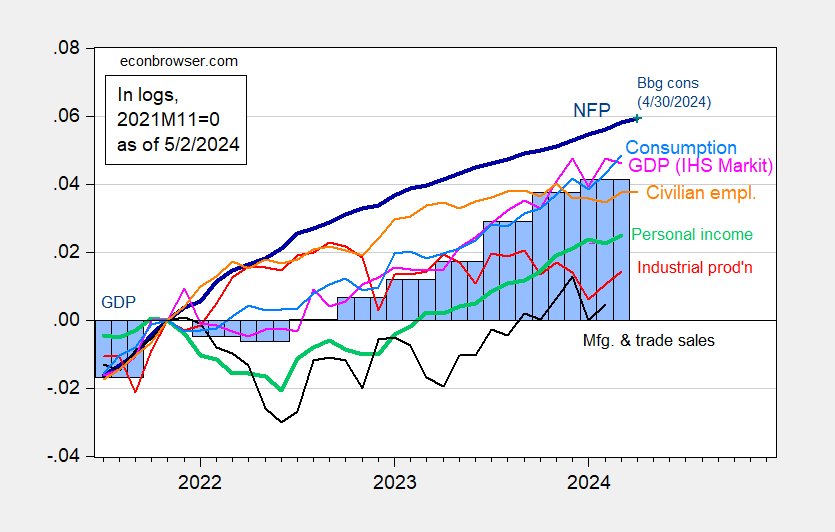

As the employment situation is released, we take a first look at what's happening in April.

figure 1: CES Nonfarm Employment (NFP) employment (blue bold), civilian employment (orange), industrial production (red), personal income excluding current transfers in 2017$ (green bold), manufacturing and trade 2017 Sales $ (black), 2017 consumption (light blue), 2017 monthly GDP (pink), third release GDP (blue bar), all logarithms normalized to 2021 M11=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q1 Advance Release, S&P Global Market Insights (Nigerian macroeconomic consultant, IHS Markit) (5/1/Published in 2024) and the author's calculations.

Average net job growth was 242,000, compared with 276,000 as of March (before the revision). The annualized monthly GDP growth rate fell to -1.9% in March from 11.5% before the revision in February.

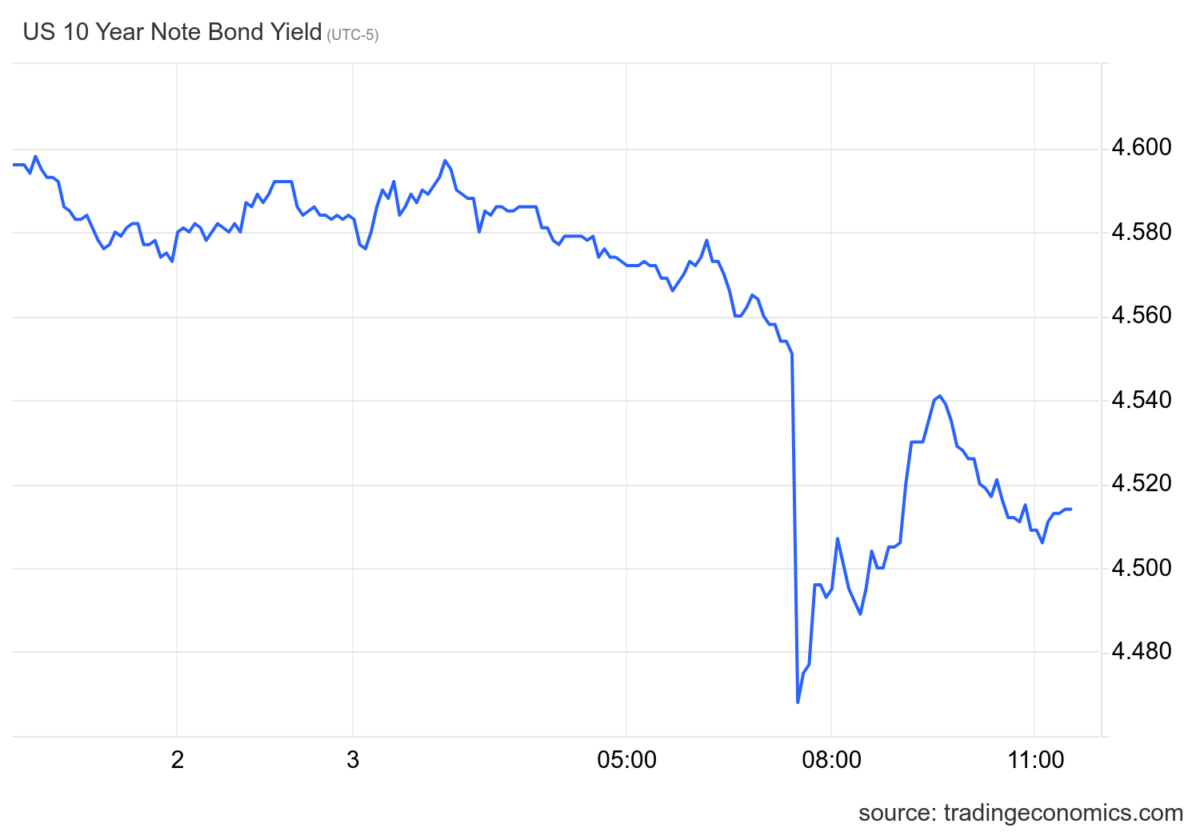

The bond market viewed the job release details overall as a deceleration (relative to pre-release). Yields have fallen, while futures point to a greater chance of federal funds falling at the September Federal Open Market Committee (FOMC) meeting.

source: TradingEconomics, viewed on May 3, 2024. Time is central.

{kind=link}

{kind=link}