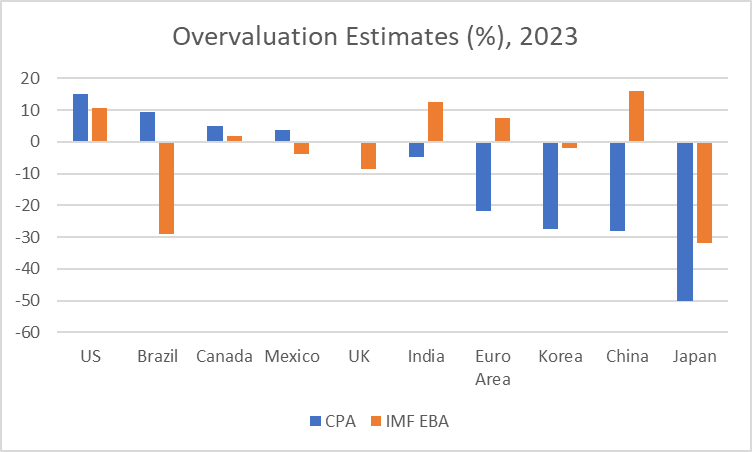

The Alliance for Prosperous America and the Blue Collar Dollar Institute develop measures of currency misalignment and report in their Currency Misalignment Monitor (the august issue is here). I thought it would be interesting to compare their estimates of currency overvaluation with those reported by the IMF in their reports. External Sector Report (July). Here’s a chart of the currencies they’re watching in August.

figure 1: Currency misalignment measures from the CPA/BCDI (blue bars) and the IMF EBA (tan bars), expressed as percentages. Values greater (less than) zero are overestimation (underestimation). source: CPA and International Monetary Fund.

Why is there such a big difference? CPA/BCDI estimates are based on the methodology employed (2008) SMIM by William Cline. Using trade elasticity, overvaluation is defined as the percentage of depreciation required to bring the current account into balance over time, requiring all other current account balances to be consistent.

The IMF External Sector Report provides some estimates of the dislocation. Here, I report an approach based on the External Balancing Approach (EBA). Dislocation refers to the amount of exchange rate change required to bring the current account to a level consistent with medium-term equilibrium (not necessarily zero).

In other words, EBA depends on Savings Investment Framework.This approach has a long history both within and outside the IMF (my acquaintance began with Chin and Prasad (2000)published in JIE 2003, but for earlier versions, see Feldstein and Horioka (1979)1980 Published Economic Journal (over 4000 citations).

Klein’s approach does not assume that zero balance is the goal; thus, while the overall mathematical framework is the same (matrix, matrix!), the goal is quite different. To see how crazy this zero balance standard is, it means a “fair” exchange rate means zero current account balances, which in turn means zero financial account balances. In other words, countries are neither borrowers nor savers in the medium term.

See earlier CPA discussion of dollar value analysis, here. Discussion of measurement misalignment, here.

{kind=link}

{kind=link}