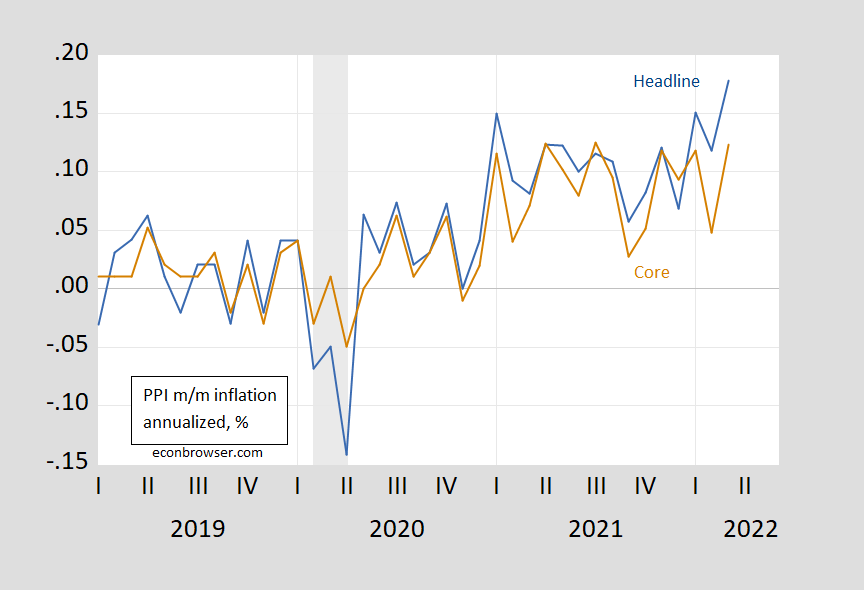

MoM PPI inflation unexpectedly rose at 1.4% vs. Bloomberg consensus of 1.1%, while core PPI rose 1% vs. consensus of 0.5%.

figure 1: Chain annualized PPI (final demand) inflation (blue) and core PPI (final demand) (brown). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: BLS, NBER, and author’s calculations.

An obvious question is, will the inflationary pressures that were seen in the PPI be seen in the April CPI?

From my August post on CPI and PPI:

Does the PPI lead the US CPI? Clark (1995) Be skeptical that PPI provides additional system predictive power.

Some analysts expect the recent rise in crude oil and intermediate product prices to travel through production chains and generate higher consumer price inflation. While simple economics suggest that such pass-through effects may occur, more sophisticated reasoning and careful consideration of the construction of the PPI and CPI data suggest that any pass-through effects are likely to be weak. Consistent with this more sophisticated analysis, empirical evidence also suggests that production chains only weakly link consumer prices to producer prices. PPI changes are sometimes helpful in predicting CPI changes, but this cannot be done systematically. Therefore, the recent rise in some producer price indices does not by itself herald a rise in the CPI.

Corporal and others. (2002) Using a more formal multivariate approach, it is concluded that for the G-7 economies, the PPI does lead the CPI. It remains to be seen whether these findings still hold true in the current environment (and newer versions using PPI).

This is an open question as the change in the correlation between monthly/monthly CPI and lagged PPI inflation is more pronounced.

Correlations aside, I tried to use a simple bivariate VAR (with 3 lags and a constant) to do a quick and dirty assessment of whether the PPI provides additional information on the evolution of the CPI. Between February 2010 and December 2019 (ie, before the pandemic), when the PPI was first ordered, the PPI explained about 40% of the short-term (1-3 months) CPI variance, which was slightly above the level. However, ordering PPI first attributes exogenousness to PPI. If I order CPI first, then PPI accounts for almost zero of CPI variance.

If 2021-2022M03 were added to the sample, the results would change dramatically, at least assuming a more exogenous PPI. Then, with PPI prioritization, the PPI share of variance rose from 40% to 80% at 10 months. (Results sorted by CPI did not change much in the short term; the variance accounted for by PPI rose to 20% in 10 months).

The fact that the relationship between PPI and CPI may have changed highlights that, until 2019M12, one cannot reject the null hypothesis that PPI is not Granger causes CPI (and can reject the null hypothesis that CPI is not Granger causes CPI PPI).Including the 2020-2022M03 period, a were able Reject the null value at 5% msl.

The point forecast using the full sample VAR (order PPI first) is 1.04% in April (vs. 1.23% in March, on a logarithmic basis).

{kind=link}

{kind=link}