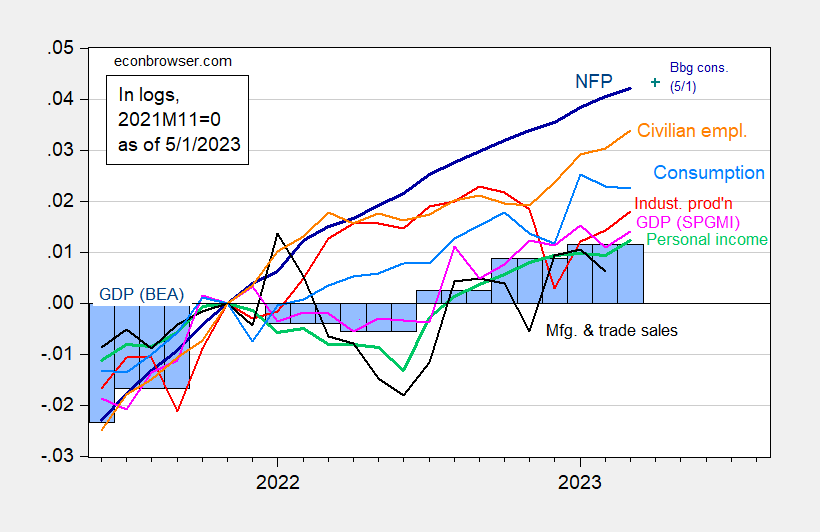

S&P Global Market Insights reported monthly GDP growth of 0.3% (3.9% annualized) in March, with final sales up 6.3% (annualized). This follows Thursday’s announcement that nominal personal income and nominal personal spending beat market expectations by 0.1 percentage points m/m. Here’s a picture of the key series followed by the NBER’s Business Cycle Dating Committee, adding monthly GDP (where the first two are real personal income, excluding current transfers and nonfarm payrolls).

figure 1: Non-farm payrolls, NFP (dark blue), Bloomberg 5/1 consensus (blue+), private employment (orange), industrial production (red), China’s personal income excluding transfers in 2012 (green), manufacturing and Trade Sales Ch.2012 USD (black), Ch.2012 USD Consumption (light blue) and Ch.2012 USD Monthly GDP (pink), GDP (blue bars), all log normalized to 2021M11=0. Data sources for the third quarter: BLS, Federal Reserve, BEA 2023Q1 released in advance through FRED, S&P Global/IHS Markit (nee Macroeconomic Consultant, IHS Markit) (5/1/2023 release) and the authors’ calculations.

With the exception of consumption, most series are showing a continuous upward trend. Measured job growth continues to lead the upward trend.

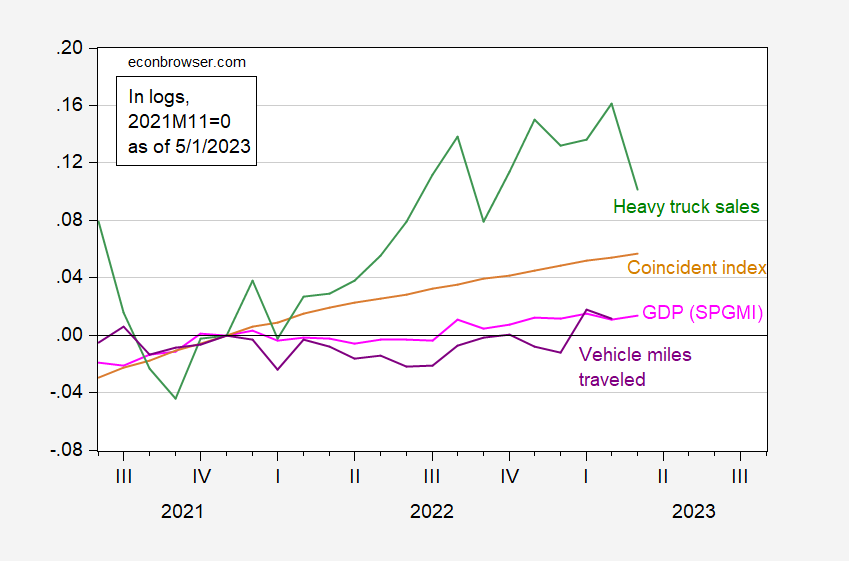

Some alternatives have been proposed. In Figure 2, I show the Philadelphia Fed’s US coincident index, heavy truck sales, and vehicle miles traveled compared to monthly GDP.

figure 2: 2012 monthly GDP in USD (pink), coincident index (tan), heavy truck sales (green), and vehicle miles traveled (purple), all in logarithmic form, Nov 2021 = 0. source: S&P Global/IHS Markit (nee Macroeconomic Consultant, IHS Markit) (5/1/2023 release), Philadelphia Fed, Commerce Department, and NHTSA via FRED, and authors’ calculations.

The coincident index, which primarily reflects labor market indicators, continued to grow at a faster pace than monthly GDP. heavy truck sales, Special Information Measures for Business Cycle Movements, which had surpassed the coincident index, but fell sharply in March. By contrast, vehicle miles driven, a poorly coincidental indicator of a recession, continued to rise in February.

The above is in line with GDP estimates, suggesting that a recession is yet to come. (For more on GDP+ and final sales, see this postal.)

{kind=link}

{kind=link}