted break-even kilowatt (Access 4/8), for SPF Federal Reserve Bank of Philadelphia, cleveland fedand National Bureau of Economic Research.

Since the reader, I have provided hyperlinks to specific data sources john h. wrote: “Hard to argue with data that doesn’t link to any particular source data!”

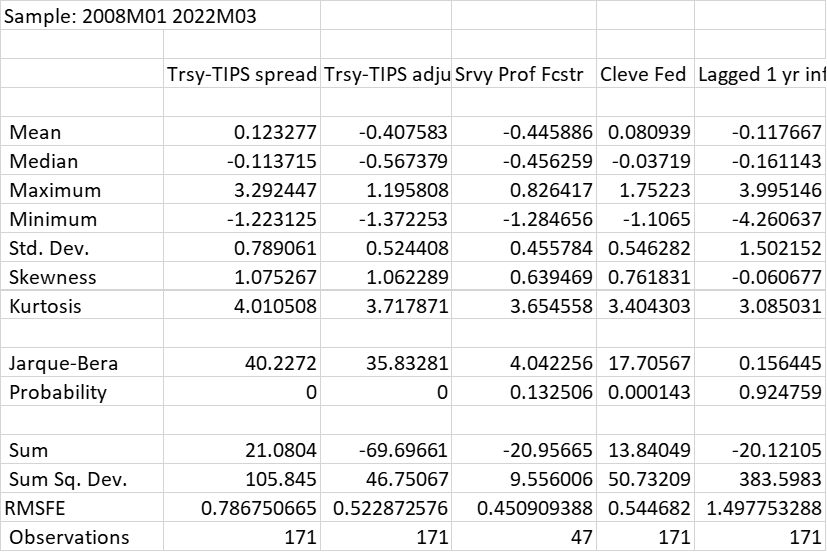

During 2008M01-2023M02, the average error (absolute value) is the smallest for the Cleveland Fed. The smallest median error (in absolute value) comes from the Cleveland Fed. The largest maximum forecast error is for inflation lagged by one year. The smallest minimum forecast error is for inflation lagged by one year. The largest mean squared forecast error (by far!) is for inflation lagged by one year.

I think it’s reasonable to conclude (if you don’t already know) that adaptive expectations using inflation lagged by one year are poor predictors of inflation five years in the future (or 10 years in the future).

{kind=link}

{kind=link}