The Conference Board supports the former, while the US state of Michigan supports the latter.

figure 1: University of Michigan sentiment index (blue) and Conference Board sentiment index (tan). Recession peak-to-trough dates as defined by NBER are grayed out. Sources: University of Michigan (FRED), The Conference Board (investing.com), and NBER.

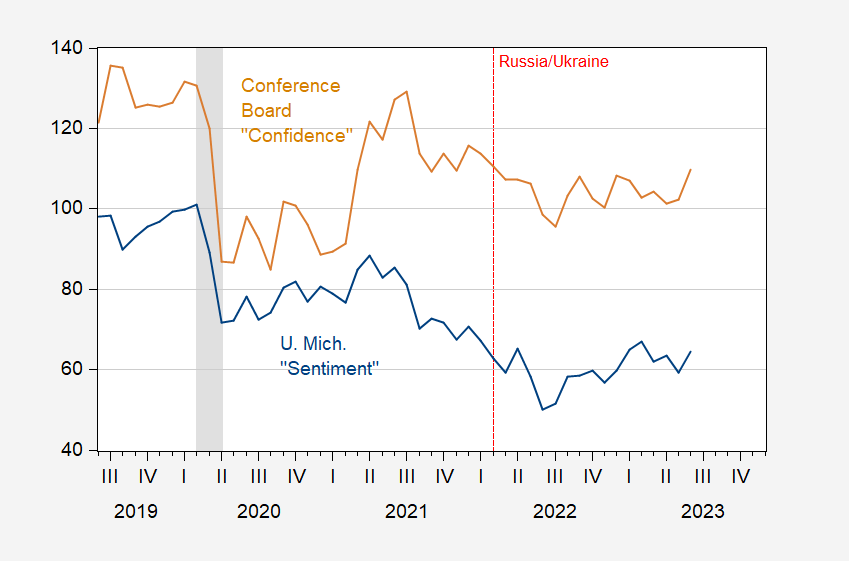

Sentiment was even lower than at the height of the pandemic, according to the Michigan Index. The Conference Board index suggests confidence is at levels seen in early 2021 and definitely above pandemic levels (110 in June vs. 94 sample average). Why is there a difference? A hint can be obtained by looking at the long-term time series of the two indices.

figure 2: University of Michigan sentiment index (blue) and Conference Board sentiment index (tan). Recession peak-to-trough dates as defined by NBER are grayed out. Sources: University of Michigan (FRED), The Conference Board (investing.com), and NBER.

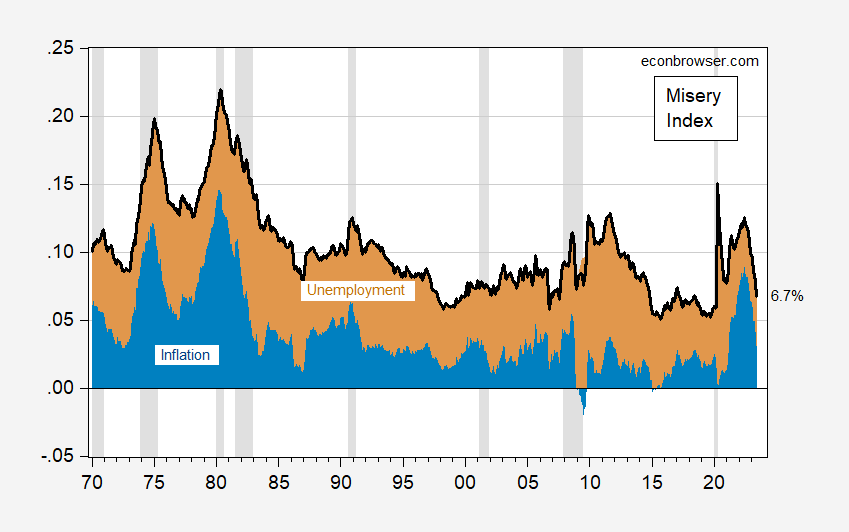

folk wisdom conveyed Investment Encyclopedia Note that the Conference Board index has a higher correlation with employment, while the Michigan index has a higher correlation with wallet problems (cost of living). This means that the two do not covariate with the misery index in the same way (see this study for the investigation of the correlation between the misery index and Michigan sentiment) postal). Consider the components of the unweighted version of the misery index as follows:

image 3: Share of misery index (thick black line), year-over-year CPI inflation (blue bar), unemployment (tan bar). Recession peak-to-trough dates as defined by NBER are grayed out. Sources: BLS, NBER, and authors’ calculations.

For the Michigan Sentiment Index, the regression results for 1970-2023M06 are:

UMCSENT = -0.415you – 0.479PI

Standardized (“beta”) coefficients. adjust-R2 = 0.41, SER = 10.07, DW = 0.16, Nobs = 576, samples 1970M01-2023M06. bold Indicates significance at 10% MSL, using HAC robust standard errors.

For the Conference Board confidence index, the regression results are:

confidence = -0.725you – 0.095PI

Standardized (“beta”) coefficients. adjust-R2 = 0.54, SER = 16.04, DW = 0.19, Nobs = 642, samples 1970M01-2023M06. bold Indicates significance at 10% MSL, using HAC robust standard errors.

One cannot compare “beta” coefficients between regressions, but within regressions. The estimates confirm that unemployment and inflation have about the same impact on the Michigan index. Unemployment is the key issue for the Conference Board metric.

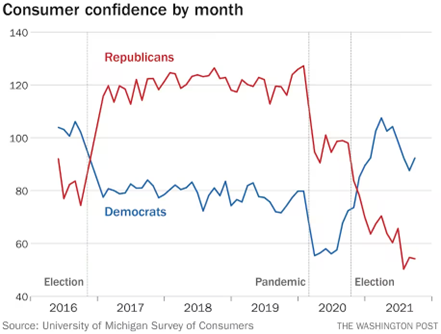

Note that I’m treating the data as mean sentiment values.I do wonder (without knowing the distribution of the responses) if there is really a mean; this graph is from Bump (WaPo, Dec 2021) illustrates the point.

source: Bump, ‘People’s views on the economy are inevitably partisan,” Washington postDecember 15, 2021.

It would be interesting to see how the categorical sentiment index stacks up with the misery index (in other words, who is out of touch with reality), but I don’t have readily available data. Mian (it still exists2023) shows that these partisan expectations influence economic decisions such as consumption. He also demonstrated that these effects increased over time.

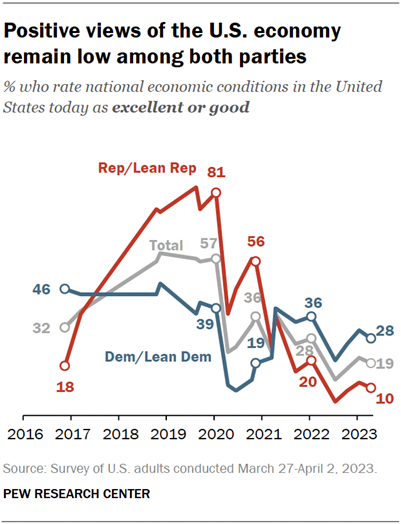

Interestingly, looking at overall economic optimism over the past seven years, Republican/Republican-leaning respondents appear to show greater volatility than Democrats/Democrat-leaning respondents.

source: Pew Research Center, April 7, 2023.

The Republican/leaning Republican range for views on the economy was more than 71 points, peaking in 2019, while the Democrat/Leaning Democrat range was more than 36 points. So while there is a partisan divide, at first glance, it seems to me that the Republican/leaning Republican swing is more intense. If behavior is indeed driven in part by sentiment, averages may not be a good measure of the impact on the economy.

{kind=link}

{kind=link}