last week – The RBA wants to destroy the livelihoods of 140,000 Australian workers – a shocking indictment of a failed state (June 22, 2023) – I wrote an article about the feeling of being in a parallel universe when one reads the official statement of the Bank of Japan and juxtaposes it with a series of statements from other central banks. The day after I wrote that article (June 23, 2026), the Japan e-Stat service (Japanese government statistics portal) released the latest data – Monthly CPI data – Annual inflation fell by 0.2 percentage points to 3.2% in May on the back of a sharp easing in electricity and gas prices, data showed, partly as a result of government policies aimed at reducing rising energy prices in the domestic economy. Here’s more on parallel universes. My conclusion is that ongoing experiments among central banks show that Japan’s zero interest rate regime (accompanied by fiscal expansion) is not an inflationary factor. It did not lead to a dangerous shift in inflation expectations for businesses or households. In addition, the Bank of Japan’s decision not to raise interest rates eased (temporary) inflationary pressures on cost-of-living pressures on mortgage-borrowing households. Other central banks, by contrast, have imposed additional burdens on the indebted and are orchestrating massive redistribution of income from the poor to the rich. If they continue to act blindly, they risk a recession and a sharp rise in unemployment, which will exacerbate the pain suffered by citizens.

Summary of results

1. In the 12 months ended May 2023, inflation rose by 3.2%, down from 3.4% in April.

2. The main contributors are processed food, durable goods, mobile phones and hotel expenses.

3. Falling electricity and natural gas prices reduce inflation.

4. After excluding the energy index, the CPI rose 4.3%, higher than 4.1%.

A more detailed comparison with the US

I have previously pointed out that there is little comment in the mainstream economic media on what is apparently an ongoing global experiment, given the stark difference in monetary policy approaches to inflationary pressures in Japan compared to the rest of the world.

There is near consensus among central banks that rates are now being raised, with officials claiming they are “winning” the war on inflation, which has peaked and is falling, for reasons entirely different from central banks’ intent. doing.

Clearly, the BoJ is running in a completely different direction than the neo-Keynesian macroeconomic consensus, and I see this as an experiment in the accuracy of the mainstream approach.

I commented on this experiment earlier:

1. Japan has low inflation, no currency crisis, and the living conditions of its citizens have improved due to monetary and fiscal policy initiatives (May 4, 2023).

2. Ex-BOJ chief challenges current monetary policy consensus (March 22, 2023).

3. Bank of Japan continues to show who has the power (January 26, 2023).

4. Bank of Japan has yet to change monetary policy direction (December 22, 2022).

5. Monetary institutions are the same — but culture shapes the choices we make (December 8, 2022).

6. Two Opposite Ways to Deal with Inflation – The Stupid and the Japanese Way (October 6, 2022).

7. Why Japan avoided rising inflation – a more united approach helps (July 4, 2022).

8. BoJ keeps calm, we’re running an experiment (March 31, 2022).

Japan has experienced all the global supply shocks that other countries have experienced, creating inflationary pressures.

Almost everything in Japan is imported!

However, the BOJ did not raise its policy rate and left its yield target on 10-year Japanese government bonds unchanged.

The Japanese government has also eased fiscal policy further in response to the cost of living crisis – providing fiscal transfers to households and subsidies to firms as part of a deal to squeeze profit margins.

Meanwhile, businesses elsewhere are raking in profits because our government refuses to pressure the corporate sector to do the same behavior that the Japanese government has successfully coerced from price-setters.

Because of its policy stance, the yen has come under relentless attack from financial market “short sellers” who believe they can trick the central bank into changing policy, generating huge profits for speculators.

The bank refused to be bluffed and instead inflicted huge losses on short sellers.

I discuss this issue in the third (3) blog post referenced above.

Below is an update using data through May 2023.

Japan’s current annual inflation rate (all items) (May 2023) is 3.2% lower than the January 2023 peak of 4.4%.

For the US, the August 2022 peak is 8.3% and the current 4.1%.

The four graphs below show the primary totals (in annualized percentages) for the period January 2021 to March 2023.

The dynamics were similar – energy prices rose rapidly, pushing up all group indices in both countries.

Japan is more exposed to imported food price shocks than the United States, and the lagged effects of energy price inflation on the production and transport sectors are also evident on food prices.

Soon, these lagging effects will disappear, and the overall figures for each country will decline.

While headline inflation is falling in both countries, it is difficult to argue that rising interest rates in the US are at the root of stagnant inflation in the US.

A common dynamic is higher energy prices, driven by cartel behavior amid pandemic supply constraints.

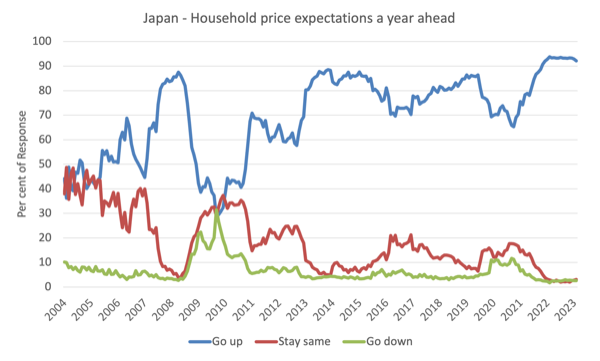

Household Price Expectations in Japan

The monthly magazine published by the Cabinet Office of Japan—— Consumer Confidence Survey – which includes data on households’ “price expectations for the coming year”.

The latest figures show:

1. The share of respondents expecting price increases within 12 months fell in May – down 0.1 percentage points to 93.1%.

2. The proportion of respondents expecting prices to remain unchanged in May increased by 0.3 percentage points to 2.7%.

3. It is expected that the proportion of prices falling will decrease by 0.2 percentage points.

As a result, more Japanese households now believe that peak inflation has passed.

The graph below shows the evolution of the expectations of the three groups of households between 2004 and May 2023.

Japan’s business inflation expectations

Fundamental to New Keynesianism is the concept of inflation expectations, which central bankers often cite to justify their continued rate hikes, even if inflation peaks sometime in the last two quarters of 2022.

This fits in particular with any analysis of the situation in Japan, which has firmly maintained what is considered a highly expansionary monetary and fiscal policy stance in the face of rising inflation from imported supply shocks.

New Keynesians assert that prices adjust to expected inflation. Under rational expectations, mainstream models predict that inflation will correspond one-to-one with changes in expected inflation.

After a period of low inflation, as inflation rises, it is speculated that people will factor this into forward-looking behavior through rising expectations, driving inflation higher once the initial factors have faded.

The RBA Governor keeps claiming that if they let inflation settle more slowly as supply factors become less important, then persistence will be self-fulfilling through rising inflation expectations.

In any of the countries I’ve looked closely over the past few months, it’s hard to see this kind of process unfolding.

Of course, neo-Keynesian causality cannot be established in Japan.

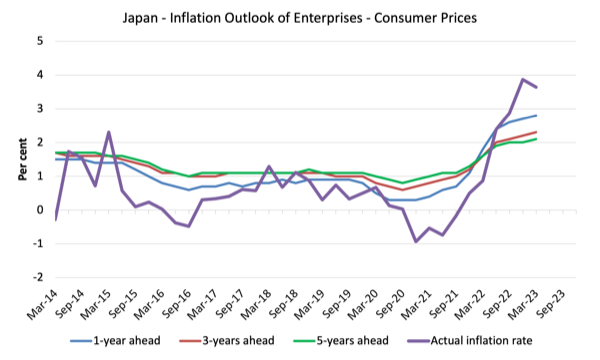

The picture below is taken from—— Tankan Summary of the Corporate Inflation Outlook – The latest data is released on April 3, 2023 and covers expectations through March 2023.

Firms are asked to assess future price changes in output prices and consumer prices.

The chart below shows the business outlook for consumer prices – 1, 3 and 5 years ahead. It also includes real inflation (thicker purple line).

Expectations lag the actual evolution of the inflation rate.

Interestingly, the rise in expected inflation slowed sharply in mid-2022, even as headline inflation continued to rise.

Now, with the CPI peak behind us, expectations are largely static and should flatten out going forward.

Given that the April data above showed that inflation was falling relatively quickly, I would expect the next Tankan survey to show that expectations are also falling.

Crucially, the data do not support the view that headline inflation remains high because of expectations.

I also examine the possibility of a relationship between changes in interest rates set by the US and Japanese central banks and inflation dynamics going back to January 1970, using econometric time-series regression techniques.

Given its technical nature, I won’t report the results here, but in plain English I found:

1. Using a range of lagged interest rate terms, there are no statistically significant systematic relationships (even at the 10 percent level).

2. A weak positive relationship can be found—that is, as interest rates rise, inflation rises—but it is not statistically significant.

3. I tested for structural breakage, etc.

In other words, the current monetary policy shift in the U.S. is unlikely to be the cause of inflation falling back and converging with Japan’s lower inflation.

Common factors are supply constraints during the pandemic, as well as the impact of Ukraine and OPEC+.

All of these are insensitive to the Fed’s interest rate decisions.

in conclusion

My conclusion so far is that when I update the data monthly to see where we are, the experiment shows that Japan’s zero interest rate regime (plus fiscal expansion) is not an inflationary factor.

It did not lead to a dangerous shift in inflation expectations for businesses or households.

In addition, the Bank of Japan’s decision not to raise interest rates eased (temporary) inflationary pressures on cost-of-living pressures on mortgage-borrowing households.

Other central banks, by contrast, have imposed additional burdens on the indebted and are orchestrating massive redistribution of income from the poor to the rich.

If they continue to act blindly, they risk a recession and a sharp rise in unemployment, which will exacerbate the pain suffered by citizens.

I prefer the Japanese approach.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}