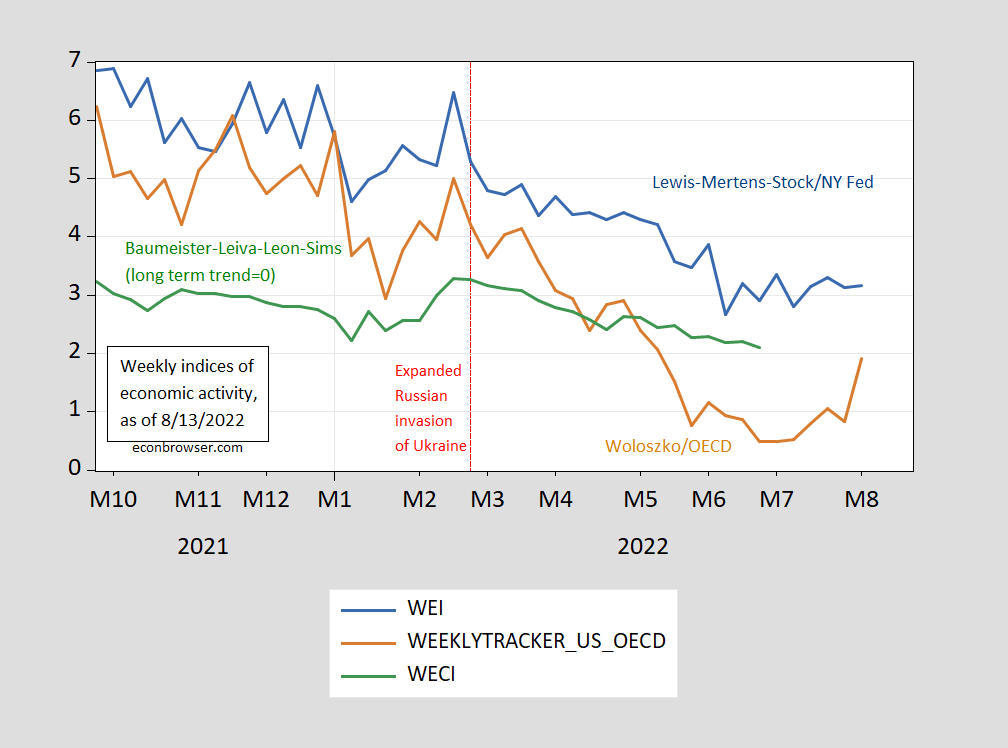

Lewis-Mertens-Stock (NY Fed) weekly economic indicators and Baumeister, Leiva-Leon and Sims WECI weekly indicators as of 12/10; and Woloszko (OECD) Weekly Tracker as of 26 November (not updated).

figure 1: Lewis-Mertens-Stock weekly economic index (blue), OECD weekly tracker (tan), Baumeister-Leiva-Leon-Sims US weekly economic conditions index plus 2% trend (green).Source: New York Fed via fred, OECD, WECIand the author’s calculations.

The deceleration over time and across metrics has been pretty consistent, with the exception of the weekly tracker. A WEI reading of 0.6% for the week ended Dec. 10 could be interpreted as a 0.6% YoY increase if the 0.6% reading persists throughout the quarter. The OECD Weekly Tracker reading of -0.5% can be interpreted as a year-on-year growth of -0.5% as of Oct 26 (the series has not been updated in two weeks, the reading is interpreted at last week’s posts). This Baumeister et al. A reading of 0.6% was interpreted as a growth rate of 0.6% above the long-term trend growth rate. US GDP growth averaged around 2% over the period 2000-19, so this implies an annualized growth rate of 2.6% through 12/10.

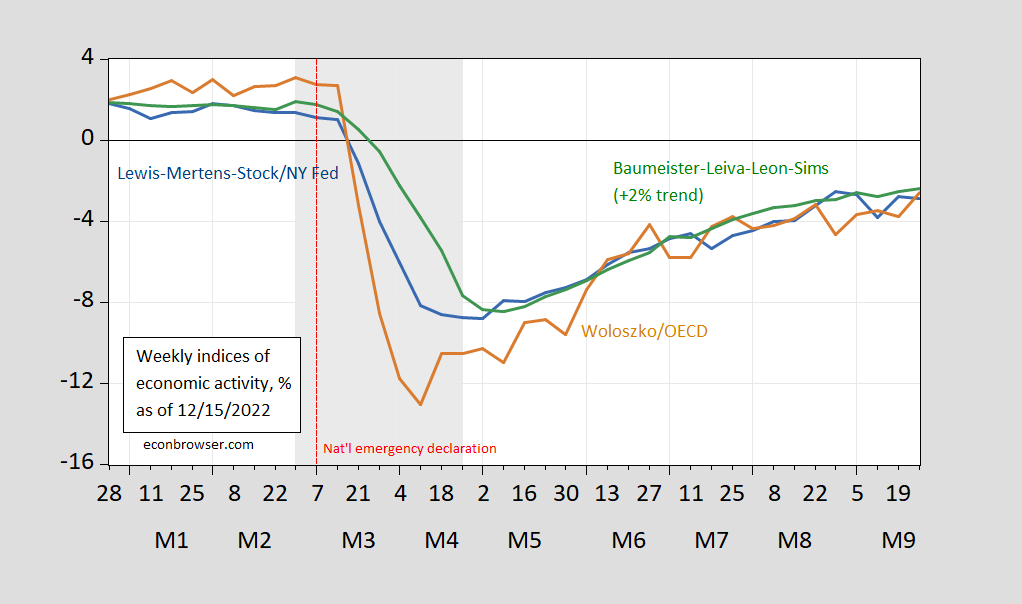

Are these latest figures consistent with an ongoing recession? For reference, I show the same series from early 2020 in Figure 2.

figure 2: Lewis-Mertens-Stock weekly economic index (blue), OECD weekly tracker (tan), Baumeister-Leiva-Leon-Sims US weekly economic conditions index plus 2% trend (green). Recession dates as defined by NBER are shaded gray.Source: New York Fed via fred, OECD, WECINBER, and author’s calculations.

{kind=link}

{kind=link}

{kind=link}