Teaching an undergraduate macro course for the first time in three years, so I thought it was time to revise it Syllabus (Economics 442) Explain new problems (with Fall 2001).

First, Climate change and macro impacts.

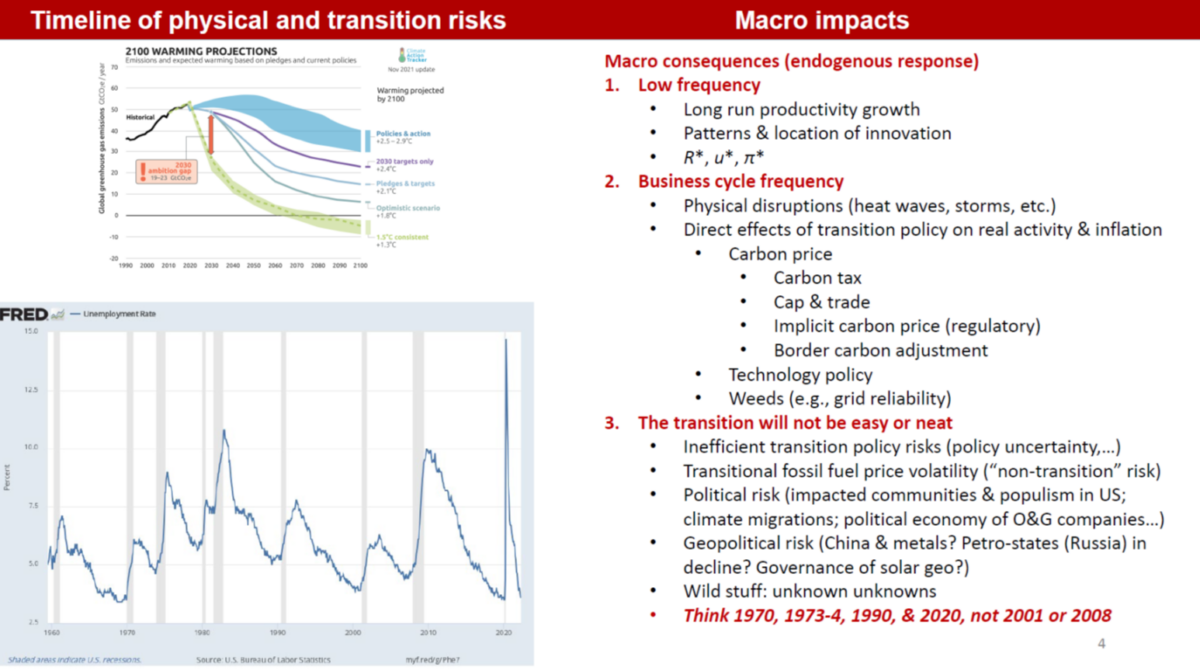

source: Inventory(2022).

There will be a focus on climate shocks that complicate macrostability (consider hurricanes, droughts, heat waves, disaster insurance crises), the consequences of fossil fuel dependence, and the impact of carbon taxes and cap-and-trade.

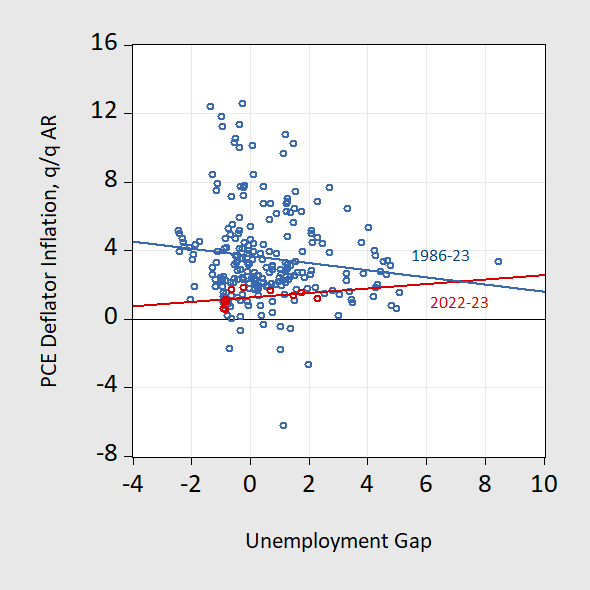

Does the Phillips Curve still apply?

figure 1: PCE deflator quarterly/quarterly annualized inflation lags the unemployment gap by one quarter from 1986 to the third quarter of 2023. Bivariate regression lines for 1986-2023 (blue) and 2021-2023 (red). The unemployment rate gap is calculated as the unemployment rate minus the Congressional Budget Office's noncyclical unemployment rate. Sources: BEA, BLS, CBO (via FRED), and author's calculations.

Some consider the rapid rise and fall to be an indictment of the traditional Phillips Curve approach. Figure 1 is instructive. However, even the basic textbook version of the Phillips Curve contains more than two variables…

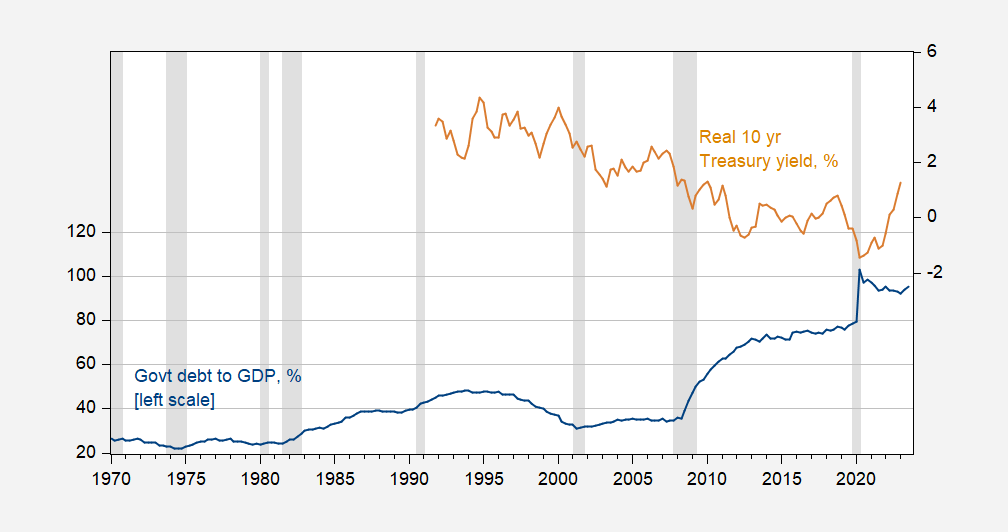

Is it government debt: why are real yields rising?

figure 2: Government debt held by the public divided by % of GDP (blue, left axis) and the 10-year real yield in % (tan, right axis). The real yield is the 10-year nominal yield minus the SPF's expected 10-year inflation rate. NBER-defined recession peak-to-trough dates appear gray. Source: Treasury, BEA, FRED, Federal Reserve Bank of Philadelphia, NBER, and author's calculations.

In 2001, the debt-to-GDP ratio shifted from falling to rising, accompanied by a fall in real yields, challenging conventional wisdom. Has the surge in debt-to-GDP ratios in 2020 contributed to a longer-term breakdown in this correlation?

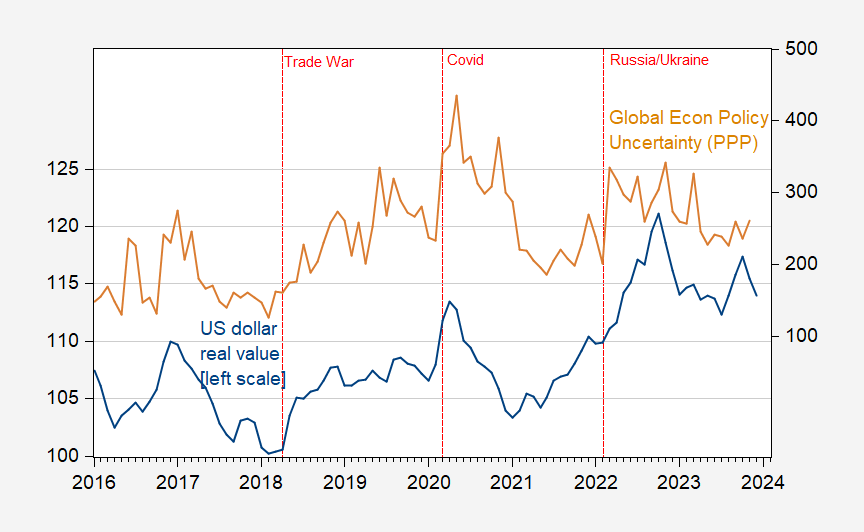

Will the dollar remain a safe-haven currency? (What does this mean for interest rates)?

image 3: Dollar (broad) real value (blue, left axis) and global economic policy uncertainty, purchasing power parity weighted (tan, right axis). The real exchange rate is spliced from January 2006 to the weight of goods before 2006 and the weight of goods and services after 2006. Source: Fed, policyuncertainty.com, and author's calculations.

In times of uncertainty, the dollar appreciates. This is especially true when the United States strikes (think COVID-19 and bleach; and September 2008).

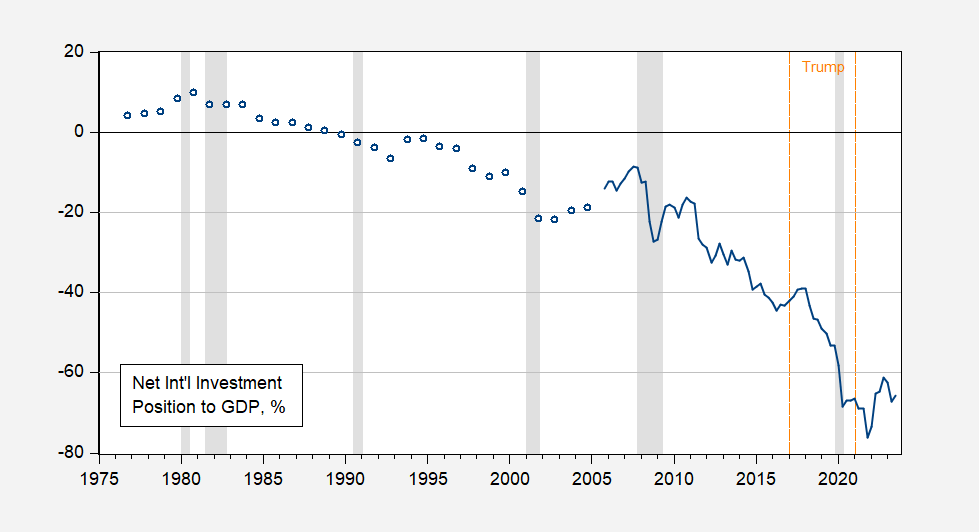

What does reserve currency status (related but distinct from safe currencies) mean? Will the U.S. net international investment position continue this trend?

Figure 4: U.S. international net investment (excluding derivatives) as a proportion of U.S. GDP, %. NBER-defined recession peak-to-trough dates appear gray. Source: BEA, NBER, and author's calculations.

Interestingly, the United States is increasingly becoming a net debtor (about 30 percentage points of GDP) compared to the Trump administration. Won!

The course textbook is by Olivier Blanchard macroeconomics.I know some people will ask “What exactly do you teach your students, Meng Qi?” (This question was raised by The same people who think a recession will happen in the first half of 2022). Now you know.

{kind=link}

{kind=link}