The latest information from Japan shows that its inflation fell sharply for the second consecutive month in December 2023, and people may conclude that the period of inflation is coming to an end. The Bank of Japan assumes that this supply-side inflation is temporary and will subside quickly once these restrictions are eased. They are right. All other central banks have somehow convinced themselves that inflation is demand-driven and have been pushing interest rates higher unnecessarily. The experiment is coming to an end and I think it's clear that Japan is on the right path. At that point, New Keynesian academics and officials should resign. Afterwards, since it's Wednesday, we listen to some music to soothe our souls.

Japan's inflation rate drops sharply

Every now and then you read about the famous “widowmaker” trades where financial market players thought they could outwit the Bank of Japan.

The widowmaker trade got its name from the huge losses it caused.

These trades can be for any asset, but the most classic are bets on Japanese Government Bonds (JGBs), in which investors (aka gamblers) short the market in the hope that yields will rise when future contracts expire, when they actually This must be done by delivering assets they do not currently own.

They are short because they believe the BOJ will raise interest rates like other central banks, pushing up yields on all financial assets and depressing the prices of fixed-income assets such as Japanese government bonds.

This allows them to flood the market at the end of the forward contract and buy the bond at a cheaper price than when the contract was signed, making a killing.

The only problem is that it never works the way hoped for.

Gamblers graduate from college or elsewhere and think textbooks apply.

The Bank of Japan has proven over the past three decades that monetary economics courses provide no knowledge.

For the past year or so, widowmakers have been arguing that the final element of so-called “Japanization” will be overturned – that is, that the Bank of Japan will soften and start pushing ahead amid rising inflation. Raise interest rates.

Every month or so, I read some financial market briefing document predicting imminent tightening by central banks.

When central banks make small adjustments to policy – such as the recent one to the upper limit of their yield curve control – gamblers go wild and think the floodgates are about to open.

People can still profit from the yen carry trade, which involves borrowing yen at a low interest rate and then selling it for a higher-interest currency.

But JGB short sellers are unlikely to be satisfied anytime soon.

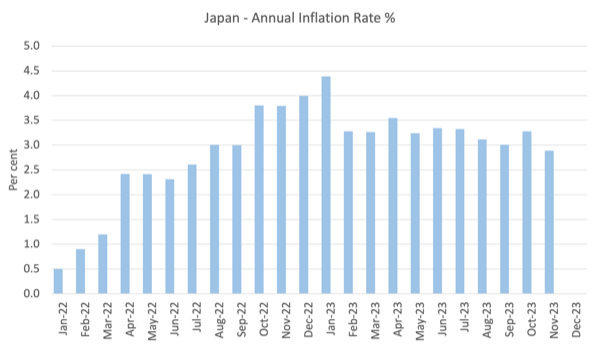

I say this because Japan's latest inflation data hardly provides a signal to the Bank of Japan that it should raise interest rates, even if it follows the logic used by other central banks.

Official data from e-Stat (Japanese government statistics agency) is as of November 2023.

This is the monthly inflation rate since January 2022.

The inflation rate at that time was 2.9%, but the monthly change between October and November 2023 was -0.187, which is a decrease in inflation from 3.3%.

Before we get the latest e-Stat data for December, this article discusses a poll conducted by Reuters – Japan's December CPI likely to hit 18-month low, fueling stable view of Bank of Japan: Reuters poll – shows that the economic slowdown is continuing, with food and energy prices rising quite rapidly.

farther:

Polls also suggest wholesale prices may have fallen in December for the first time in nearly three years…

What this tells me is that the Bank of Japan is not sending any signals at all to change its current monetary policy settings – negative policy rates and a 1% 10-year JGB cap.

Japan's period of inflation is coming to an end.

We will have official data on Friday, January 19, 2024.

I will discuss this more when I speak in London next week.

The point is, Japan once again provides an example of how mainstream macroeconomics can miss the mark even as policymakers deny what they are doing.

I read the comments on a previous post I wrote stating that the Bank of Japan operates using monetarist logic – inflation is the result of an excess monetary base.

Indeed, their official discussions talk about how they view the monetary base.

But if they were true monetarists, they wouldn't have defied the rest of the world and left interest rates unchanged over the past few years.

The decision sets them apart from other central banks that have been acting in a completely orthodox way over the past few years – rising inflation and pushing interest rates higher.

What I am trying to say is that Japan provides us with a tested example of what happens when a government and its central bank set policy beyond what most economists would consider reasonable.

For more than three decades, the differences between Japan's fiscal and monetary policy settings and those of other countries have been more than trivial.

Japan's fiscal deficit is high relative to other countries, and mainstream economists would say their monetary policy settings are extreme.

So we've been able to see for a long time what happens when these “extreme” settings are put in place.

What we are seeing is that mainstream forecasts have failed spectacularly across all major aggregates.

This is why it is important to study and understand Japan.

GIMMS London Event – Friday 26th January 2024

This time next week I will be on a plane to London, which will be my first time there since February 2020.

I'm hoping to get back to regular travel there, but we'll see how this one goes – I hate the risk of COVID.

The next week I will be attending my usual classes at the University of Helsinki, which I have been doing via Zoom for the past 3 years.

I've prepared warm clothes!

Anyway, my first date in London next week will be on Friday 26th January 2024, organized by amazing women from: Integrated management management system.

A major policy experiment has taken place over the past few years that seems to have escaped the attention of the media and commentators.

Rarely do we have the opportunity to compare two diametrically opposed approaches to solving global problems that affect all countries.

But since 2021, most central banks have raised interest rates sharply, in what they believe is a response to emerging inflationary pressures.

These countries are also said to have tightened fiscal policy to “support” their central banks' anti-inflation stance. In contrast, Japan has kept interest rates unchanged while increasing fiscal policy stimulus to help households and businesses cope with rising cost of living pressures.

Countries implementing austerity policies not only misunderstood the nature of inflationary pressures, but also exposed the poverty of mainstream policy approaches.

In this talk, I discuss why the mainstream approach fails and why it is not fit for purpose.

Date and time: Friday, January 26, 2024 starting at 13:00.

Location: Unite, 128 Theobalds Road London WC1X 8TN United Kingdom

GIMMS organizers note that they will ask people to gather from 13h00 for a prompt start at 13h30 to make the most of this important opportunity.

Coffee and cake will be served during the break, followed by a question and answer session.

Ticket link: https://www.eventbrite.co.uk/e/gimms-event-professor-bill-mitchell-tickets-788915095287

I did not receive any payment for this event.

I want to see all the gangs out there and I want you to wear masks at events to protect yourselves and those around you.

Music – Memories of the Alhambra

This is what I heard at work today.

When I studied classical guitar at the Melbourne Conservatorium of Music in the early 1970s, I was particularly interested in the work of: Francisco Tarrega – He was one of the founders of what we now call “classical guitar.”

I studied his playing carefully.

That one – Memories of the Alhambraa – is a beautiful piece of music that is a great test for both left and right hand skills.

The right-hand part requires “vibrato technique,” where the fingers play the same string in rapid succession to give the impression of a continuous sound.

The challenge is to achieve smoothness so that the listener can barely hear the tapping of individual fingers.

This is a very difficult thing to learn.

This piece is very nostalgic to me.

I spent hours trying to get it right.

The poem was written in 1899 for Tarrega's patron after a visit to the Alhambra Palace in Granada.

I visited this palace a few years ago and thought of this music.

Listening to Tarrega's oeuvre was a great backdrop for the morning's work.

This special version is from a Deutsche Grammophon CD released in 2002 – art in segovia.

It was played by a master—— Andres Segovia – As a young boy, he went to live in Granada to further his musical education.

From the sound of it, this is a very reasonable move.

That's enough for today!

(c) Copyright 2024 William Mitchell. all rights reserved.

{kind=link}

{kind=link}