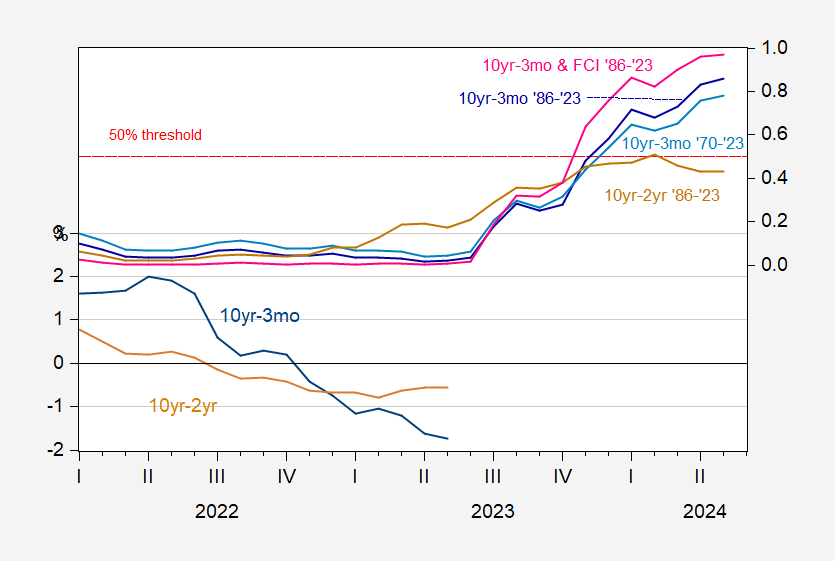

Apologies to Lawrence Oliver “Marathoner”. Described by Derek Thomson of The Atlantic “How Recession Doom Got the U.S. Economy So Wrong”. Personally, I don’t think we should rule out a recession, despite the recent abundance of good data.First, the term spread model implies that Downturn/recession in Q4 2023 (Using a 50% threshold), we’re still in Q3. Second, the numbers will be revised — GDP in particular will be substantially revised.

For the first point, I repeated the probability plot derived from the term propagation model June assessment.

figure 2: The 10-year-3-month Treasury spread (blue, left scale) and the 10-year-2-year spread (tan, left scale), both in %; and the 10-year-3 Recession probabilities for months (dark blue, right axis) and measured by financial conditions index (pink, right axis), 10-year to March term spreads (light blue, right axis) from 1970 to May 2023 Enhanced, and 10 to 2 years from 1986 to May 2023 (brown, right scale). Recession peak-to-trough dates as defined by NBER are grayed out. Regression assumes no recession through May 2023. Sources: Treasury Department via FRED, Chicago Fed via FRED, NBER, and authors’ calculations.

Therefore, based on these term spread/probability models, a recession is not out of the question if the historical correlation persists into the 2023-24 period.

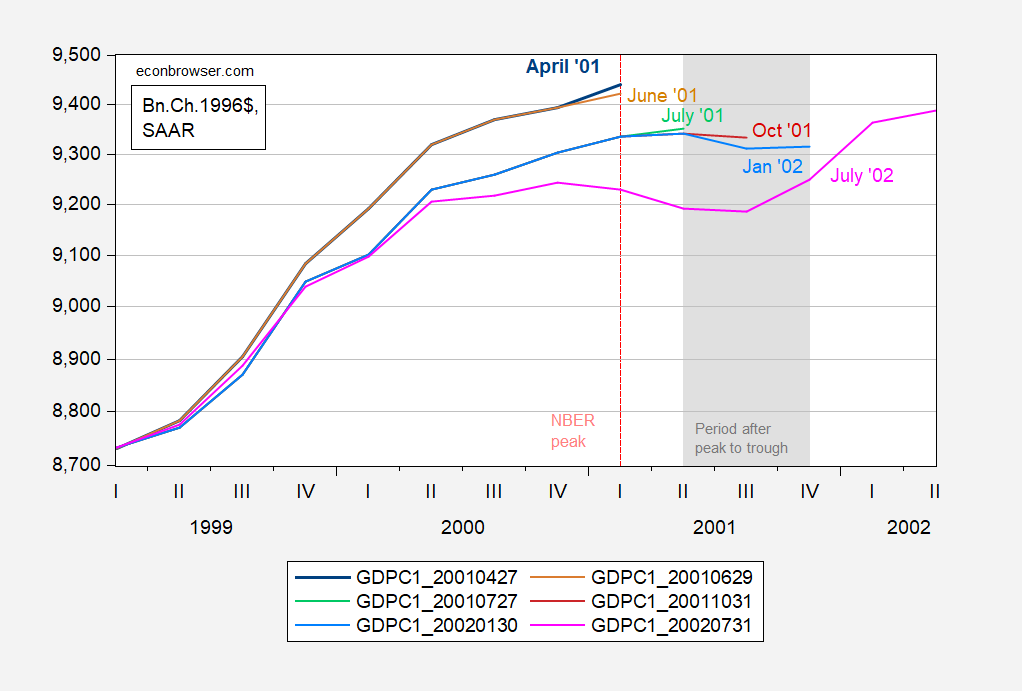

On the second point, as I reflect back on my own experience as a senior government economist, a colleague of mine told me that the data currently being reported ensures that there will be no recession. That was in April or May of 2001, if I remember correctly. We were a month into a recession by then.

To make this more concrete, consider our data at the end of April 2001; this is shown in the top blue line in Figure 2 below.

figure 2: 1996 GDP Billions SAAR April 2001 (bold blue), June 2001 (tan), July 2001 (light green), October 2001 (red), 2002 January (sky blue), July 2002 (pink) ). The period after the NBER-defined recession peak-to-trough date is shown in gray. Dashed red line at NBER peak. Source: BEA, via ALFRED and NBER.

Note that at the end of April, the economy still looked like it was expanding. Even after the annual baseline revision, the gradient remained positive in the second quarter. Only after several revisions did the recession become apparent.

Now, as I’ve emphasized (not too much for some), NBER BCDC doesn’t rely primarily on GDP to determine peak/trough dates. Instead, they focus more on monthly indicators, most prominently employment and personal income transfers.Monthly indicators have been revised to a lesser extent, but are still subject to revision (see this Published in 2006 on the 2001 recession).So, we are Today’s monthly metrics Not what we’ve seen with subsequent release years.

{kind=link}

{kind=link}