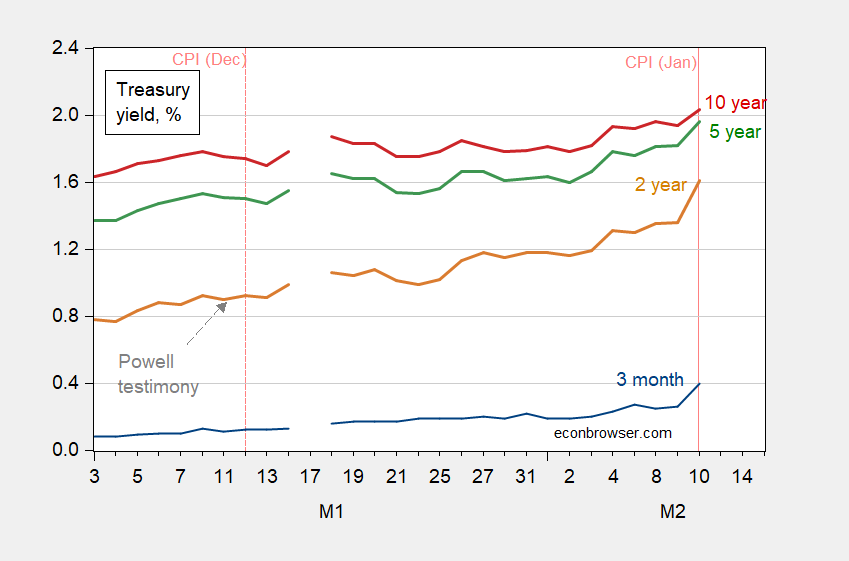

Nominal and real yields rose, as did inflation breakevens, while the yield curve flattened.

figure 1: US Treasury 3-month yield (blue), 2-year yield (brown), 5-year yield (green), and 10-year yield (red), all expressed as a percentage. Dotted pink line for CPI release date. Source: Treasury via FRED.

The sharp rise in yields, especially between 3 months and 2 years, suggests that short-term rates are rising faster than the market had expected.

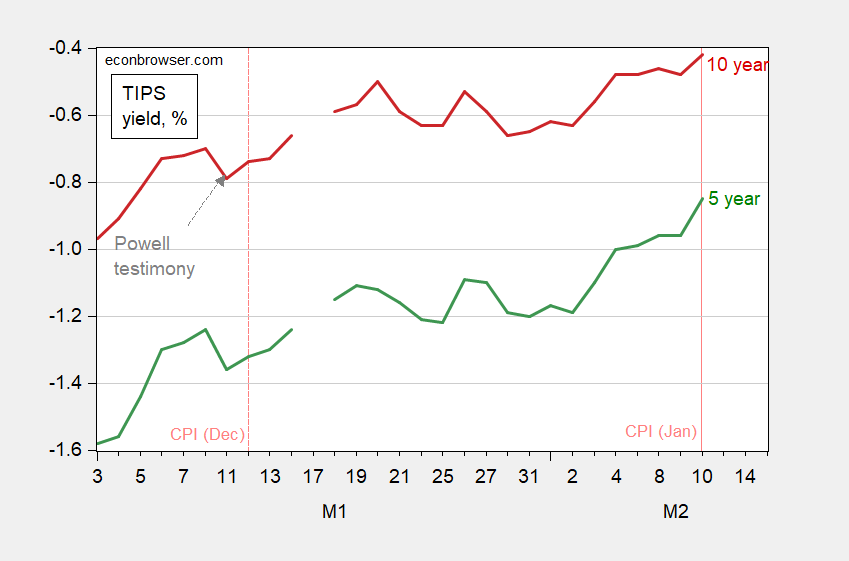

At the same time, real interest rates are rising, as measured by TIPS yields, including liquidity premiums.

figure 2: TIPS 5-year yield (green) and 10-year yield (red), both in %. Dotted pink line for CPI release date. Source: Treasury via FRED.

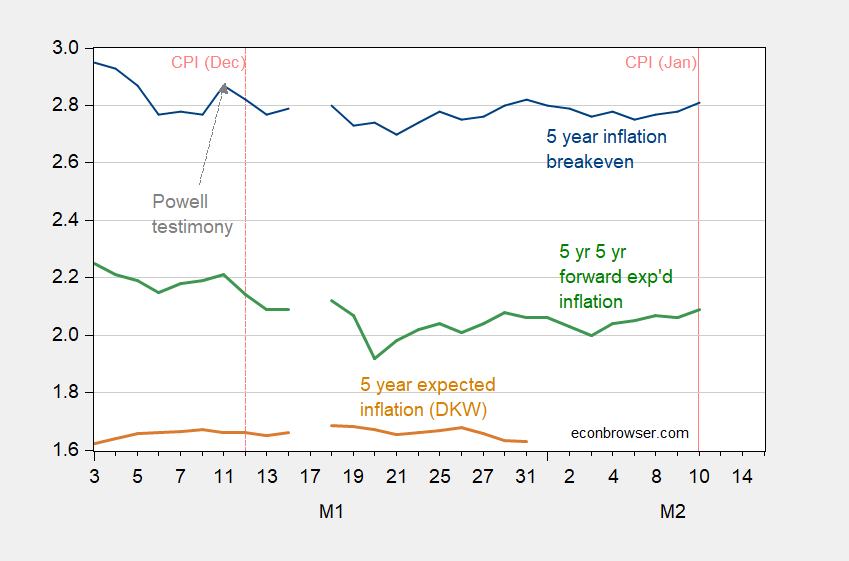

Implied expected inflation over the next five years – both current and the next – increased by 3 basis points.

image 3: 5-year maturity calculated using 5-year Treasury note minus 5-year TIPS yield (blue), 5-year expected inflation rate (brown), and 5-year, 5-year forward inflation breakeven (green) Inflation breakeven point. Dotted pink line for CPI release date. Source: Treasury via FRED, Kim, Walsh & Wei (2019) Follow D’amico, Kim and Wei (DKW) on 2/10/2022, and the author’s calculations.

Given how different the risk and liquidity premiums (according to Kim, Walsh, and Wei) are to estimated expected inflation after unadjusted inflation breakeven, one must be careful to extrapolate from these changes, especially such small ones .

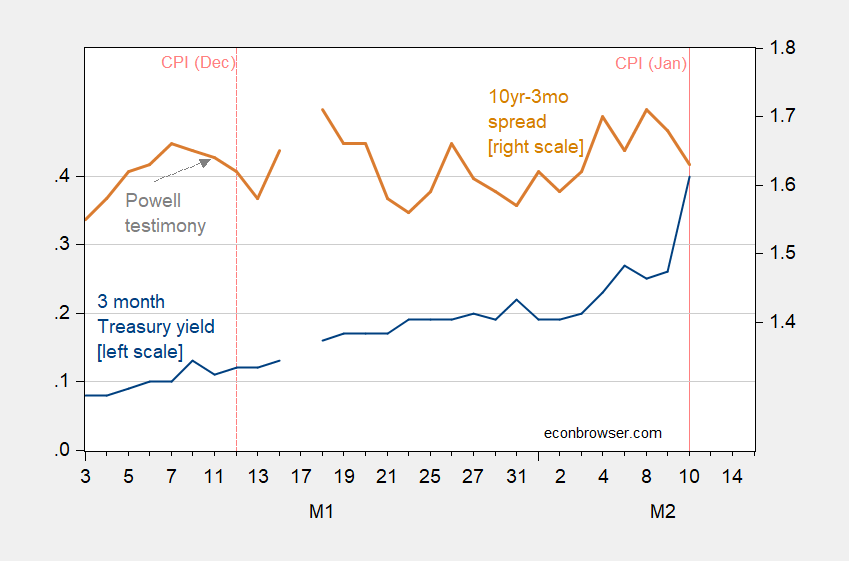

Finally, even as long-term yields rose, term spreads narrowed by 5 basis points.

Figure 4: Treasury 3-month yield (blue, left scale), 10-year-3-month spread (brown, right scale), both in %. Dotted pink line for CPI release date. Source: Treasury via FRED, and author’s calculations.

While the flattening of the yield curve suggests that the market is expecting a deceleration, it remains to be seen. The current spread is roughly the same as the March 2021 spread.

{kind=link}

{kind=link}